It usually starts with a quiet glance at the mailbox, a late-night bill, or a mortgage payment that suddenly feels heavier than it did last year. For many men over 45, the fear of losing the home is not really about the house itself — it is about what the house represents when money starts to feel less certain.

Why This Happens

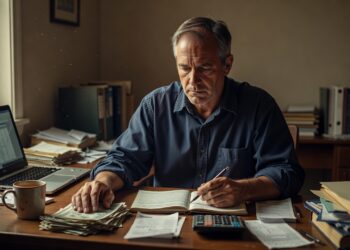

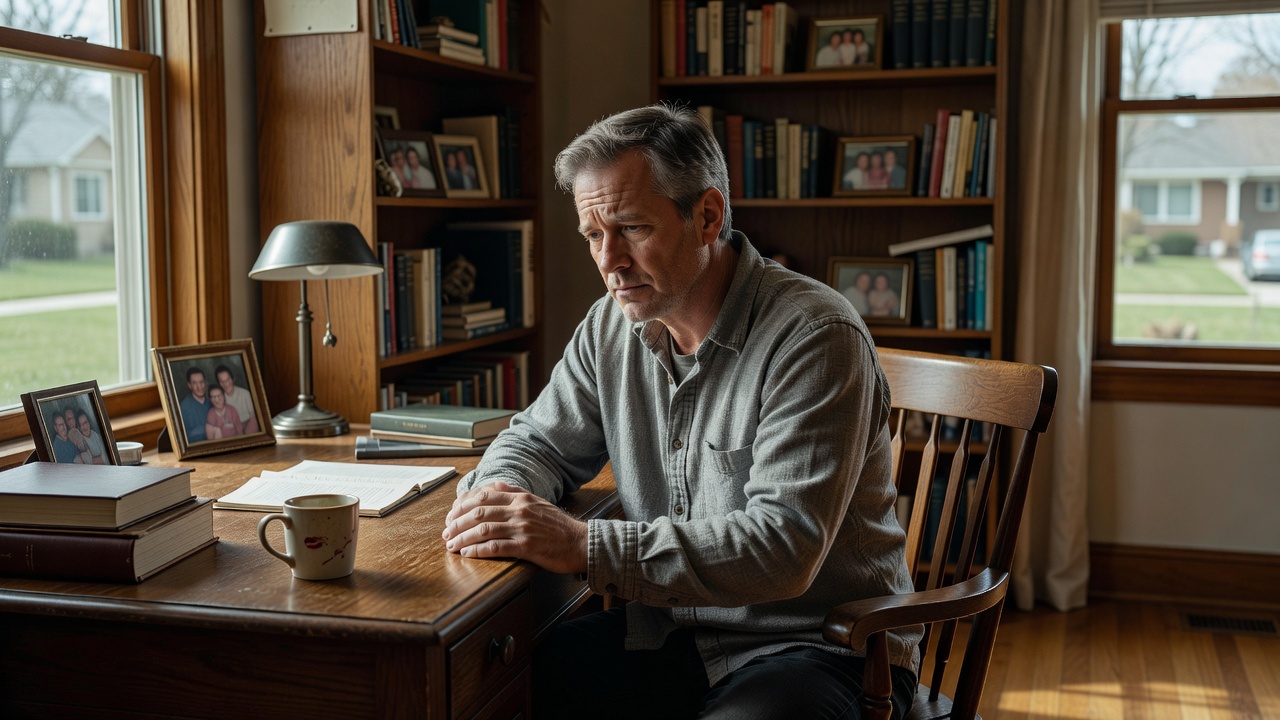

For a lot of men over 45, the fear of losing a home does not show up as panic. It shows up as silence, irritability, overthinking, or a strange need to keep everything looking normal. The mortgage gets paid, the lights stay on, and the outside life still looks steady, but inside there is a constant question: what happens if one thing goes wrong?

This is often the age where money stops feeling like a simple matter of earning and spending. It becomes tied to identity, responsibility, and the story a man has been telling himself for years. If he has been the provider, the stabilizer, or the person who kept the household from falling apart, then the home starts to symbolize more than shelter. It becomes proof that he held things together.

That is why the fear can feel so private. Losing a home is not just a financial event in the mind of someone who has built his life around being dependable. It can feel like public failure, even when nobody else is saying that. The nervous system does not always distinguish between a real crisis and the possibility of one, so even a small setback can trigger a much bigger emotional reaction.

In daily life, this fear often grows during seasons that look ordinary from the outside. A job changes, a retirement account looks weaker than expected, a medical bill appears, or a spouse starts asking questions about spending that were easy to ignore before. The issue is rarely one bad month. It is the feeling that the ground has become less stable than it used to be.

A person can be doing everything “right” and still feel this fear. That is because the fear is not only about numbers. It is about the gap between the life a man expected to have by this age and the one he is actually trying to maintain.

The Hidden Pattern Behind It

The hidden pattern is usually not reckless spending. It is delayed attention. Many men are taught to endure first and examine later, which works in emergencies but causes trouble when money pressure becomes chronic. They will keep pushing forward, hoping the next paycheck, the next bonus, or the next good month will make the discomfort disappear.

That pattern creates a strange split. On paper, the household may still be functioning. In practice, the emotional burden keeps building because the problem is never fully named. This is usually where people realize their money isn’t random… it’s patterned. The same stress, the same avoidance, the same quiet resetting of the mental calendar every month.

The fear of losing a home often sits on top of older beliefs:

– I should already have this figured out.

– I cannot afford to make a mistake now.

– Asking for help means I failed.

– If I stay calm, maybe this will pass.

Those beliefs can be powerful because they feel responsible. But they also keep people from looking directly at the numbers until the pressure becomes personal. A man may not be afraid of the payment itself. He may be afraid of what it would mean if he finally had to admit the payment has become a strain.

There is also a common emotional pattern here: the home becomes the last visible sign that life is still intact. If income rises and falls, careers change, children leave, relationships shift, and health gets less predictable, the house remains the place that says, we are still here. So when the house feels at risk, the fear is amplified by everything else that already feels less certain.

That is why this kind of fear can survive even when the math does not yet justify it. The mind is not only measuring affordability. It is measuring dignity, control, and the fear of being cornered.

Common Mistakes People Make

One of the most common mistakes is treating the fear as a personality flaw instead of a signal. Men often assume they are simply being weak, dramatic, or overly sensitive. In reality, the fear is often the first honest indication that the financial setup is carrying more weight than it should.

Another mistake is over-focusing on one bill while ignoring the pattern around it. Someone may obsess over the mortgage and miss the fact that the real problem is uneven income, recurring debt, or a lifestyle that no longer matches current capacity. The home becomes the emotional target because it is the largest, most visible obligation.

A third mistake is using avoidance as a coping strategy. The statements go unopened, the spreadsheet never gets updated, and the budget gets reimagined in the mind rather than checked in reality. Avoidance can feel calming in the short term because it delays shame, but it usually increases fear later because uncertainty grows in the dark.

Many people also make the mistake of comparing their situation to someone else’s highlight reel. They look at a neighbor, a brother, or a coworker and assume everyone else is more secure. That comparison can be especially painful for middle-aged men because financial struggle at this age can feel like it should have been solved by now. The result is often more silence, not more clarity.

A final mistake is trying to fix the fear with a vague promise to “do better.” That sounds responsible, but it is too fuzzy to change behavior. The mind needs structure, not just intention, because money stress usually returns to the same habits unless something specific interrupts the cycle.

Real-Life Patterns and Behaviors

When you look closely, the fear of losing a home often shows up through repeat behaviors long before it becomes an emergency. A man might check his bank balance multiple times a day but never look at the full picture. He may feel better for a moment, then worse again, because he is monitoring anxiety rather than managing cash flow.

Another common pattern is protecting the family from discomfort by staying vague. He may say everything is fine, even when he is mentally rearranging bills in his head. This is not always dishonesty. Sometimes it is an attempt to prevent worry from spreading. But when people in the home cannot talk honestly about money, the fear tends to grow in private.

The behavior can also become cyclical. A stressful month leads to tight control, then relief leads to spending, then guilt returns, then the cycle starts again. The person may not feel irresponsible. He may feel trapped between wanting normal life and needing more discipline than he can sustain emotionally.

Common real-life signs include:

– putting off home repairs because the money feels too uncertain

– avoiding conversations about refinancing, insurance, or debt

– feeling tense every time a major household expense appears

– acting more confident than the internal numbers support

These patterns matter because they reveal a deeper truth: fear changes decision-making. It can make people overly cautious in some areas and strangely passive in others. They may clutch small amounts of cash while ignoring larger structural issues that would actually reduce risk.

This is why the problem is so often misunderstood. Outsiders may think the issue is income, but the daily behavior shows something more complicated. It is about how a person experiences control. When control feels fragile, even stable money can feel unstable.

What Actually Helps

What helps most is not pretending the fear is irrational. It is acknowledging that the fear has a logic, even if that logic is emotionally overloaded. A home is tied to safety, status, family, and memory, so of course the mind reacts strongly when that stability feels threatened.

The next helpful step is to separate the emotional meaning from the financial facts. That means looking at the mortgage, debts, income, and reserves without turning the exercise into a moral judgment. A budget tool, a mortgage calculator, or a simple cash flow tracker can help here because it creates a visible picture instead of a vague dread. The point is not to become obsessed with numbers. It is to give the fear something real to stand against.

When people finally see the full picture, they often discover the problem is more specific than they thought. Sometimes the issue is not the mortgage itself but timing. Sometimes it is not the housing cost but the absence of a buffer. Sometimes it is not income alone but the way expenses spike at certain points in the month.

That is the moment when the fear becomes more manageable, because the brain can work with a pattern. A clear tool can turn a cloud into a map. And once the map exists, the next decisions feel less like survival and more like strategy.

It also helps to stop treating home security as a private test of masculinity. Stability is not the same thing as pretending. People who handle money well are often the ones willing to look directly at the uncomfortable parts before they become expensive. Quiet honesty is more useful than quiet pride.

What To Do Next

If this fear feels familiar, the next step is not to make a dramatic vow. It is to get a clearer picture than the one anxiety has been giving you. Start with one practical tool: a simple budget tracker, a mortgage affordability calculator, or a debt payoff view that shows what is actually pressuring the household.

Then look for the pattern, not just the problem. Ask yourself when the fear gets worse, what events trigger it, and which expenses create the most tension. That kind of review often reveals that the issue is less about a single crisis and more about a repeating strain that has never been named out loud.

If you want a calmer way to approach it, use a calculator before you use worry. A tool will not solve the whole problem, but it can show you whether the fear is coming from a temporary squeeze, a structural mismatch, or an avoidable habit loop. Once you can see that clearly, the home stops feeling like a question mark and starts feeling like something you can plan around.

And that is really the shift here. Not certainty, but clarity. If you are at this stage, the most useful next move is to open the numbers, not the anxiety. A small check-in with a budgeting tool today can tell you more than a month of silent pressure ever will.

Related Reading

- Why Men Over 45 Quietly Fear Job Loss

- Why Monthly Bills Feel Worse for Men Over 45

- Why Men Quietly Fear Losing Financial Stability

Keep Exploring the Pattern

Watch more breakdowns of real-life money behavior on our YouTube channel.

Browse the full Money Behavior Library to explore more patterns like this one.

If you want a clearer view of your monthly patterns, try the Salary Breakdown Calculator, the Subscription Cost Calculator, or the Bill Due Date Planner.

Explore more patterns in the Money Behavior Library — a growing collection of real-life financial patterns explained clearly.

Disclaimer:

This content is for educational and informational purposes only and does not constitute financial advice. Always consult a qualified financial professional before making personal financial decisions.