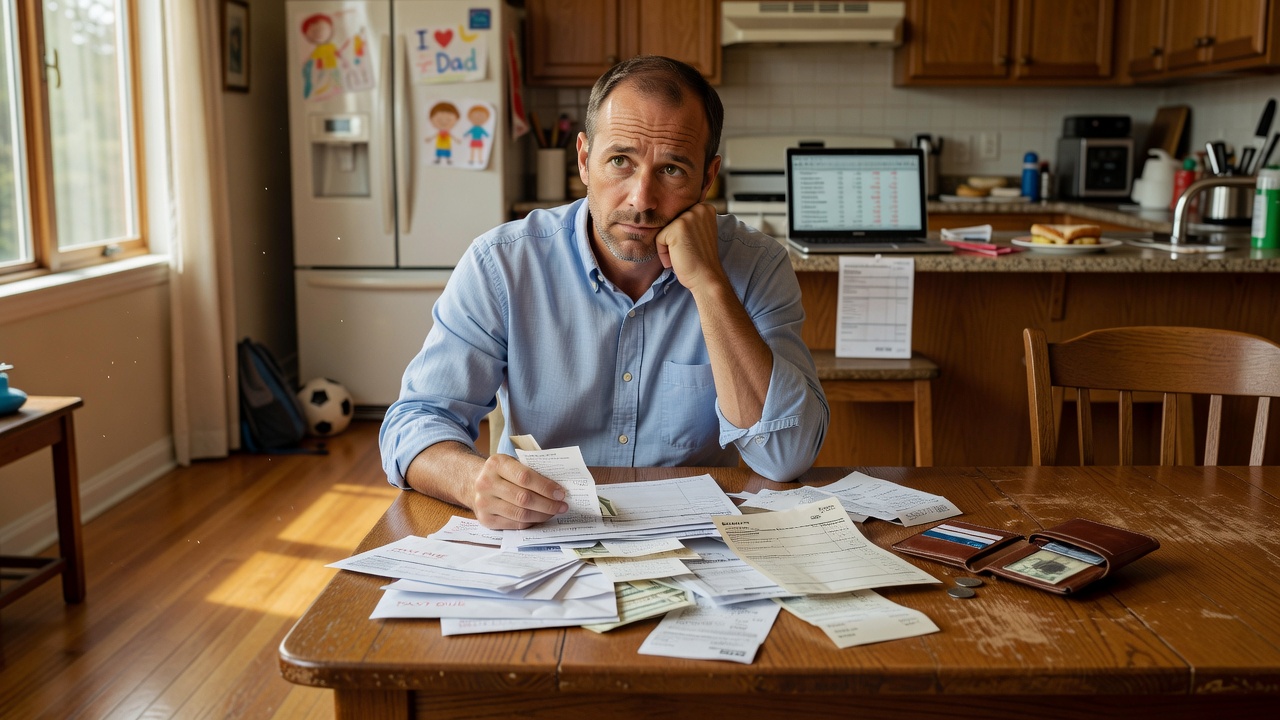

You check your account after payday and the number already feels smaller than it should. The mortgage clears, a few subscriptions renew, the grocery run costs more than expected, and somehow the money that looked solid on paper is already moving out the door. For a lot of working fathers, this does not feel like overspending so much as a quiet vanishing act.

Why This Happens

Working fathers often describe the same strange feeling: income comes in, obligations instantly surround it, and the remaining money seems to evaporate before there is any real chance to enjoy it. That experience is usually not a sign that someone is careless. It is more often the result of a life structure where income has already been mentally assigned before it even lands.

By the time payday arrives, a father may already be carrying a long list of invisible commitments. Housing, childcare, school costs, fuel, groceries, insurance, family activities, debt payments, and occasional repairs all wait in line. In that kind of month, money does not disappear in one dramatic moment. It disappears through many small, predictable exits that feel sudden only because they happen quickly and repeatedly.

This is where the emotional part matters. Many working fathers are not just managing bills; they are managing identity. They often feel pressure to be steady, prepared, and unfazed, even when the numbers are tight. That pressure can create a strange distance from the money itself, where the focus becomes keeping everything moving rather than noticing the pattern underneath it.

A lot of people assume the answer is simply to spend less, but that misses the deeper issue. The real problem is often that income is being consumed by a lifestyle structure built around fixed obligations and fast-moving family needs. When every dollar already has a job, the account balance can feel misleadingly temporary.

The Hidden Pattern Behind It

The hidden pattern is not just spending. It is compression. Working fathers often live in a financial system where paydays are followed immediately by a cluster of recurring demands, and the space between one obligation and the next is almost nonexistent. The money does not have time to sit still long enough to feel like wealth.

This compression creates a very specific psychological effect. When money is moving out quickly, the brain stops seeing income as flexible and starts seeing it as fragile. That can lead to a narrowed view of decisions, where each expense feels necessary in the moment because there is no emotional buffer left to evaluate it calmly. The result is not always reckless behavior. Sometimes it is just relentless momentum.

There is also a pattern of delayed visibility. Many fathers do not feel the impact of spending at the moment they spend it, because each decision looks reasonable in isolation. The impact shows up later, when the account balance is already thin and the next obligation is near. That delay makes the money feel like it vanished instantly, even though it was quietly absorbed over days or weeks.

In practice, the pattern often looks like this:

– income lands and feels briefly available

– fixed costs and family needs claim most of it

– small purchases fill in the gaps of a stressful week

– the remaining balance is too small to feel useful

This is usually where people realize their money is not random. It is patterned. And once a pattern becomes visible, it becomes less shameful and more workable.

Another hidden layer is what might be called recovery spending. A father who has been working hard, commuting, solving problems, and carrying stress may unconsciously use small purchases to soften the edges of daily fatigue. Lunch out, tools, convenience items, streaming, a quick upgrade, or something for the kids can all feel minor. But when life is already full, these small releases start behaving like a leak.

Common Mistakes People Make

One common mistake is treating the problem as if it is only about discipline. That framing can make an already tired person feel worse. The reality is that many working fathers are dealing with a mix of timing, obligations, and emotional load. If the system is tight, a stricter attitude alone will not create room.

Another mistake is looking only at large expenses and ignoring the repeated middle-sized ones. People often scan the biggest bills and assume that is where the story ends. But the real pressure frequently comes from the combination of groceries, gas, school costs, convenience purchases, family outings, and little fixes that keep a household functioning. None of them look dramatic alone. Together, they can dominate a paycheck.

A third mistake is not giving the money a place to land before it gets assigned. When income goes straight from deposit to obligation without a pause, it becomes harder to understand what is actually happening. A simple budgeting tool or cash-flow tracker can make this visible without turning life into a spreadsheet obsession. Sometimes the issue is not spending too much. It is not seeing the timing clearly enough.

People also underestimate how often stress creates false urgency. If a father is always solving the next thing, he can start treating almost every expense as urgent. That habit makes sense in a busy life, but it can quietly erase any sense of choice. The money starts following the mood of the day instead of the plan for the month.

Finally, many people assume a better income will automatically solve the feeling. Sometimes it helps, but not always. Higher income can still disappear instantly if the habits, expectations, and obligations rise with it. That is why the emotional experience often follows people upward. The number changes, but the pattern stays.

Real-Life Patterns and Behaviors

This issue becomes clearer when you look at everyday behavior instead of abstract budgets. A working father might tell himself that he is being careful because he does not make big reckless purchases. And he may be telling the truth. But his money may still be vanishing through the structure of his week.

One pattern is the weekday recovery loop. After work, there is little energy left for planning, cooking, comparison shopping, or delayed decisions. So the easiest option wins. Convenience becomes a financial habit, not because it is luxurious, but because it is frictionless. Over time, convenience can become one of the quietest drains on a household budget.

Another pattern is the family-first reflex. Many fathers will absorb costs they do not personally enjoy because they want to protect their family from stress. That can be noble, but it can also become automatic. When every small request is answered quickly, the budget loses its boundaries. The father feels generous, but the account feels invisible.

A third pattern is the payday reset illusion. People often feel briefly better when income arrives, then spend from relief rather than intention. The money seems abundant for a short window, and the body relaxes. Then reality returns in the form of bills, school needs, fuel, and routine spending. The drop from relief to scarcity can feel abrupt even when it was always going to happen.

There is also the pattern of silent comparison. Working fathers may compare themselves to peers who appear to manage effortlessly. That comparison can push them into spending that preserves dignity or normalcy. It is not always about status in the obvious sense. Sometimes it is about not wanting to feel behind in front of the people around you.

A few behaviors tend to repeat across households:

– buying convenience because the day is already full

– absorbing family costs without noticing the accumulation

– checking balances too late in the month

– underestimating how much routine life actually costs

Once these behaviors are seen clearly, they stop looking like personal failure and start looking like feedback.

What Actually Helps

What helps most is not a dramatic financial makeover. It is creating enough visibility to separate real scarcity from perceived scarcity. When money feels like it disappears instantly, the first goal is to see where it goes in a way that does not require constant effort. A simple budgeting tool or expense tracker can help here, especially one that shows spending by category instead of only showing the final balance.

The second help is timing. Many fathers focus on the total monthly income, but the real pressure is often weekly. If bills cluster too tightly after payday, the account will always feel empty fast. A cash-flow view, even a basic one, can reveal whether the problem is spending, timing, or both. That distinction matters because it changes the solution.

The third help is reducing decision fatigue. When every purchase has to be judged in the moment, the brain gets tired and starts choosing the easiest path. Pre-deciding a few common spending categories, such as fuel, lunch, kids, and household extras, can lower that mental load. It is not about perfection. It is about making routine choices less emotionally expensive.

Another helpful shift is separating necessary spending from stress spending. Necessary spending keeps the household moving. Stress spending soothes the person making the decisions. Both are understandable, but they should not be treated as the same thing. A little awareness here can save a lot of confusion later.

This is also where a calculator can be surprisingly useful. A paycheck calculator, debt payoff calculator, or simple monthly budget calculator can turn vague pressure into something measurable. That does not solve everything, but it makes the pattern harder to deny. And once the pattern is measurable, it becomes easier to change without guessing.

The biggest mistake at this stage is trying to fix the feeling before fixing the structure. The feeling of disappearance is real, but it usually comes from repeated financial motion, not from one bad choice. If the structure is tighter than it looks, the emotions will keep following the structure until something changes.

What To Do Next

Start by watching one full paycheck from arrival to exhaustion. Not forever, just one cycle. Notice what hits first, what repeats, and what disappears without much thought. That single review often reveals more than months of vague frustration.

Then choose one tool that makes the pattern visible. A budgeting app, a simple spreadsheet, or even a basic expense tracker can help you see whether the problem is fixed costs, convenience spending, family leakage, or timing. The best tool is the one you will actually use without resenting it.

If you are a working father who feels like income disappears instantly, do not start by asking what is wrong with you. Start by asking what the money is doing. That shift is calmer, more accurate, and usually more useful. It turns a personal frustration into a solvable pattern.

If you want a practical next step, use a monthly budget calculator or cash-flow tracker and map one paycheck from start to finish. Not to judge it. Just to see it clearly. In money, as in life, what becomes visible becomes easier to change.

Related Reading

- Why Men Over 50 Fear Outliving Their Income

- Why Financial Stress Feels Constant for Men Supporting Families

- Why Working Men Feel Like Their Savings Never Grow

Keep Exploring the Pattern

Watch more breakdowns of real-life money behavior on our YouTube channel.

Browse the full Money Behavior Library to explore more patterns like this one.

If you want a clearer view of where your income goes each month, try the Salary Breakdown Calculator.

Explore more patterns in the Money Behavior Library — a growing collection of real-life financial patterns explained clearly.

Disclaimer:

This content is for educational and informational purposes only and does not constitute financial advice. Always consult a qualified financial professional before making personal financial decisions.