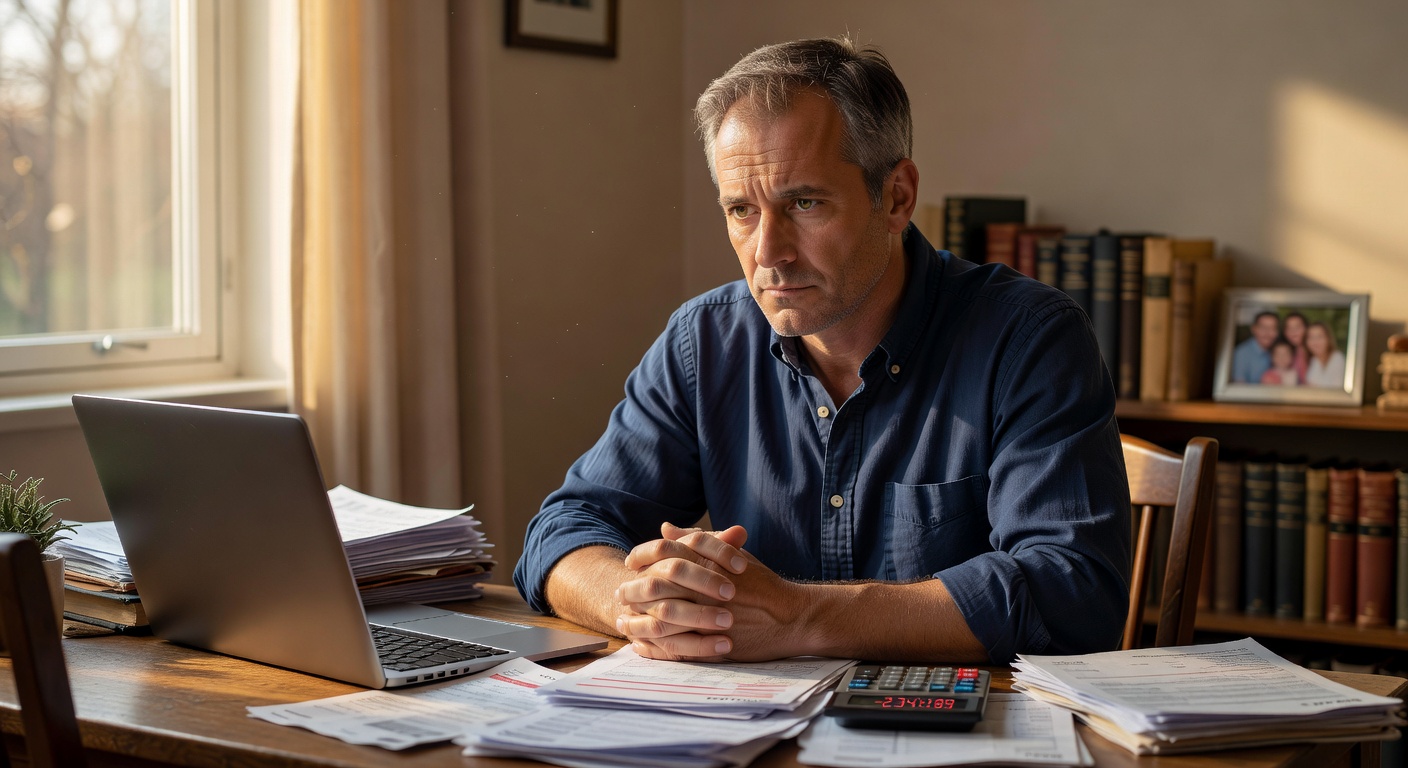

It usually starts on an ordinary afternoon: a bill lands, a car needs something expensive, or a quiet glance at the checking account changes the whole mood. A man who used to feel steady suddenly feels one step behind, and the money itself has not changed as much as the feeling around it has.

Why This Happens

By the time many men reach their 40s, money stops feeling like a simple problem of earning and starts feeling like a problem of pressure. In your 20s and 30s, financial insecurity can still feel temporary, like a phase you are supposed to grow out of. After 40, that same unease can feel heavier because it arrives with more responsibility, more history, and fewer illusions.

The strange part is that the numbers are not always disastrous. Often the income is decent, the job is stable enough, and the life looks reasonably built from the outside. But financial security is not only about numbers. It is also about whether your mind believes the money can handle the next surprise, the next month, the next version of life.

This is where many men feel the shift most sharply. A mortgage, aging parents, school costs, higher insurance, health expenses, and a more expensive everyday life can quietly compress the margin that once created calm. What used to look like progress can start to feel like maintenance.

There is also a deeper emotional layer. For many men, security is tied to being able to absorb problems without visible panic. When the cushion shrinks, even slightly, they do not just feel less wealthy. They feel less protected, less capable, and sometimes less like themselves.

The Hidden Pattern Behind It

The hidden pattern is not simply that expenses rise. It is that life becomes more expensive in exactly the places where people are least prepared to adjust. The extra car repair, the delayed home project, the family emergency, the higher deductible, the adult child who needs help, the subtle support given to a partner or parent — none of these look dramatic alone, but together they erode the sense of control.

Most men do not lose financial security all at once. They lose it in small, repeated experiences of surprise. A balance that used to feel reassuring becomes just enough to get through the month. A paycheck that once felt strong now feels pre-assigned before it even lands.

This is usually where people realize their money is not random. It is patterned. The same stress points appear again and again, and the emotional reaction becomes part of the cycle:

– A bill creates tension.

– Tension creates avoidance.

– Avoidance creates more uncertainty.

– Uncertainty makes the next bill feel bigger than it is.

When that loop repeats long enough, the issue stops being the bill itself. It becomes the anticipation of the bill, and then the anticipation of not feeling ready.

For men over 40, this often connects to identity. If they were raised to equate steadiness with competence, then any sign of wobble feels personal. The account balance is no longer just a number. It becomes a scorecard for whether they are handling adulthood correctly.

That is why financial insecurity at this age can feel confusing. On paper, life may be more established than ever. Internally, though, the nervous system has noticed how thin the margin has become.

Common Mistakes People Make

One common mistake is assuming the problem is laziness or lack of discipline. That framing usually misses the real issue. Many men are not careless with money; they are operating inside a life that has quietly outgrown their old systems.

Another mistake is treating every money concern as a budgeting issue only. Budgeting helps, but it does not explain why a person keeps overspending on the same category after a stressful week, or why a strong earner still feels broke after every major expense. The behavior is often emotional before it is mathematical.

A third mistake is waiting for a larger income to fix the feeling. More money can help, but it does not automatically restore security if spending habits, obligations, and expectations grow at the same pace. Sometimes the relief is brief because the underlying pattern stays intact.

People also make the mistake of measuring security by a single account balance. That can be useful, but it is incomplete. Real security is not only cash on hand. It is the relationship between income, flexibility, debt, emergency capacity, and the ability to absorb surprise without spiraling.

Another subtle mistake is keeping everything private until the pressure becomes unbearable. Men are especially likely to normalize stress and call it normal adulthood. They keep moving, keep paying, keep working, and then wonder why the anxiety never leaves.

Real-Life Patterns and Behaviors

The pattern often shows up in ordinary behavior long before it shows up in a bank statement. A man may know exactly how much is in the account, yet feel reluctant to open the app because he already expects disappointment. Another may check balances constantly during stressful weeks, not because he lacks control, but because he is trying to calm a threat response.

Some men start making more money but feel less secure because their lifestyle expands automatically. The new salary gets absorbed by a better neighborhood, a nicer car, bigger obligations, more frequent spending, or a quiet sense that life should now look a certain way. The money is there, but it never gets the chance to feel like margin.

Others feel insecure because they have become the financial shock absorber for everyone else. They help children, support parents, cover gaps for a partner, or solve household problems without seeing those costs as part of their own budget. From the outside, they are generous. From the inside, they are carrying invisible leakage.

A few common behavioral patterns repeat often:

– Delaying financial check-ins until things feel urgent.

– Using spending to relieve stress after work or conflict.

– Calling irregular expenses “surprises” even when they are predictable.

– Feeling shame after spending, then avoiding the numbers again.

The emotional side matters here. When security feels fragile, people do not always become more disciplined. Sometimes they become more avoidant, more reactive, or more numb. They spend in ways that briefly restore control, then feel worse later when the consequences arrive.

This is why two men with the same income can feel completely different about money. One has built a system that gives him a sense of room. The other has built a life that constantly tests his limits. The difference is often not intelligence. It is pattern.

A budgeting tool or expense tracker can reveal this quickly. Not because the tool fixes anything by itself, but because it shows where money keeps leaving under stress. That visibility matters when the problem is partly psychological and partly structural.

What Actually Helps

What helps most is not a dramatic financial overhaul. It is understanding the repeating pattern well enough to stop mistaking it for personal failure. Once someone sees that their insecurity is tied to pressure points, timing, and emotional reactions, the situation becomes more workable.

The first helpful shift is to separate discomfort from danger. Feeling financially uneasy does not always mean you are in immediate trouble. Sometimes it means your margin is too thin for the life you are living. That is a different problem, and it can be measured.

The second shift is to look for friction points instead of vague guilt. Where does the stress spike? After taxes? Before the mortgage clears? When the car needs attention? When a family member asks for help? The pattern usually lives in repeat moments, not in abstract money beliefs.

The third shift is to give your money some structure before the pressure hits. This does not have to be complicated. A simple cash flow view, a sinking fund for irregular costs, or a basic budget tool can make the month feel less like a series of surprises. The point is not perfection. The point is reducing the number of moments that trigger panic.

It also helps to ask a better question: not “Why am I bad with money?” but “What keeps making this feel unstable?” That question opens the door to behavior, environment, and timing. It makes the problem clearer without making it moral.

Security often improves when people stop treating every expense as proof of failure and start treating their finances as a system that can be adjusted. That is a calmer, more realistic way to work.

What To Do Next

Start by watching your money for one full month without trying to fix everything at once. Notice the moments that create tension, the purchases that follow stress, and the expenses that always seem to arrive as a surprise. A simple tracker or budgeting tool can make those patterns visible faster than memory can.

Then look for the specific gap between what you earn and what actually creates a sense of safety. Sometimes the gap is not income. It is a lack of buffer, too many obligations, or a spending rhythm that never leaves breathing room. A calculator for cash flow or emergency savings can turn that vague feeling into a real number.

If this article feels familiar, that is probably because the pattern already exists in your life. The useful move is not to judge it, but to name it clearly enough that it stops running in the background. Once you can see where the pressure comes from, you can start changing the structure around it.

Take one quiet step: open a budgeting app, review the last 30 days, or estimate your true monthly margin with a simple calculator. The goal is not to become more worried. The goal is to see your money as it is, so it can stop feeling like a mystery.

Related Reading

- Why Men Over 40 Feel Financially Trapped

- Why Men Over 40 Feel Guilty Spending Money

- Why High Earners Still Feel Financially Insecure

Keep Exploring the Pattern

Watch more breakdowns of real-life money behavior on our YouTube channel.

Browse the full Money Behavior Library to explore more patterns like this one.

If you want a clearer view of your monthly patterns, try the Salary Breakdown Calculator, the Subscription Cost Calculator, or the Bill Due Date Planner.

Explore more patterns in the Money Behavior Library — a growing collection of real-life financial patterns explained clearly.

Disclaimer:

This content is for educational and informational purposes only and does not constitute financial advice. Always consult a qualified financial professional before making personal financial decisions.