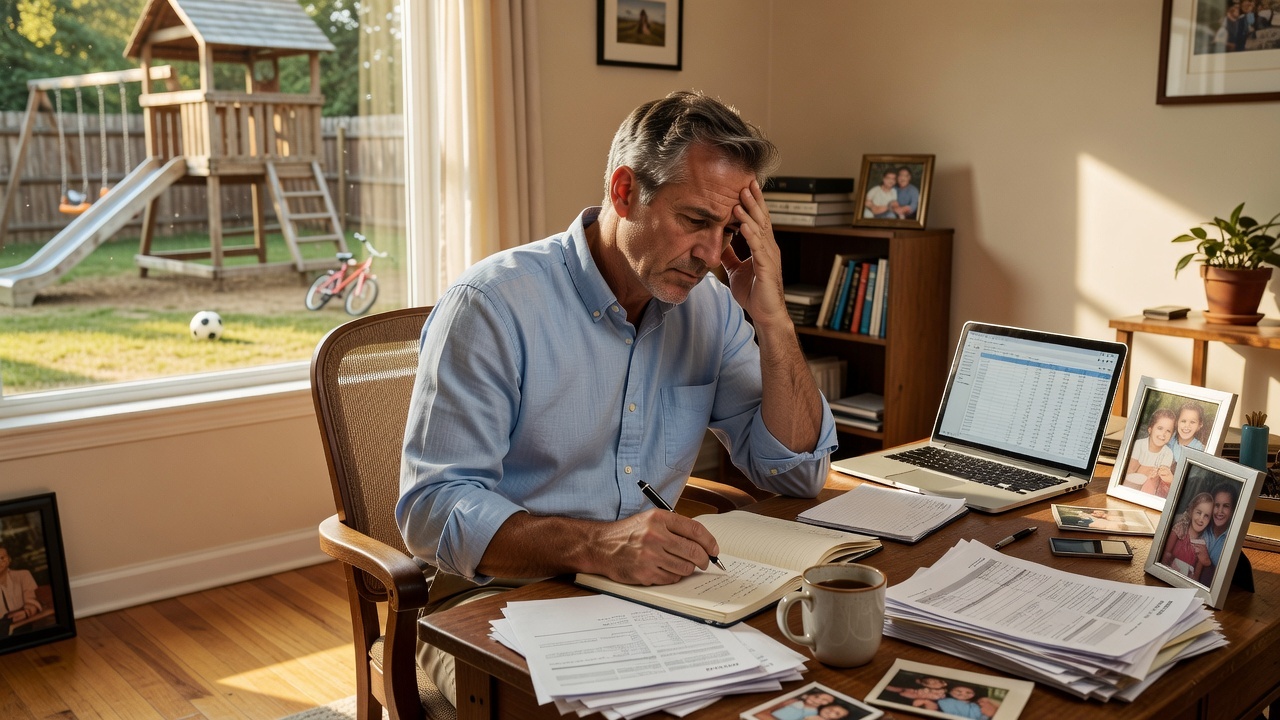

It’s 9:30 p.m., the house is quiet, and he is still answering one more email, checking one more shift, or thinking about one more bill. If you have ever wondered why fathers feel like they can never stop working, the answer is rarely just ambition. More often, it is a money pattern that gets built slowly, then starts running the whole life.

Why This Happens

A lot of fathers do not experience work as a choice once family life gets heavy. It starts to feel like a standing obligation, something tied to safety, identity, and being dependable in a way that never fully turns off. The paycheck matters, of course, but the pressure usually comes from what the paycheck is supposed to protect: rent, groceries, school costs, repairs, insurance, and the quiet fear of letting everyone down.

This is why the question Why Fathers Feel Like They Can Never Stop Working is really a question about pressure loops. Work is not only work anymore; it becomes the emotional proof that things are under control. When money feels tight or uncertain, rest can start to feel irresponsible, even when the body is clearly asking for it.

Many fathers also grew up around a simple script: a good man keeps going. That script is powerful because it sounds practical, even noble. But in daily life, it can quietly train someone to ignore fatigue, delay personal needs, and treat every spare hour like an opportunity to catch up.

The result is not just long hours. It is a nervous system that never fully stands down. Even when the shift ends, the mind keeps scanning for what could go wrong next, and that scanning itself becomes exhausting.

The Hidden Pattern Behind It

The hidden pattern is not simply overworking. It is over-responsibility. A father can begin believing that if he stops moving, the household will wobble, and if the household wobbles, it means he failed. That belief is often stronger than logic, which is why it survives even when the math no longer supports it.

This is usually where people realize their money isn’t random… it’s patterned. The pattern may look like this:

– More work to reduce money stress

– Less rest because work feels urgent

– More exhaustion, which makes planning harder

– More money leaks because tired decisions are expensive

– Even more work to cover the leaks

Once that loop starts, the father is not just earning money. He is managing fear through motion. The body learns that staying busy is safer than sitting still, so stopping starts to feel like danger rather than relief.

There is also a social layer to this pattern. Many fathers do not feel free to say, I am overwhelmed, because they worry that admitting strain will make them look unreliable. So the pressure gets translated into action: another shift, another weekend job, another side hustle, another task no one else asked for but no one else is there to do.

That hidden pattern matters because it changes the question from Why won’t he stop working? to What does stopping seem to mean to him? For many men, stopping does not mean rest. It means exposure.

Common Mistakes People Make

One common mistake is assuming the problem is purely income. Sometimes more money would help, but not always in the way people expect. If the underlying pattern is fear, then every raise becomes temporary relief, not lasting peace. The spending adjusts, the obligations adjust, and the sense of pressure often returns.

Another mistake is treating exhaustion like a character flaw. Fathers are often told to be stronger, more disciplined, or more grateful, as if the issue were a personal weakness. In reality, many are functioning inside a structure that rewards constant availability and punishes pause. That is not a moral failure; it is a predictable result.

A third mistake is trying to fix everything with willpower. Willpower is not a plan when the problem is a repeated behavior loop. If the pattern is check bank balance, feel panic, take extra work, ignore rest, repeat, then the solution has to interrupt the loop, not just scold the person inside it.

People also mistake motion for progress. A father can be very busy and still feel financially trapped. He may be working harder than ever, but if he does not know where the money is going or what each hour is actually buying, the busyness becomes a way of hiding uncertainty.

There is also a common emotional mistake: believing that the family only needs income, not presence. That assumption can keep fathers locked into a model where money comes first because it is measurable, while connection, recovery, and mental clarity get treated like luxuries. Over time, that trade costs more than it saves.

Real-Life Patterns and Behaviors

This pattern usually shows up in ordinary scenes, not dramatic ones. A father checks work messages while eating dinner. He says yes to overtime because next month has a car payment. He picks up an extra weekend shift because the last utility bill made him uneasy. None of these choices look irrational on their own, but together they create a life with no soft edges.

What often gets missed is how money stress changes time perception. When bills feel close and savings feel thin, the future shrinks. The mind stops thinking in seasons and starts thinking in days. That is when rest becomes harder to justify, because every day feels like it could contain a problem.

The behavior can also become self-reinforcing in small, almost invisible ways:

– He delays checking the budget because he expects bad news

– He takes on extra work to avoid feeling behind

– He spends less time planning because he is too tired

– He makes fast decisions because he is always rushing

– He feels guilty resting, then works more to erase the guilt

These are not random habits. They are protective behaviors that have outlived their usefulness. At first, they may have helped him keep the household steady. Later, they become the reason he cannot feel steady himself.

For many fathers, the hardest part is that the behavior looks responsible from the outside. He is providing. He is present in practical ways. He is paying what needs to be paid. But underneath that visible function may be a constant state of financial vigilance, which can make even small interruptions feel threatening.

That is why some men describe themselves as unable to stop, even when they are not technically on the clock. Their mind has converted financial insecurity into a permanent job. They are not only working for income. They are working to stay ahead of anxiety.

What Actually Helps

What helps most is not a dramatic lifestyle overhaul. It is making the pattern visible enough that it stops feeling like destiny. Once a father can see the loop, he can start separating actual financial needs from emotional urgency. That distinction alone can lower the pressure.

A practical money tracker or budgeting tool can help here, not because spreadsheets are magical, but because clarity interrupts panic. When someone can see what is coming in, what is going out, and which expenses are recurring, the mind has less room to invent worst-case scenarios. Even a basic calculator for monthly work hours versus actual take-home pay can reveal whether extra labor is truly helping.

What also helps is naming the real trigger. For some fathers, it is not laziness or poor discipline. It is dread. For others, it is shame about past money mistakes, or fear of becoming a burden, or a deep need to feel indispensable. Once the trigger is named, the response can change from automatic to intentional.

Support matters too, but not in a vague motivational sense. It helps when the household talks about money as a system instead of a moral scorecard. If one person is carrying all the worry, the family often pays for it in silence, tension, and constant urgency. Shared visibility creates shared reality.

This is where gentle tools can be useful in a way that feels almost unremarkable but important. A simple budgeting app, a debt payoff calculator, or a savings goal tracker can reduce the emotional load of remembering everything. The point is not to optimize every dollar. The point is to make money less mysterious so it stops demanding constant mental labor.

Rest also becomes more realistic when it is scheduled and protected like any other obligation. That does not mean pretending the bills are not real. It means recognizing that a completely depleted father is not more productive, only more fragile. A rested mind usually makes fewer expensive mistakes, and that matters more than it sounds.

What To Do Next

If this sounds familiar, do not start by trying to change your whole life in one week. Start by observing the pattern without arguing with it. Ask a few plain questions: When do I feel the strongest urge to keep working? What bill, memory, or fear usually appears right before that urge? What am I trying to protect when I say yes again?

Then make the money visible. Use a budgeting tool, a spending tracker, or a simple calculator to see whether the hours you are adding are actually solving the problem or just feeding the loop. Sometimes one clear number does more than ten stressful thoughts. That kind of clarity can be quietly powerful.

If you want a next step that feels calm instead of overwhelming, pick one: track one week of spending, calculate your real hourly take-home pay, or list the three expenses that create the most pressure. Then stop and look at the pattern before you make the next move. That is usually where real change begins, not in more effort, but in better sight.

Related Reading

- Why Working Men Feel Like Their Savings Never Grow

- Why Fathers Quietly Feel Financially Unappreciated

- Financial Rest Never Comes for Working Fathers

Keep Exploring the Pattern

Watch more breakdowns of real-life money behavior on our YouTube channel.

Browse the full Money Behavior Library to explore more patterns like this one.

If you want a clearer view of your monthly patterns, try the Salary Breakdown Calculator, the Subscription Cost Calculator, or the Bill Due Date Planner.

Explore more patterns in the Money Behavior Library — a growing collection of real-life financial patterns explained clearly.

Disclaimer:

This content is for educational and informational purposes only and does not constitute financial advice. Always consult a qualified financial professional before making personal financial decisions.