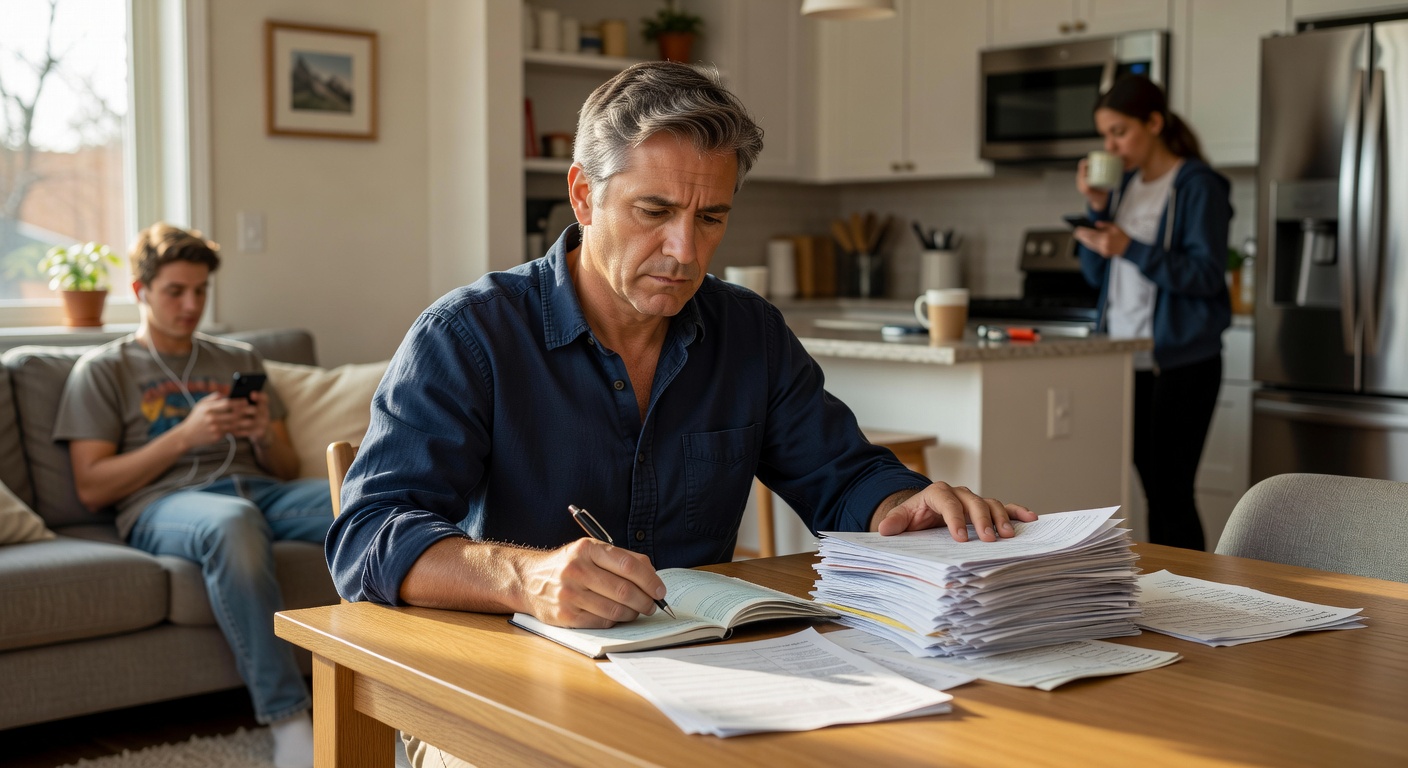

It starts with one more bill, one more emergency, one more “I’ll pay you back next month.” Then the helping becomes part of the family rhythm, until the money feels less like support and more like a leak you can’t find. If you have ever wondered why supporting adult children feels financially endless, it is usually because the pattern is doing more than the numbers admit.

Why This Happens

Supporting adult children often feels financially endless because the money is rarely one single expense. It shows up as rent help, groceries, phone bills, car repairs, co-signing, medical costs, tuition gaps, or short-term rescue after a job change. Each request can seem small enough to justify on its own, which is exactly why the total keeps growing without feeling visible in the moment.

The emotional side matters just as much as the financial side. Many parents do not think, “I am choosing to fund an adult child indefinitely.” They think, “This is temporary,” “They just need help getting through this month,” or “I cannot let them struggle when I can help.” Those thoughts are compassionate, but they also make the support feel morally necessary, which makes it harder to set a limit.

That is why the experience can feel endless even when the intention is generous. The parent is not only paying money; they are also paying to relieve worry, reduce guilt, avoid conflict, or preserve a sense of being a good parent. Once money starts carrying those emotional jobs, the cost becomes harder to measure and easier to repeat.

There is also a real-life timing problem. Adult children often need help during unstable seasons: layoffs, new apartments, debt repayment, childcare gaps, health issues, and career starts that pay less than the cost of living. The need may be legitimate, but if the family never pauses to define the shape of support, the temporary season can quietly become the default system.

This is where people start saying things like, “We’re helping again,” or “It feels like we are always covering something.” That is usually the first sign that the issue is no longer only about cash flow. It is about a relationship pattern that has been repeated often enough to feel normal.

The Hidden Pattern Behind It

The hidden pattern is usually not generosity alone. It is a cycle of rescue, relief, and reset. A parent feels pressure, steps in, the crisis calms down, and everyone breathes again. Then another need appears, and the same emotional script starts over because the last one never created a new structure.

This is why the problem can look different from the inside than it does from the outside. On paper, it may look like a few scattered transfers. In daily life, it feels like being on call. That on-call feeling is what drains people, because the brain never fully relaxes when it expects the next request.

A common hidden pattern is what you could call financial invisibility. If the help is paid in small amounts, through side payments, or by covering shared household costs, it does not feel large enough to count. But repeated invisibility is how a budget gets broken without anyone noticing the break. The money leaves in fragments, not in one obvious decision.

Another pattern is the emotional contract that forms without being spoken. No one may say, “You will keep helping,” but repeated assistance creates that expectation anyway. Adult children often learn the household rule by experience, not conversation, and parents may unconsciously reinforce it by stepping in before the discomfort has time to build.

This is usually where people realize their money isn’t random… it’s patterned. Once the pattern is named, it becomes easier to see why the support feels endless: the need, the guilt, the rescue, and the relief are all feeding one another. The money is not simply leaving; it is being attached to a family role that never really ends.

Common Mistakes People Make

One of the most common mistakes is treating every request like an emergency. Not every need is a crisis, but when the parent feels responsible for the adult child’s stability, the emotional alarm system turns on too fast. That urgency leads to quick decisions, and quick decisions are often expensive decisions.

Another mistake is confusing kindness with absence of limits. Parents sometimes believe that boundaries will feel cold, selfish, or unloving, so they avoid defining them at all. But no boundary usually becomes a blurry, exhausting one, and blurry boundaries are harder on relationships than clear ones.

People also make the mistake of helping in ways that are easier to say yes to in the moment but harder to sustain over time. For example:

– covering a bill instead of discussing a budget

– paying off a balance without changing the spending pattern

– rescuing a shortfall before asking what caused it

– giving money without deciding when it ends

The problem is not the help itself. The problem is when the help is designed to end the discomfort, not to change the pattern. When relief is the main goal, the same financial stress tends to return in a new form.

Another frequent mistake is keeping the support vague. Vague support sounds loving at first, but it often turns into invisible obligation. “Just let me know if you need anything” can quietly become a standing arrangement, especially if nobody revisits what “anything” was supposed to mean.

Real-Life Patterns and Behaviors

In many families, the financial pattern begins with a genuine transition. An adult child moves out too soon, earns less than expected, goes through a breakup, loses a job, or tries to stabilize after a setback. A parent steps in because that is what caring looks like, and in the short term, it often helps everyone feel safer.

The challenge is that repeated help changes behavior on both sides. The adult child may delay tightening spending because there is a backup. The parent may delay reviewing the impact because saying no feels harder than absorbing one more month. Over time, both people can become trapped in a version of the relationship that was never consciously designed.

This pattern often shows up in small emotional moments, not just financial ones. The child may call only when stressed. The parent may feel relief from being needed. Money becomes part of the bond, which means any conversation about limits can feel like a conversation about love, loyalty, or family identity.

That is why the behavior is so sticky. The support can be tied to old parenting instincts, especially if the parent remembers years of sacrifice and still feels responsible for protecting the child from hardship. The adult child, meanwhile, may carry shame, dependence, gratitude, or quiet resentment. Money ends up carrying all of it.

A few repeated patterns often appear:

– help starts after a crisis, then becomes normal

– no one calculates the yearly total

– emotions rise before a budget is discussed

– boundaries are postponed because the timing never feels right

– both people assume the arrangement is temporary, even when it is not

Once these patterns are visible, the problem looks different. It is not simply that adult children need too much. It is that the family has built a financial habit around reacting instead of structuring. That distinction matters, because reacting can feel endless even when the actual numbers are manageable.

What Actually Helps

What actually helps is not harder control. It is clearer structure. Families usually do better when support is named, limited, and reviewed instead of offered in a fog of good intentions. A structure does not remove compassion; it gives compassion a shape.

A good first step is to separate one-time help from ongoing help. Those are not the same thing, even if they feel similar emotionally. One-time help solves a specific problem. Ongoing help becomes part of the household system and should be treated like a line item, even if it is not on a formal budget yet.

This is where a simple budgeting tool or expense tracker can be surprisingly useful. Not because the answer is hidden in an app, but because the app makes the pattern visible. Once the total is visible, people can stop guessing and start deciding. Many families do not need a dramatic solution; they need a clear picture of what is already happening.

It also helps to talk about support in categories instead of vague promises. The difference matters:

– emergency help

– planned monthly help

– shared housing help

– education support

– short-term bridge support

When the categories are separate, the emotional pressure drops a little. You are no longer deciding whether to help in the abstract. You are deciding what kind of help belongs here, how long it lasts, and what condition ends it.

Another helpful move is to notice what emotion triggers the spending. For some parents, it is guilt. For others, it is fear that the child will fail. For others, it is the discomfort of seeing someone they love struggle. The trigger matters because if you do not name it, the trigger will keep making the decision for you.

What To Do Next

Start by looking at the last six to twelve months of support and add it up. Not because you need to judge yourself, but because clarity changes the conversation. A basic calculator, a spending tracker, or a budgeting worksheet can turn a vague feeling into a real number, and that number is often the moment the story changes.

Then ask one calm question: is this temporary help, or is this now part of the family budget? That question matters because it separates crisis support from lifestyle support. If it is temporary, define the end point. If it is ongoing, decide what can be sustained without resentment or financial strain.

If you want a practical next step, use a simple tool to estimate what this support is doing to your monthly cash flow and your yearly savings. Seeing the total clearly can make the next conversation less emotional and more honest. That is often the first real step toward helping without feeling financially endless.

And if you are not ready to change everything yet, that is still information. Sometimes the next step is not a hard boundary; it is simply naming the pattern out loud. Once you can see it, you can stop treating every request like a surprise and start treating your money like a system you are allowed to understand.

Related Reading

- Why Men Over 40 Stop Feeling Financially Secure

- Why Do I Always Feel Financially Stressed? The Pattern

- Why High Earners Still Feel Financially Insecure

Keep Exploring the Pattern

Watch more breakdowns of real-life money behavior on our YouTube channel.

Browse the full Money Behavior Library to explore more patterns like this one.

If you want a clearer view of your monthly patterns, try the Salary Breakdown Calculator, the Subscription Cost Calculator, or the Bill Due Date Planner.

Explore more patterns in the Money Behavior Library — a growing collection of real-life financial patterns explained clearly.

Disclaimer:

This content is for educational and informational purposes only and does not constitute financial advice. Always consult a qualified financial professional before making personal financial decisions.