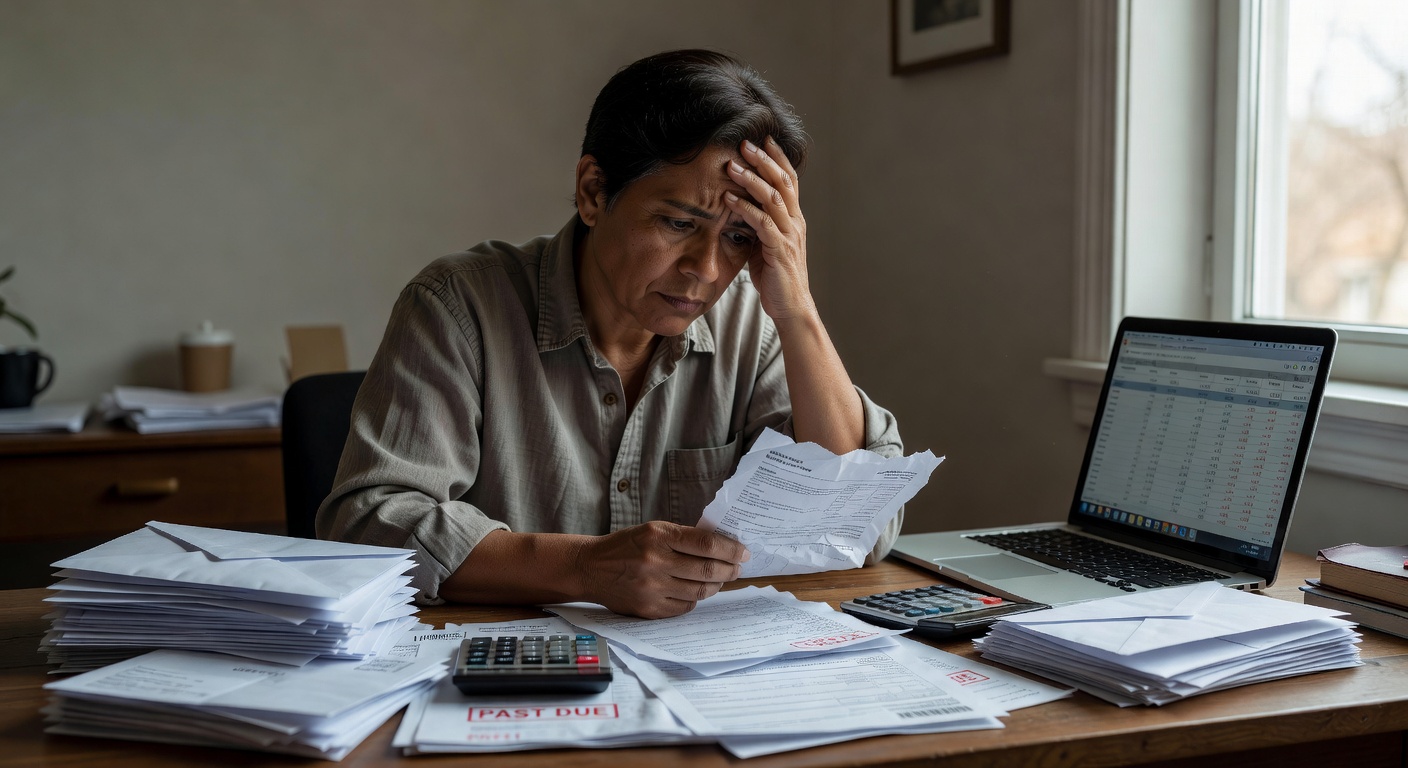

You pay the bill, move money around, and still feel strangely tired afterward. That kind of emotional drain is often the first sign that financial responsibility has stopped feeling like a task and started feeling like a constant pressure.

Why This Happens

Financial responsibility feels emotionally exhausting because it rarely arrives as one clean decision. It shows up as a stream of small judgments: should I spend this, save that, delay this, fix that, or ignore it until next week? For many middle-aged adults, the burden is not just the money itself. It is the mental background noise that never fully turns off.

This is especially tiring when you are the person who is supposed to be dependable. You may be managing a household, supporting children, helping parents, or carrying the memory of financial mistakes from earlier years. The exhaustion comes from being the one who has to notice everything, absorb everything, and make the right call when there is no perfect call to make.

A lot of people assume they are burned out because they are bad at money. In reality, they are often burned out because they are trying to be good at money in a life that keeps asking for flexibility. That tension creates a quiet emotional load. It is not dramatic, but it is constant.

There is also a hidden grief inside financial responsibility. When you become serious about money, you start seeing every choice as a tradeoff. That can feel mature and stabilizing at first, but over time it can become heavy. The fun of spending, the ease of not thinking, and the comfort of avoiding details all disappear at once.

This is where people start asking a question that sounds practical but is really emotional: Why does doing the right thing with money feel so draining? The answer usually has less to do with discipline and more to do with the pressure of sustained self-control.

The Hidden Pattern Behind It

The hidden pattern is that financial responsibility often becomes an identity, not a behavior. Once you see yourself as the responsible one, every mistake feels bigger. Every impulse feels like failure. Every delay feels like character weakness instead of a normal human moment.

That identity pressure creates a loop. You monitor your money more closely, notice more risks, and carry more tension. Then the tension makes it harder to stay consistent, which leads to more monitoring. It is a self-reinforcing cycle that looks like maturity from the outside but feels like exhaustion from the inside.

Another piece of the pattern is decision fatigue. Money asks for repeated choices in areas that are already emotionally loaded. Groceries, subscriptions, school costs, medical bills, gifts, repairs, savings goals, debt payments, and irregular expenses all compete for attention. Even when each choice is small, the total weight is not.

This is usually where people realize their money is not random, it is patterned. They may overspend when they are tired, avoid checking balances after stressful days, or get unusually strict after a big bill. These are not separate failures. They are signals that the nervous system has started attaching emotion to money decisions.

A simple way to see the pattern is this:

– Stress makes money feel urgent.

– Urgency makes people act fast or avoid altogether.

– Fast decisions and avoidance both create later regret.

– Regret increases the emotional cost of the next money decision.

Common Mistakes People Make

One common mistake is treating exhaustion like laziness. People say they need more willpower, more budgeting apps, or a stricter plan. But if the problem is emotional overload, adding more rules can make the situation worse. The person does not need more pressure. They need a system that costs less to maintain.

Another mistake is turning every financial slip into a moral event. A late transfer, a forgotten bill, or an unexpected spending burst can feel embarrassing enough on its own. When people layer shame on top, they do not become more responsible. They become more avoidant. Avoidance usually creates more stress than the original mistake.

People also underestimate how much life stage matters. In your 20s, financial mistakes may feel temporary. In your late 30s, 40s, or 50s, money choices often feel tied to stability, identity, and future security. That shift changes the emotional stakes. The same spending habit can feel harmless at one age and deeply unsettling at another.

Another common mistake is believing that caring more should make the burden lighter. It often does the opposite. The more seriously someone takes their obligations, the more they notice what is missing. They see the gap between what they want to do and what their income, time, and energy actually allow.

The last mistake is trying to solve an emotional pattern with a purely numerical fix. A spreadsheet can tell you what happened, but it cannot tell you why you felt relieved buying something at the end of a hard week. That is why so many budgets fail in real life. They are built for math, not for human behavior.

Real-Life Patterns and Behaviors

Financial exhaustion usually appears in ordinary moments, not dramatic ones. It can show up when you open your banking app and feel a small wave of dread before the numbers even load. It can show up when you know the balance is technically fine, but you still feel like you are one unexpected expense away from losing control.

It also appears in family dynamics. One partner may become the household financial coordinator, while the other assumes the system is working because the bills are paid. The coordinator is often the one feeling the hidden fatigue. They are not just tracking expenses. They are carrying the emotional responsibility of remembering, anticipating, and explaining.

For many people, the pattern looks like this:

– They work hard to be careful.

– They feel deprived or boxed in.

– They eventually overspend or disengage.

– They feel guilty and recommit harder.

That cycle is exhausting because it has no real recovery built into it. It feels like personal failure, but it is often a sign of an unsustainable emotional rhythm. The person is not only managing money. They are managing anticipation, guilt, self-control, and future fear at the same time.

There is also a quiet resentment that can develop. People may resent that financial responsibility never ends, or that being careful does not feel rewarding in the moment. They may look at less careful people and feel a mix of envy and judgment. Underneath both is the same longing: the wish that money could feel lighter without becoming dangerous.

When you start noticing these behaviors, the question changes. It is no longer, Why am I like this? It becomes, What is this pattern trying to protect me from? That question is usually more useful, and much more human.

What Actually Helps

What helps most is reducing the emotional labor around money, not demanding more of it. That begins with making fewer decisions on the fly. A simple recurring system for bills, savings, and regular spending can lower the number of moments that require fresh willpower. Less decision-making means less emotional friction.

It also helps to separate money management from self-judgment. If you only review your finances when something has gone wrong, your brain learns to associate money with threat. A calmer rhythm, even a short weekly check-in, can make the process feel less like an emergency. This is where a basic tracking tool or budgeting tool becomes useful, not because it fixes behavior by itself, but because it removes some of the memory burden.

Another helpful shift is naming the emotional trigger before you act. Some people spend when they feel depleted. Others avoid when they feel ashamed. Others become hyper-controlled after a scare. Once you can name the trigger, the behavior feels less mysterious and more workable.

It can also help to lower the standard from perfect control to stable repetition. Money habits do not need to be impressive to be effective. A system that is boring, predictable, and easy to repeat usually outperforms a system that looks ideal but collapses under stress. Many people discover that consistency is less about intensity and more about friction.

One of the most useful things you can do is build a plan that includes recovery, not just discipline. A budget that allows for ordinary life is less emotionally expensive than one that assumes constant restraint. When people give themselves a realistic buffer for unplanned spending, the whole system tends to feel less punitive.

What To Do Next

Start by noticing where the exhaustion lives. Is it in checking balances, making decisions, talking about money, or recovering from guilt after spending? The point is not to fix everything at once. The point is to identify the part of the pattern that costs you the most energy.

Then look for one recurring money task that could become less emotional. It might be automating a transfer, using a simple calculator to estimate monthly spending, or trying a budgeting tool that shows patterns without forcing daily manual effort. A small system change can sometimes do more than a burst of motivation.

If you want a practical next step, review one month of spending and ask a simple question: where did money feel heavy, and where did it feel automatic? That contrast often reveals the real pressure points. Once those are visible, the problem becomes less personal and more solvable.

You do not need to become harder on yourself to become better with money. In many cases, the real shift comes from understanding the pattern and making it easier to live with. If you are ready, use a budgeting calculator or tracking tool to take one calm look at the numbers, then let the pattern tell you what needs less effort next.

Related Reading

- Why Financial Stress Feels Heavier for Fathers

- Why Financial Pressure Makes Men Emotionally Withdraw

- Why Men Over 40 Stop Feeling Financially Secure

Keep Exploring the Pattern

Watch more breakdowns of real-life money behavior on our YouTube channel.

Browse the full Money Behavior Library to explore more patterns like this one.

If you want a clearer view of your monthly patterns, try the Salary Breakdown Calculator, the Subscription Cost Calculator, or the Bill Due Date Planner.

Explore more patterns in the Money Behavior Library — a growing collection of real-life financial patterns explained clearly.

Disclaimer:

This content is for educational and informational purposes only and does not constitute financial advice. Always consult a qualified financial professional before making personal financial decisions.