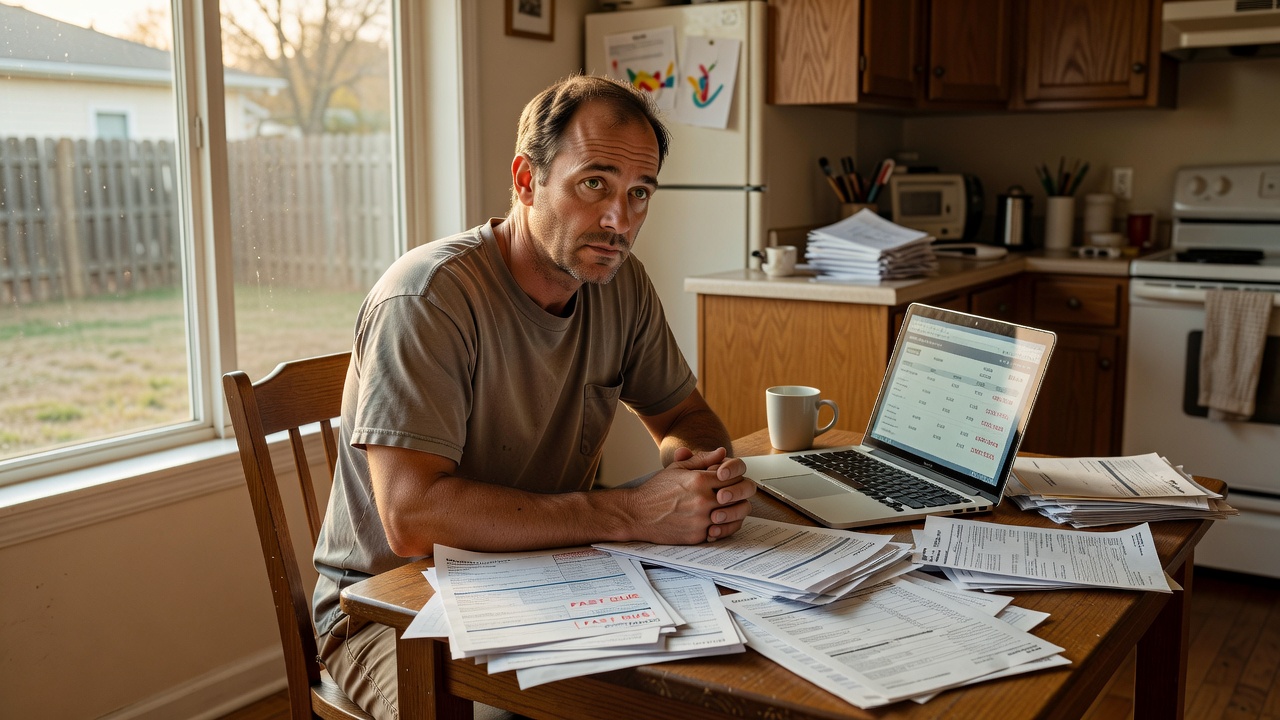

It usually starts with a quiet moment at the kitchen table: the bills are paid, but there is no real breathing room, and one unexpected expense changes the whole mood of the month. If you have ever wondered why middle class fathers feel financially cornered, it is often because the pressure is less about one big mistake and more about a pattern that repeats until it feels normal.

Why This Happens

A lot of middle-class fathers do not feel broke in the dramatic sense. They feel trapped in a narrower and narrower space where every dollar already has a job before it arrives. The paycheck comes in, the obligations line up, and the margin between what is earned and what is owed feels thin enough to tear. That is what makes the pressure so hard to explain to other people, because from the outside it can still look like stability.

The real strain is that middle-class life often asks for proof of success at the same time it demands restraint. You are expected to keep the mortgage current, the car dependable, the children covered, the household moving, and your own stress invisible. The money itself may not be disappearing in one reckless direction. Instead, it is being fragmented into dozens of respectable obligations that quietly leave no room for error.

This is where the feeling of being cornered begins. Not because fathers are always making bad choices, but because their choices are made inside a shrinking set of acceptable options. You can cut expenses, but not too much. You can earn more, but not immediately. You can say no, but then there is the social and emotional cost of saying no.

That is why this experience is so common in financial psychology. People do not only react to numbers. They react to the story those numbers seem to tell about their role, their competence, and their value inside the family.

The Hidden Pattern Behind It

The hidden pattern is not just high spending. It is identity spending under pressure. A middle-class father often feels responsible for keeping the household steady, which can turn ordinary purchases into emotional decisions. The new tires are not just tires. The school activity, the family trip, the upgraded appliance, the work clothes, the practical dinner out after a hard week, all become part of preserving a version of life that feels safe and respectable.

Then there is the invisible math of delayed stress. Many families can absorb a little pressure for a while, so the warning signs do not feel urgent. But the longer the margin stays thin, the more every surprise starts to feel like an attack. One repair turns into a credit card balance. One holiday season turns into a payment plan. One year of holding it together becomes several years of catching up.

This is usually where people realize their money is not random. It is patterned.

The pattern often looks like this:

– earn enough to look fine from the outside

– spend enough to keep the household functioning and everyone else comfortable

– save too little because urgency always arrives first

– feel shame when the numbers do not leave room for rest

That loop is powerful because it is not irrational. It is emotionally understandable. Fathers often delay their own financial relief because someone else always seems to need something more immediate.

Common Mistakes People Make

One common mistake is treating the problem as if it is only about discipline. That framing makes the father the villain, which misses the real structure of the situation. If your life is built around fixed costs, social expectations, and responsibility for other people, willpower alone cannot create margin.

Another mistake is waiting for a crisis before noticing the pattern. When money is tight but not yet catastrophic, people often normalize the discomfort. They tell themselves this is just a busy season, a few expensive months, or the price of being responsible. But if the same pressure keeps returning, it is not a temporary inconvenience. It is a behavioral system.

A third mistake is using short-term relief to avoid long-term adjustment. A credit card swipe, a payment deferral, or a vague promise to tighten up next month can reduce anxiety for a moment. The emotional gain is real. But the future cost grows quietly, and that future cost is what makes the corner feel smaller over time.

Many fathers also underestimate how much social comparison shapes their financial decisions. They may not be trying to impress strangers, but they are often trying not to fall behind peers, siblings, neighbors, or colleagues. The pressure to appear steady can be stronger than the pressure to be financially flexible.

Real-Life Patterns and Behaviors

The most revealing part of this topic is how predictable the behaviors become once you know what to look for. The father who feels cornered usually is not spending wildly on impulse. He is often absorbing everyone else’s needs first and his own second. He may be postponing his own maintenance, avoiding account balances, or making decisions based on the mood of the moment instead of the whole month.

This can show up in small ways that feel harmless at first. He might say yes to a cost because he is tired of arguing. He might keep a subscription or habit because it feels like the last small comfort left. He might agree to a purchase for the family because saying no feels like saying he cannot provide. Over time, these choices form a pattern that is emotionally understandable but financially expensive.

A few repeated behaviors tend to show up again and again:

– checking the account only after spending

– using the next paycheck as a mental cushion

– avoiding full visibility into debt or subscriptions

– treating emergencies as if they are exceptions instead of expected events

The key point is not that these behaviors are careless. It is that they often protect a person from feeling powerless in the short run. The emotional logic is: if I cannot fix everything, I can at least keep things moving. The problem is that movement is not the same as progress.

There is also a deeper emotional layer here. Many fathers are uncomfortable admitting fear around money because fear can feel incompatible with the role they think they are supposed to play. So the fear gets translated into irritability, withdrawal, overworking, or silence. The household may only see the mood, not the pressure underneath it.

What Actually Helps

What helps is not a dramatic personality overhaul. It is getting honest about the pattern at the level where it actually operates. For many middle-class fathers, the real issue is not that they do not care. It is that they care in too many directions at once and have no built-in margin to absorb the cost of that care.

The first useful shift is to make the pattern visible without making it moral. That means looking at where the money goes, but also why it goes there. A budgeting tool can help here, not because the tool solves everything, but because it removes some of the guesswork. When categories are visible, the emotional story gets a little less foggy.

A spending tracker or simple budgeting app can reveal the places where urgency keeps winning. Sometimes that is groceries, sometimes school-related costs, sometimes recurring convenience spending, and sometimes a pattern of saying yes when tired. A calculator can also be useful for seeing what a small monthly surplus or debt payment actually does over time. Those numbers can feel abstract until they are mapped out clearly.

This is also where families often discover that the issue is not one expense category, but timing. Money can look adequate on paper and still feel cornered if everything arrives at once. If bills, repairs, and family costs cluster around the same dates, even a decent income can feel thin.

What tends to help most is not intensity, but clarity. The goal is to reduce surprise. The less surprise there is, the less often the household has to rely on emotional reflexes to make financial decisions.

What To Do Next

If this sounds familiar, the next step is not to judge the pattern harder. It is to name it more accurately. Ask a simple question: where does the pressure actually come from, and what keeps making it repeat? Sometimes that answer is fixed costs. Sometimes it is uneven cash flow. Sometimes it is the habit of covering every need before checking whether the month can really support it.

A practical next move is to review one month of spending with a budgeting tool or calculator and look for the moments where the money gets cornered before it ever reaches savings. Do not look only for waste. Look for pressure points, timing problems, and emotional spending that felt reasonable in the moment. That is often where the real leverage is.

From there, the goal is not perfection. It is building a little more room between income and obligation. Even a small buffer changes the emotional tone of the month. It makes decisions slower, calmer, and less reactive. And once that happens, the feeling of being cornered starts to loosen.

If you want a quiet place to begin, use a simple calculator or spending tracker and follow one full month without trying to fix everything at once. Just see the pattern clearly first. That alone can change the way the next decision feels.

Related Reading

- Why Working Fathers Never Feel Financially Relaxed

- Why Many Fathers Feel Financially Replaceable

- Why Working Fathers Rarely Feel Financially Safe

Keep Exploring the Pattern

Watch more breakdowns of real-life money behavior on our YouTube channel.

Browse the full Money Behavior Library to explore more patterns like this one.

If you want a clearer view of your monthly patterns, try the Salary Breakdown Calculator, the Subscription Cost Calculator, or the Bill Due Date Planner.

Explore more patterns in the Money Behavior Library — a growing collection of real-life financial patterns explained clearly.

Disclaimer:

This content is for educational and informational purposes only and does not constitute financial advice. Always consult a qualified financial professional before making personal financial decisions.