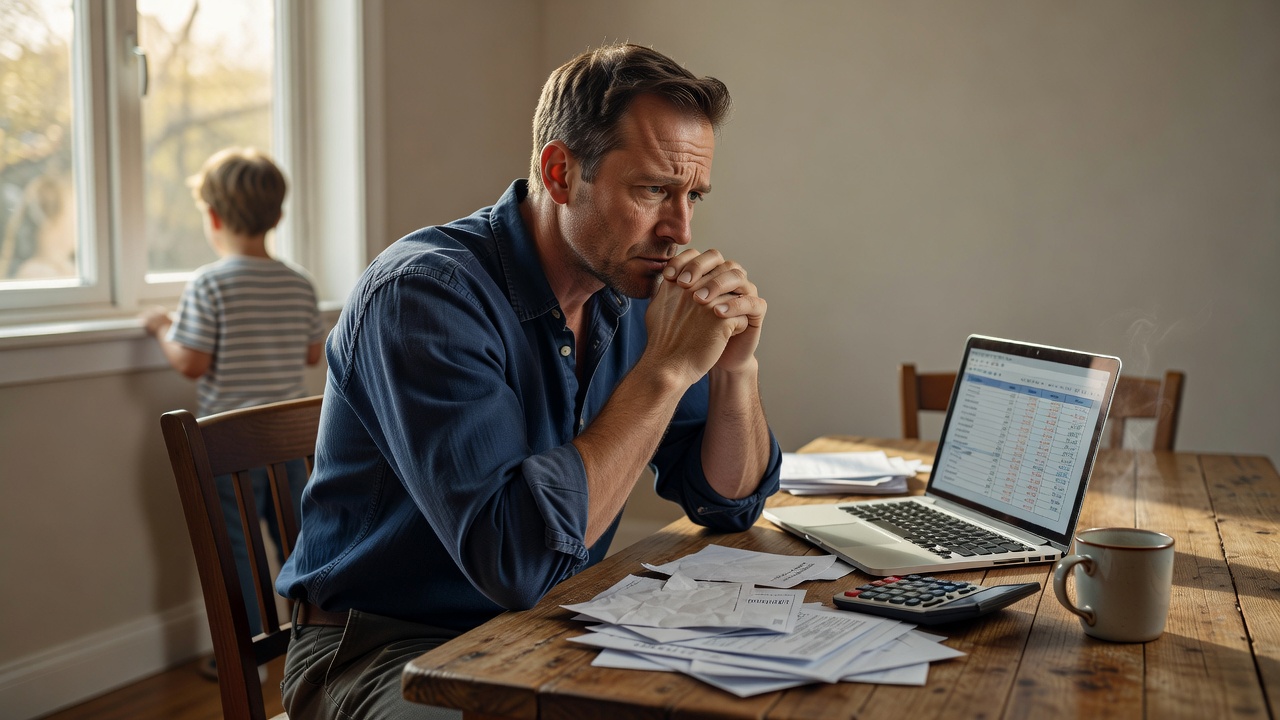

It usually shows up in ordinary moments: the utility bill lands, the car makes a new noise, and a father who is employed, responsible, and doing everything “right” still feels his stomach tighten. That feeling is not always about the number in the bank account. Often, it is about the way money pressure keeps following him, even when life looks stable from the outside.

Why This Happens

Working fathers rarely feel financially safe because their money life is often built around constant anticipation, not actual calm. They are not just paying bills; they are mentally carrying rent, groceries, school costs, repairs, and the invisible cost of being the one who is supposed to keep things steady. When responsibility becomes the identity, every expense starts to feel personal.

That is where the fear gets sticky. Even a decent paycheck can feel fragile when the next month is always waiting to challenge it. A father may know the math on paper, but the body keeps reacting to the memory of bad months, surprise expenses, or the feeling that one mistake could unsettle the whole house. Money safety becomes less about income and more about whether life seems predictable.

For many men, the pressure is also emotional, not just financial. They are often taught to be dependable, solution-oriented, and quiet about stress, which means the anxiety has nowhere clean to go. So it turns into scanning, bracing, overworking, or staying mentally attached to what could go wrong. That is why the question behind why working fathers rarely feel financially safe is rarely about salary alone.

It is usually about the mismatch between what they provide and what they feel they are allowed to need. A father may be earning enough to function, yet still feel one step away from failure. That feeling is hard to explain, because from the outside it looks like stability, but inside it feels like constant exposure.

The Hidden Pattern Behind It

The hidden pattern is that many working fathers confuse financial activity with financial safety. They are busy earning, paying, covering, and fixing, but they do not always build the kind of structure that makes money feel contained. Income enters, obligations spread, and there is little space for the mind to settle.

This creates a familiar loop. A paycheck arrives, bills get handled, a few urgent things get addressed, and whatever is left is too small to feel protective. Then the next expense appears, and the nervous system resets to alert mode. The pattern is not incompetence; it is chronic reactivity.

You can usually spot this pattern in a few ways:

– Money is always being assigned before it has time to sit still

– Savings are treated as leftover money instead of planned protection

– Any surprise cost feels bigger than it should

– The father keeps asking himself whether he is “doing enough”

This is usually where people realize their money is not random; it is patterned. If every month feels like a recovery mission, the problem is not just the budget. The problem is that the budget never gets to become a system the mind can trust.

There is also a deeper pattern around control. Some fathers try to solve anxiety by working more, watching every dollar, or avoiding spending on themselves entirely. But the more they tighten around money, the more money starts to feel scarce. Safety cannot grow in a system that only knows pressure.

Common Mistakes People Make

One common mistake is assuming financial safety comes from income alone. More money helps, but if spending, saving, and planning remain emotionally reactive, the feeling of safety still does not arrive. A bigger paycheck with the same nervous system often creates the same fear in a larger container.

Another mistake is waiting for a perfect month to start feeling organized. Many fathers tell themselves that once the debt is lower, once the car is replaced, or once work settles down, then they will finally feel calm. But life rarely clears itself completely, so the emotional pattern stays in place while the deadlines keep coming.

A third mistake is treating every financial tension as a personal failure. That mindset turns ordinary stress into shame, and shame makes people avoid looking closely at the numbers. Avoidance is expensive because it lets uncertainty grow in the dark. The longer the situation stays vague, the more dangerous it feels.

There is also the habit of overcommitting to the role of provider. Some fathers say yes to every need because they do not want to disappoint anyone, then quietly resent the pressure later. That resentment often shows up as burnout, secrecy, or the sense that money is always disappearing faster than it should.

The real issue is not that they are careless. It is that they are trying to meet emotional, family, and financial demands with a system that was never designed to give them relief. Without a structure that reflects real life, even responsible choices can feel exhausting.

Real-Life Patterns and Behaviors

The pattern often begins before the paycheck even lands. A father may already be mentally spending the money on the bills he knows are coming, which means he never experiences income as breathing room. The money arrives with instructions attached, and the day becomes a countdown instead of a reset.

Another common behavior is delayed self-checking. He may avoid looking too closely at account balances because he already expects bad news, or because he cannot tolerate another reminder of how tight things are. That avoidance can create a strange disconnect: he is handling money all month without ever feeling in contact with it.

This is also where emotional spending or compensatory spending can appear, even in very responsible households. It might not be flashy; it might be a tool purchase, a convenient upgrade, a meal out, or a small escape after a hard week. The purchase is not always about the item. Sometimes it is about a brief feeling of control, relief, or being human again.

Working fathers also tend to normalize depletion. They get used to saying things like “we are fine,” while privately carrying the fear that they are not. When exhaustion becomes routine, financial safety starts to feel like a story other people get to live in. That distance can make even solid finances feel emotionally unavailable.

What matters here is the repetition, not the drama. If the same tension appears every payday, every unexpected bill, or every time a child needs something new, then the behavior is telling a story. The story is usually: I can keep this going, but I do not feel protected while doing it.

What Actually Helps

What helps most is not a dramatic financial overhaul. It is creating enough predictability that the nervous system stops treating money like a moving target. A simple budget that reflects real spending patterns often does more for safety than a complicated plan that looks impressive but never survives daily life.

A savings buffer matters, but not only because of the dollars. It matters because it interrupts the pattern of immediate reactivity. Even a modest emergency fund can change the emotional script from “something is about to break” to “we have time to respond.” That shift is small on paper and enormous in the body.

Tracking tools can be useful here, especially ones that show timing, category drift, and recurring pressure points. A basic budgeting app, a spreadsheet, or a bill tracker can reveal where the fear is coming from: uneven spending, irregular obligations, or a month that is technically affordable but emotionally overloaded. A calculator can also help with debt payoff or savings goals when the mind keeps guessing instead of seeing.

The point is not to micromanage every dollar. It is to make the money visible enough that it stops feeling mysterious. When people can see the pattern, they usually stop blaming themselves for a feeling that was never only about self-control.

And this is where the emotional work matters too. If a father only responds to financial stress by pushing harder, he may keep the household afloat while never actually feeling safe. The healthier shift is to pair practical structure with permission to notice stress without turning it into identity.

What To Do Next

The next step is to get honest about which part of the pattern is actually hurting the most. For some fathers, it is cash flow timing. For others, it is debt pressure, irregular expenses, or the emotional habit of treating every setback like proof that they are behind. Once the real pressure point is named, the numbers stop feeling like a blur.

Start with one calm review of the last 30 to 60 days instead of trying to fix the whole year. Look for recurring shortages, surprise expenses, and the moments when anxiety spikes. A simple cash flow tracker or budget calculator can help you see whether the issue is income, timing, overspending, or just too many demands arriving at once.

If this feels familiar, do not rush past it. The goal is not to become a perfect planner overnight. The goal is to build a money system that gives your mind fewer reasons to stay on alert. That is usually how financial safety begins: not with a fantasy of control, but with a pattern you can finally see clearly.

If you want the next step to feel manageable, use one tool this week: a budgeting app, a debt calculator, or a simple spending tracker. Keep it small, keep it honest, and let the data tell the story before your stress does.

Related Reading

- Why Working Fathers Never Feel Financially Relaxed

- Why Many Fathers Feel Financially Replaceable

- Why Older Working Men Feel Stuck Financially

Keep Exploring the Pattern

Watch more breakdowns of real-life money behavior on our YouTube channel.

Browse the full Money Behavior Library to explore more patterns like this one.

If you want a clearer view of your monthly patterns, try the Salary Breakdown Calculator, the Subscription Cost Calculator, or the Bill Due Date Planner.

Explore more patterns in the Money Behavior Library — a growing collection of real-life financial patterns explained clearly.

Disclaimer:

This content is for educational and informational purposes only and does not constitute financial advice. Always consult a qualified financial professional before making personal financial decisions.