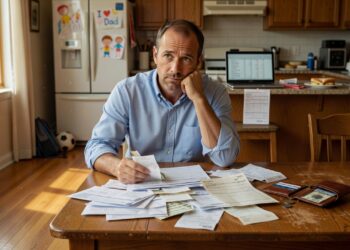

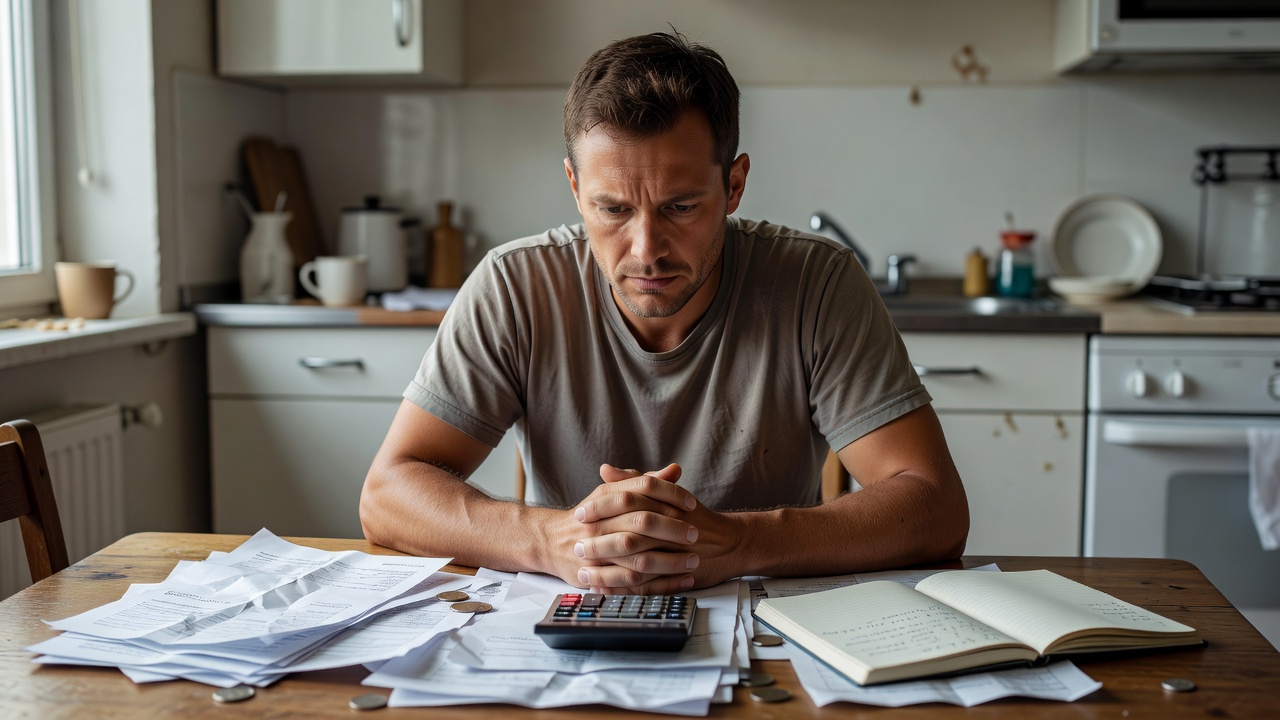

You get home, drop your keys by the door, and the numbers are already waiting for you. The mortgage, groceries, school costs, gas, repairs, and the quiet pressure of being the one who keeps it all moving can make financial stress feel constant for men supporting families.

Why This Happens

What makes this kind of stress feel endless is that it is rarely caused by one big mistake. It usually comes from a steady collision between responsibility, uncertainty, and the feeling that your margin is always too thin. When a man is supporting a family, money is no longer just money; it becomes proof of stability, protection, and sometimes self-worth. That is why even a normal month can feel heavy.

A lot of men are not reacting to the size of a bill as much as they are reacting to what the bill represents. A tire replacement is not just a tire replacement. It is another reminder that the system is fragile and that one unexpected expense can knock the whole month off balance. The stress becomes constant because the mind keeps scanning for the next problem before the current one has even passed.

This is also why financial stress often feels louder at night, after work, or in the quiet moments when nobody is asking for anything directly. During the day, there is movement and purpose. At night, the numbers speak more clearly. That shift from action to reflection can make the same financial reality feel twice as heavy.

For many men, the pressure is intensified by a simple but powerful belief: if I am the provider, I should be able to handle this. That belief can be admirable, but it can also become a trap. It turns ordinary strain into private failure, even when the actual issue is a mismatch between income, obligations, and the cost of everyday life.

The Hidden Pattern Behind It

The hidden pattern is not just spending more than you should. It is living in a state where every decision feels like it has consequences for everyone else. That changes the emotional math. Instead of asking, What can I afford? many men are asking, What will happen to my family if I get this wrong? That question keeps the nervous system activated.

Once that pattern starts, it repeats itself in small ways. You delay checking accounts because you do not want the feeling. Then the account gets checked under stress. Then you notice how close things are. Then you promise yourself you will be more careful next week. The problem is not only the money; it is the cycle of avoidance, dread, and sudden attention.

This is usually where people realize their money isn’t random… it’s patterned. The same kind of week creates the same kind of behavior: a small purchase for relief, a little postponement on planning, a quick internal calculation, then guilt. None of it looks dramatic from the outside, but over time it shapes the whole financial experience.

A common pattern looks like this:

– Income arrives, and pressure briefly drops

– Necessary bills are covered, but not much else

– Unexpected expenses create immediate anxiety

– The month becomes a countdown instead of a plan

Once money starts feeling like a countdown, stress becomes self-renewing. Every choice is made under the shadow of the next one. That is why even men who are technically making enough may still feel like they are barely surviving. The hidden burden is not only the cash flow. It is the constant mental load of keeping the household from tipping.

Common Mistakes People Make

One of the most common mistakes is treating the stress as a personal weakness instead of a pattern to observe. When that happens, men often push harder, cut harder, or stay silent longer. They try to be tougher about it, but toughness does not solve a system that keeps producing the same result.

Another mistake is waiting for a perfect month to get organized. There is always something happening: a school fee, a repair, a medical bill, a gift, a holiday, a gap in income. If the standard for acting is a calm month, the work never starts. The result is that stress remains emotional instead of becoming visible.

A third mistake is confusing short-term relief with actual stability. A delivery dinner, a purchase, or a weekend decision can feel justified because it gives the mind a break. And sometimes it does. But if relief spending becomes the only pressure valve, it quietly widens the gap between what is coming in and what life is asking for.

Men also often make the mistake of carrying the problem alone for too long. Not because they want to, but because they believe talking about money will add shame, conflict, or worry. In reality, silence usually increases uncertainty, and uncertainty is one of the fastest ways to intensify financial stress. The issue grows larger in private than it does in conversation.

Another common error is thinking in monthly snapshots instead of behavioral patterns. A good paycheck can hide a weak system. A bad month can hide a strong one. Without a consistent view, people keep judging themselves by the latest number instead of the recurring behavior that creates the number.

Real-Life Patterns and Behaviors

In real life, this stress often shows up in very specific behaviors. A man may be the first to say yes to family needs and the last to spend on himself. He may know the numbers in his head but avoid writing them down because writing them makes the pressure feel real. He may work hard all day and still feel behind because the mental load does not disappear when the shift ends.

The pattern often includes emotional over-responsibility. That means carrying not just your part, but the imagined future of everyone else too. You start factoring in school clothes, car maintenance, household repairs, and possible emergencies before they happen. This can create an exhausting state where even good news feels temporary.

There is also the quiet habit of making money decisions from fatigue. When someone is tired, every choice gets shorter and more emotional. The grocery run becomes less planned, the subscription stays because canceling feels like another task, the debt payment gets thought about but not revisited. Fatigue does not just drain energy; it reshapes behavior.

A few patterns tend to repeat:

– Checking balances only after spending

– Delaying conversations about money until there is a problem

– Feeling calm right after payday, then tense by midmonth

– Overworking to create safety, then spending less time noticing the system

These are not random flaws. They are signs that money has become emotionally loaded. And once money is emotionally loaded, every decision carries more weight than it should. The family may see a provider. The provider often feels like a pressure point.

What Actually Helps

What helps most is not a dramatic transformation. It is making the pattern visible enough that it stops feeling mystical. A simple budgeting tool or tracking app can help here, not because it solves stress by itself, but because it turns vague pressure into a shape you can look at. Once the pattern is visible, it becomes easier to stop blaming yourself for every hard month.

A cash flow calculator can be especially helpful for men who feel like they are constantly reacting. It shows where the pressure actually lands, and sometimes that is the first honest moment a household has had in months. The goal is not to create a perfect budget on day one. The goal is to stop guessing.

Another thing that helps is separating fixed responsibility from emotional responsibility. Fixed responsibility is real: rent, utilities, food, transportation, debt payments. Emotional responsibility is the extra burden of believing you must personally absorb every problem without support. The first one needs planning. The second one needs perspective.

Helpful shifts often look small from the outside, but they change the pattern underneath:

– Track the same five categories every week

– Notice when stress peaks during the month

– Identify which spending happens from relief, not need

– Use a budgeting tool before the month feels urgent

This is where behavior matters more than motivation. Motivation rises and falls. Patterns keep repeating unless something visible interrupts them. A tracking tool, a debt calculator, or a simple family budget sheet can create that interruption without turning money into a moral issue.

Most importantly, help works better when it reduces shame. Shame makes people hide numbers, delay decisions, and exaggerate failure. Clarity does the opposite. It creates a more honest relationship with the month, which is often the first step toward feeling less trapped by it.

What To Do Next

If this feels familiar, do not start by trying to fix everything. Start by looking at the pattern you repeat most often. Ask yourself when the stress spikes, what you usually do next, and whether that reaction is solving the problem or just softening it for a moment.

Then choose one tool that gives you a clearer view. A budgeting app, a simple spending tracker, or a cash flow calculator can make the month less foggy. If you share responsibilities with a partner, a short money check-in can help more than a long, emotional conversation that never gets to the numbers.

The point is not to become perfect with money. The point is to stop letting the same pattern run your week without being named. Once you can see it, you can work with it instead of living inside it.

If you want a quieter next step, use a calculator or tracking tool this week and look at one full month at a time. Not to judge it. Just to understand it. That kind of clarity is often where pressure starts to loosen.

Related Reading

- Why Men Over 50 Feel Financially Uncertain About the Future

- Why Men Over 40 Quietly Worry About Inflation

- Why Men Quietly Fear Running Out of Money Eventually

Keep Exploring the Pattern

Watch more breakdowns of real-life money behavior on our YouTube channel.

Browse the full Money Behavior Library to explore more patterns like this one.

If you want a clearer view of where your income goes each month, try the Salary Breakdown Calculator.

Explore more patterns in the Money Behavior Library — a growing collection of real-life financial patterns explained clearly.

Disclaimer:

This content is for educational and informational purposes only and does not constitute financial advice. Always consult a qualified financial professional before making personal financial decisions.