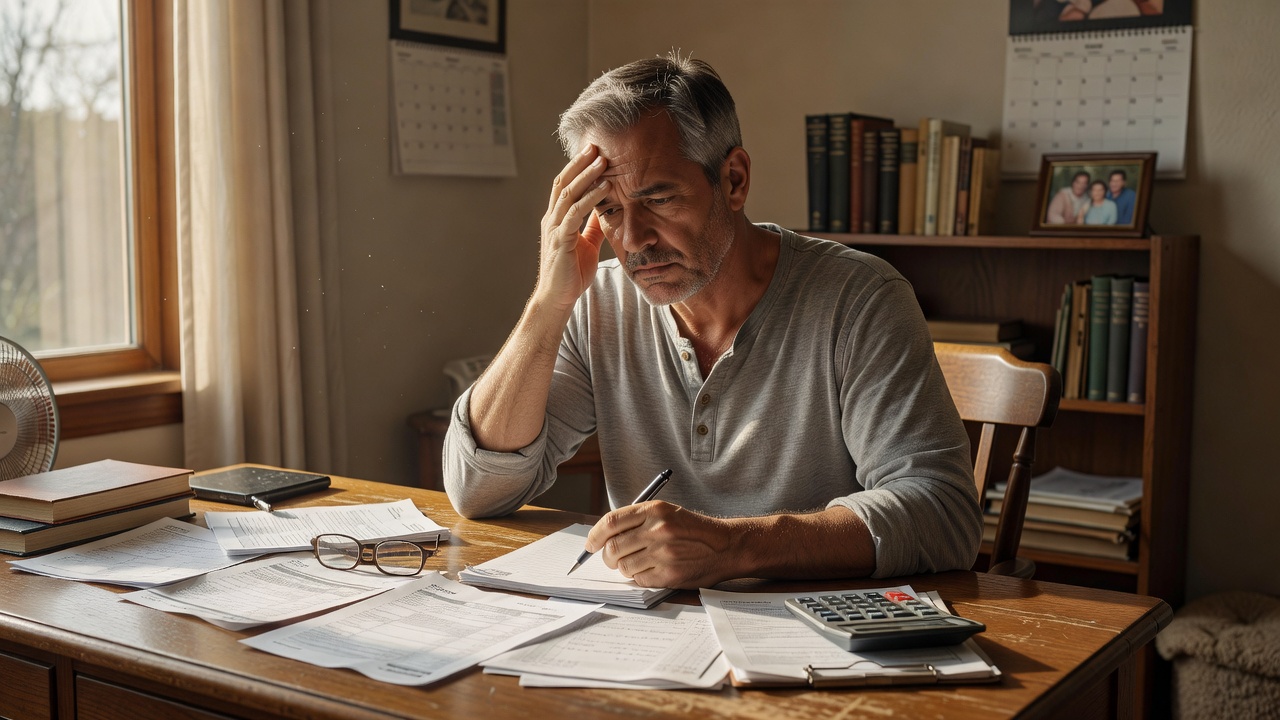

You check the balance, look at the retirement account, then quietly do the math again in your head. Why men over 50 feel financially uncertain about the future is often less about one bad number and more about the slow feeling that the rules changed while life was already in motion.

Why This Happens

The uncertainty usually starts in ordinary places, not dramatic ones. A medical bill arrives, a promotion never comes, a child still needs help, or a partner says the word retirement and it suddenly feels less like a milestone and more like a test. For many men over 50, money stops feeling like something they manage and starts feeling like something that can expose them.

That shift matters because financial uncertainty is rarely only about cash. It is about identity, timing, and the pressure of being the one who is supposed to have it figured out by now. When the future looks less predictable than the past, the mind does what it always does under stress: it scans for risk, replays old decisions, and assumes the worst when information is incomplete.

There is also a simple reality that does not get talked about enough. At this stage of life, the margin for error can feel smaller. You may be earning more than you did at 35, but the runway is shorter, the responsibilities are heavier, and the stakes feel louder. A financial mistake at 28 feels recoverable. The same mistake at 54 can feel like a warning.

That is why so many men describe the future as uncertain even when the numbers are not collapsing. The feeling is often out of proportion to the spreadsheet, but it is still rational in a human sense. It comes from living inside a changing system, where income, health, family needs, and retirement expectations all move at the same time.

The question underneath the question is usually not, “Do I have enough?” It is, “What if the life I planned is not the life I get?” That is real financial psychology, and it explains why search phrases like “why am I worried about retirement” or “how do I know if I can retire” are so common. People are not only looking for facts. They are looking for a feeling they can trust.

The Hidden Pattern Behind It

The hidden pattern is that uncertainty grows when money becomes harder to read. At younger ages, progress is visible in simple ways: more income, fewer obligations, a clearer ladder. After 50, the signals get mixed. Savings may be higher, but debt may linger. Home equity may look strong, but cash flow may feel tight. The numbers can say one thing while daily life says another.

This creates a strange emotional loop. You may appear stable from the outside, yet internally feel one setback away from trouble. That feeling is often fed by comparison. A friend retires early. A coworker sells a business. Someone online talks about passive income as if it arrived naturally. Suddenly your own path feels slower, even if it is healthy and real.

Another pattern is that men often confuse control with certainty. If you have spent decades solving problems by working harder, delaying decisions, or staying composed, uncertainty can feel like failure. But money in this stage of life is not just about effort. It is about timing, health, market performance, family obligations, and the decisions other people make around you.

This is usually where people realize their money isn’t random; it’s patterned. The anxiety is often not triggered by the balance itself, but by recurring situations:

– Income feels strong, but spending rises with it.

– Savings exist, but they are not clearly assigned.

– Retirement feels important, but distant enough to ignore.

– Debt is manageable, but emotionally unfinished.

When these patterns repeat, the brain starts predicting stress before the stress arrives. That prediction becomes the feeling of uncertainty. It is not just fear of a number. It is fear of the next surprise.

The hidden pattern also includes silence. Many men over 50 do not talk openly about money unless there is a crisis. They may discuss markets, housing, or taxes, but not the private feeling of being behind, unclear, or underprepared. That silence creates a gap between what is known and what is felt, and in that gap uncertainty grows.

Common Mistakes People Make

One of the most common mistakes is checking the wrong number for reassurance. People look at a retirement account balance and expect comfort, but the account is only one part of the story. If monthly expenses, debt payments, health costs, and income stability are not part of the picture, the balance can create false confidence or false panic.

Another mistake is treating uncertainty like a motivation problem. Men often respond to discomfort by promising themselves they will get stricter, work more, or “finally get serious.” That can help briefly, but it misses the deeper issue. If the real problem is a lack of clarity, then more pressure does not create clarity. It usually creates avoidance.

A third mistake is assuming that a good income should eliminate anxiety. This belief is common and quietly damaging. High earners can feel just as uncertain as moderate earners if their lifestyle expanded faster than their planning. In those cases, the money is not disappearing; it is simply being absorbed by obligations that never got named.

People also make the mistake of thinking they need a perfect answer before they can act. They want to know exactly when they can retire, exactly how much they need, and exactly what the future will cost. But financial life is rarely that precise. Waiting for certainty can become a way of postponing the one thing that would reduce uncertainty: a plain, honest look.

Sometimes the mistake is emotional, not mathematical. A man may avoid looking at the full picture because he does not want to confirm what he suspects. That avoidance is understandable, but it keeps the feeling alive. The longer money stays vague, the more it grows into something larger than it is.

Real-Life Patterns and Behaviors

The daily pattern is often easy to recognize once you know what to look for. A man feels uneasy, checks accounts, gets a small burst of relief, then stops looking again. A month later, the same concern returns. The problem was never solved; it was temporarily soothed. That is one reason the worry keeps coming back.

Another pattern is the “I’ll handle it later” reflex. It sounds harmless, but it usually means the financial question is being emotionally postponed. Maybe the person knows the retirement accounts need review, or the will still needs attention, or the budget has never matched reality. The delay is less about laziness than discomfort.

Many men also drift into what could be called silent adaptation. They reduce spending without labeling it, avoid risk without explaining it, or keep working because the idea of stopping feels more frightening than the workload itself. On the surface, this can look responsible. Inside, it often feels like resignation.

The behavior tends to follow a predictable cycle:

– Something feels uncertain.

– The person checks or avoids checking.

– Relief appears briefly.

– The underlying question returns.

– More emotional distance gets added.

This cycle can run for years. It is why some men say they are “fine” while quietly feeling unsettled every time they think about the future. The feeling is not dramatic enough to call a crisis, but it is strong enough to shape choices.

In real life, this shows up in spending too. Some men tighten up aggressively after a financial scare, then loosen up once the discomfort fades. Others spend to keep life feeling normal, especially if retirement or aging feels like loss. Both behaviors are attempts to regulate emotion through money.

And then there is the role of responsibility. Men over 50 are often carrying overlapping roles: provider, parent, partner, caregiver, employee, business owner, or all of the above. When those roles stack, the future becomes uncertain not because money vanished, but because too many obligations are making claims on it at once.

What Actually Helps

What helps most is not a dramatic financial overhaul. It is a clearer relationship with the numbers you already have. When people move from vague worry to specific visibility, the emotional tone changes. A retirement calculator, a spending tracker, or a simple cash flow tool can turn a cloud into a map.

That matters because uncertainty feeds on generality. “I am not ready” feels heavier than “I need to understand monthly expenses, debt payoff timing, and income sources.” The second version is still serious, but it is workable. Specific questions create specific actions, and specific actions reduce the feeling of helplessness.

It also helps to separate fear from facts. Not every anxious thought is a prediction. Sometimes it is just a memory of past stress trying to protect you from future stress. When you notice the same worry returning, ask whether the concern is about a number, a habit, or an old story about what money means.

Another helpful shift is to stop measuring progress only by net worth. For many men, that number becomes emotionally loaded and misleading. A better view includes monthly stability, debt pressure, flexibility, expected expenses, and whether the future has enough room for surprises. That broader view often explains why someone feels unsafe even when they have assets.

Practical tools can support this without turning life into a project. A budgeting tool, a debt payoff calculator, or a retirement income estimator can make a private fear visible enough to work with. The value is not in perfection. It is in replacing guesswork with a clearer pattern.

Most importantly, people tend to feel calmer when they stop asking, “Am I doing enough?” and start asking, “What exactly is unfinished?” That question is less emotional and more useful. It turns anxiety into a list, and a list is something a person can actually work through.

What To Do Next

If this feels familiar, do not start by trying to fix everything at once. Start by naming the part that feels unclear. Is it retirement timing, debt, spending, health costs, or the fear of not being able to support others the way you once did? Clarity begins when the worry gets a shape.

Then look at one small piece of the picture with a tool that matches the problem. If the uncertainty is about retirement, use a retirement calculator. If it is about day-to-day tension, use a budgeting tool or a spending tracker. If it is about debt, use a payoff calculator that shows the timeline instead of the shame.

The point is not to become obsessed with numbers. The point is to stop letting vague fear do all the talking. Once the pattern is visible, it becomes easier to decide what is actually urgent and what is just emotional noise.

If you want a calmer next step, choose one tool and spend 15 minutes with it this week. Not to solve your whole future, but to make it less blurry. That is often where real financial confidence begins: not with certainty, but with a clearer view of what is already true.

Keep Exploring the Pattern

Watch more breakdowns of real-life money behavior on our YouTube channel.

Browse the full Money Behavior Library to explore more patterns like this one.

If you want a clearer view of your monthly patterns, try the Salary Breakdown Calculator, the Subscription Cost Calculator, or the Bill Due Date Planner.

Explore more patterns in the Money Behavior Library — a growing collection of real-life financial patterns explained clearly.

Disclaimer:

This content is for educational and informational purposes only and does not constitute financial advice. Always consult a qualified financial professional before making personal financial decisions.