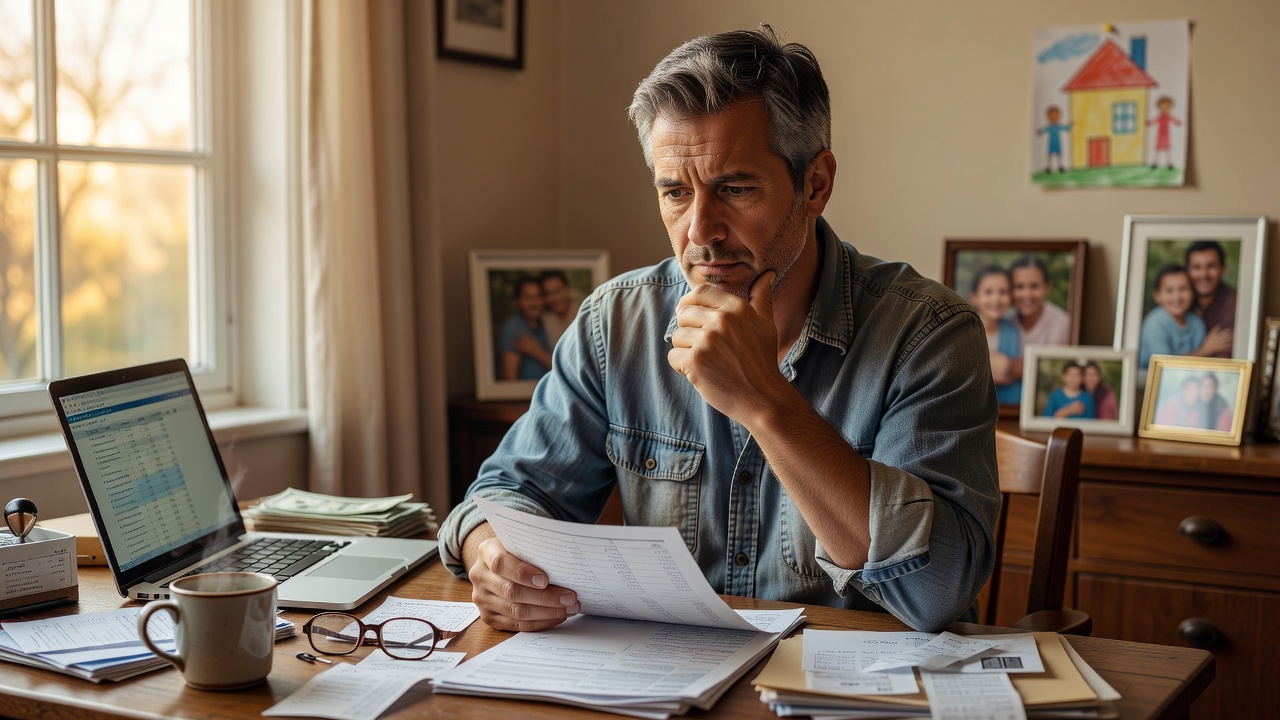

It is a familiar kind of silence: a father checking the bank balance before saying yes to dinner, a school trip, or a repair that cannot wait. What looks like hesitation is often financial worry moving quietly through every decision, long before anyone names it.

Why This Happens

A lot of fathers do not carry money stress out loud. They carry it in timing, in tone, and in the small pauses before they agree to anything. They may still look steady on the outside, but inside they are scanning every decision for hidden risk. That is why a simple purchase can feel bigger than it should.

For many men, financial responsibility became tied to identity long before adulthood arrived. Being dependable was praised, while uncertainty was something to hide. Over time, that creates a habit where money decisions are not just practical choices. They become quiet tests of whether a father is still doing his job well.

This is not always about being broke. Sometimes the income is enough on paper, but the worry remains because the mind has learned to expect interruption. One unexpected bill, one layoff in the past, one season of debt can train the nervous system to stay alert. Then every decision starts to feel like the first domino.

That is why fathers often say yes too late, no too quickly, or maybe after too much mental arithmetic. They are not being difficult. They are trying to protect the household from a future they have already imagined. The worry is less about the purchase itself and more about what the purchase might represent.

A parent may spend hours comparing prices for something small, then ignore a much larger emotional cost, like burnout or resentment. That mismatch is part of the pattern. Money worry narrows attention until the father becomes more focused on preventing loss than on creating stability.

The Hidden Pattern Behind It

The hidden pattern is not just caution. It is responsibility becoming overactive. When a father feels that his decisions are supposed to keep everyone safe, even normal spending can feel morally loaded. A grocery run becomes a referendum on discipline. A family outing becomes a vote on whether the month can survive.

This pattern often starts with a private rule: if I think hard enough, I can prevent bad outcomes. That rule is comforting because it gives the illusion of control. But money is not fully controllable, so the father keeps tightening his grip and still feels unsafe. The more he monitors, the less calm he feels.

It also shows up in the stories fathers tell themselves. They may believe they are the only one who can catch mistakes, the only one who understands the real numbers, or the only one who should absorb the pressure. Those stories sound responsible, but they can become cages. Once that happens, every decision starts to carry the weight of the entire family future.

This is usually where people realize their money is not random; it is patterned. The same fear shows up in different clothes:

– delaying necessary spending but speeding through emotional purchases

– saying finances are fine while feeling tense every time money is mentioned

– overplanning small expenses while avoiding bigger conversations

– treating short-term comfort as a threat and long-term stress as normal

The deeper pattern is that worry becomes part of the decision process itself. Instead of asking what is wise, the mind asks what is safest, what will least disappoint others, and what will preserve dignity. That is not a budgeting problem alone. It is a psychological habit built around protection.

Common Mistakes People Make

One common mistake is assuming the behavior is just about being cheap or strict. That misses the emotional layer entirely. Fathers who quietly carry financial worry are usually not trying to control others. They are trying to keep their own fear from spilling into the room.

Another mistake is pretending the worry should disappear once the numbers look better. A higher income can reduce pressure, but it does not automatically retrain the brain. If someone has spent years bracing for instability, a better paycheck may not feel like relief. It may feel like a slightly larger surface for the same fear.

People also mistake constant caution for wisdom. There is a difference between being thoughtful and being trapped. Thoughtful spending comes from clarity. Trapped spending comes from anxiety. The difference is subtle, but it changes everything because one creates choice and the other creates narrowing.

A third mistake is making every money conversation about logic alone. A father can know the math and still feel panic when he sees the expense. He may need a budget, yes, but he may also need a way to stop interpreting every purchase as evidence of failure. Without that shift, even a good plan can feel emotionally impossible.

The final mistake is overlooking the cost of hidden stress. Quiet worry often does not appear in the spreadsheet, but it shapes sleep, patience, attention, and even the tone of family life. That means the financial issue is never only financial. It is behavioral, relational, and deeply personal.

Real-Life Patterns and Behaviors

You can often spot this pattern in the routine moments. A father checks the account before groceries, even though he already knows the general balance. He mentally rehearses the month before approving a school fee. He says, “We should wait,” even when waiting will not really solve the problem.

Sometimes the behavior looks like over-responsibility. He remembers every due date, every subscription, every repair, and every possible surprise. He may seem organized, but under the surface he is carrying a constant watchfulness that never fully turns off. The mind starts to treat ordinary life as a sequence of potential leaks.

Other times it shows up as emotional distance. He does not want to talk about money because talking about it makes the pressure feel more real. So he stays vague, handles things privately, and hopes the household keeps moving smoothly. That can protect others from immediate worry, but it can also isolate him inside his own stress.

There is also the pattern of sacrifice without visibility. A father may cut his own spending without mentioning it, delay repairs on his own car, or push personal needs aside so the family does not feel shorted. On the surface that looks noble. But if it becomes the default, it creates a life where his needs are always last and his anxiety always first.

What makes this so sticky is that the behavior often gets rewarded. People praise the father for being careful, steady, and selfless. That praise can reinforce a system where he never learns that safety can include flexibility. Over time, he may start believing that worry is proof of love, when it is really just a coping strategy that has overstayed its role.

What Actually Helps

What helps first is naming the pattern without shame. The goal is not to accuse fathers of being irrational. The goal is to recognize that repeated worry is often a learned response to responsibility, past pressure, or unstable seasons. When the pattern is named, it becomes something to work with instead of something to hide.

It also helps to separate decision-making from panic. Some fathers benefit from a simple rule: do not make money decisions in the middle of a stress spike. That pause creates space between fear and action. Even a basic budgeting tool or a spending tracker can help because it turns vague dread into visible information.

A calculator can be useful here too, not because it solves the emotional problem, but because it reduces the story-writing. When the numbers are clear, the mind is less likely to invent worst-case scenarios. That does not erase worry, but it can lower the noise enough to make a sane choice.

It is also helpful to look at the household role being played. Is the father acting like the sole financial guardrail? Is every decision resting on one person’s internal alarm system? If so, the problem is not just expense management. The problem is an overloaded role that leaves no room for shared clarity.

Finally, fathers often need permission to let some choices be ordinary. Not every purchase is a sign of irresponsibility. Not every unexpected expense is a crisis. The nervous system often needs repeated evidence that money can be handled without constant emergency mode. That evidence comes from small, steady experiences of making a plan and surviving the month.

What To Do Next

If this feels familiar, do not start by trying to fix everything at once. Start by noticing when the worry is strongest. Is it before bills, before family spending, before talking about money, or right after checking the account? That pattern matters more than a perfect plan in the first week.

Then look at one regular decision and map it honestly. A budgeting tool, a spending tracker, or a simple monthly calculator can show whether the fear matches the numbers or whether old anxiety is doing extra work. This is usually where people realize their money is not random; it is patterned, and patterns can be changed.

If you want a calm next step, choose one tool that makes the month visible instead of imagined. A basic budgeting calculator can be enough to turn worry into something measurable, which is often the first real relief. From there, the goal is not perfect control. The goal is fewer silent decisions made under pressure and more choices made with clarity.

Related Reading

- Financial Exhaustion: Why Many Men Feel It Now

- Why Men Over 40 Quietly Worry About Inflation

- Why Financial Stress Gets Harder After Decades of Work

Keep Exploring the Pattern

Watch more breakdowns of real-life money behavior on our YouTube channel.

Browse the full Money Behavior Library to explore more patterns like this one.

If you want a clearer view of your monthly patterns, try the Salary Breakdown Calculator, the Subscription Cost Calculator, or the Bill Due Date Planner.

Explore more patterns in the Money Behavior Library — a growing collection of real-life financial patterns explained clearly.

Disclaimer:

This content is for educational and informational purposes only and does not constitute financial advice. Always consult a qualified financial professional before making personal financial decisions.