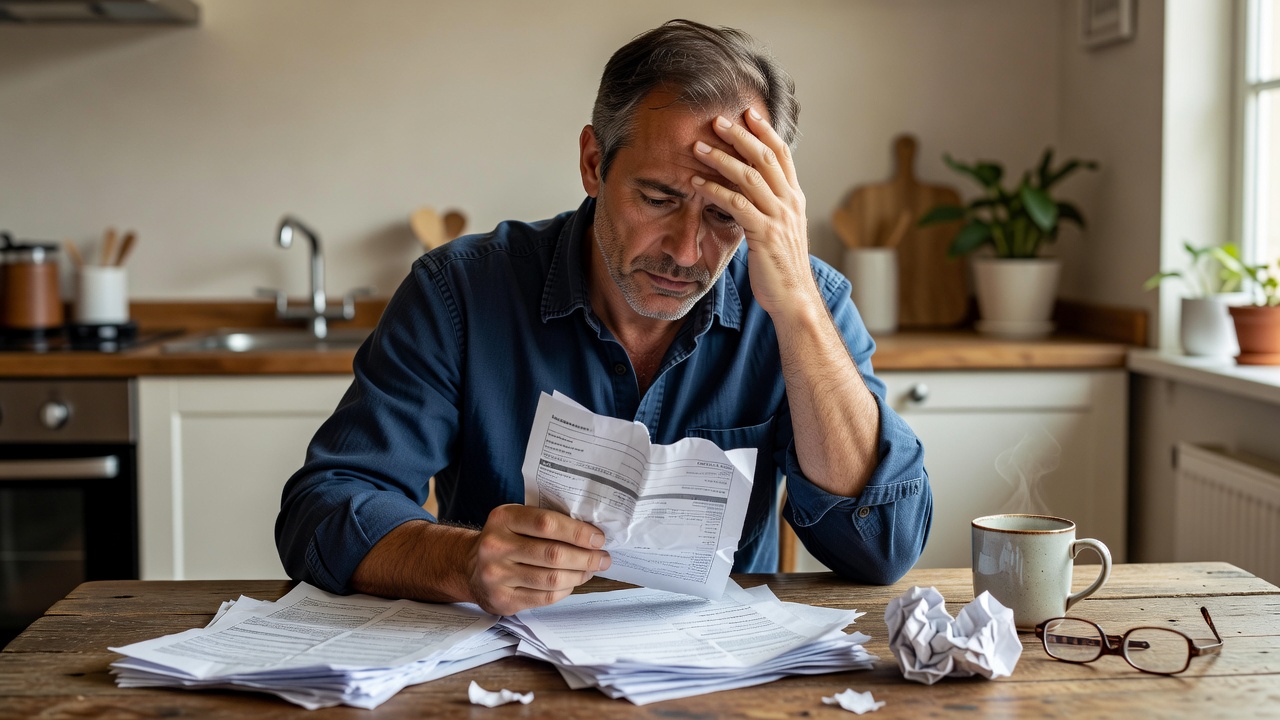

The bill arrives after the appointment, and the room gets quiet. He says it is fine, but the pause tells a different story. That is usually how panic about medical expenses shows up first: not as a breakdown, but as a small, private shutdown.

Why This Happens

Men often panic about medical expenses because the cost lands in a place that already feels loaded: responsibility. A doctor visit is never just a doctor visit when the bill can touch the mortgage, the credit card, the savings account, or the quiet promise to keep everything stable. For many men, the fear is not only about the amount. It is about what the amount might expose.

That is why the reaction can look so calm on the outside. A man may nod, say he will handle it, and then spend the evening mentally rearranging every expense in the house. He is not only calculating dollars. He is calculating what kind of person he will have to become if this cost is larger than expected. The panic is often private because private panic feels manageable.

Medical expenses also feel unpredictable in a way that everyday spending does not. You can delay a vacation, skip a restaurant, or postpone replacing a chair. But you cannot always delay a problem in your body. That lack of control creates a specific kind of money stress, and for many men, stress becomes silence before it becomes conversation.

This is where search intent often starts to show itself in real life. People are not really asking, “Why am I scared of a bill?” They are asking, “Why do I feel this knot in my stomach every time I see a medical charge?” That is a behavioral question, not a math question. And it explains why the same bill can feel manageable to one person and deeply threatening to another.

The Hidden Pattern Behind It

The hidden pattern is that medical expenses do not just threaten cash flow. They threaten identity. Many men were taught, directly or indirectly, that being steady means being prepared, and being prepared means not being caught off guard by money. So when a health expense arrives unexpectedly, it can feel like a personal failure even when it is not.

There is also a second layer: men often carry more financial silence than people realize. They may not say they are worried because they do not want to seem fragile, uninformed, or reactive. So the fear moves inward and becomes a private ledger of what-ifs. What if this is more expensive than they said? What if the deductible is higher than expected? What if this happens again next month?

That internal loop is why panic around medical bills is often disproportionate to the size of the bill itself. The number on paper is only one part of the response. The rest is built from memory, expectation, and the pressure to stay composed. In that sense, the bill is a trigger, but the deeper pattern is cumulative.

A useful way to think about it is this:

– The bill is the event.

– The fear of disruption is the pattern.

– The silence is the coping strategy.

This is usually where people realize their money is not random. It is patterned. The same person who can calmly compare insurance plans may still freeze when a specialist appointment creates a cost they never planned for. It is not inconsistency. It is a predictable response to uncertainty, responsibility, and social conditioning.

Common Mistakes People Make

One common mistake is treating the reaction as simple bad budgeting. Yes, budgeting matters, but a medical expense panic is rarely solved by a cleaner spreadsheet alone. When someone is already emotionally flooded, telling them to “just plan better” misses the part that is actually driving the behavior. The issue is not only preparedness. It is avoidance mixed with fear.

Another mistake is waiting until the bill arrives before thinking about the cost. By then, the emotional temperature has already risen. People often assume they will handle it when they see it, but the human brain tends to overreact when facts arrive late. That is why many men feel especially cornered by healthcare charges: the timing leaves no room to get comfortable.

A third mistake is confusing privacy with strength. Quietly absorbing the stress may feel disciplined, but it can also keep the problem larger than it needs to be. When no one talks about the likely cost, the mind fills the gap with worst-case scenarios. The result is not just a bill. It is a mental spiral.

People also tend to overestimate the emotional difference between a small bill and a large one. For some, a $200 expense can create the same internal shutdown as a $2,000 one if it arrives during a fragile month. The trigger is not always the size. It is the timing, the context, and the sense that the margin has disappeared.

Real-Life Patterns and Behaviors

The pattern often starts before the appointment. A man notices the pain, discomfort, or issue, but delays checking it because he does not want to invite the cost. He may tell himself he is being practical, but underneath that decision is a familiar money script: if I do not name it, maybe it stays small. That script works until it does not.

Then there is the bill itself. Some men open it immediately and then spend hours trying to make it disappear mentally. Others put it aside and avoid the envelope or email for days. Both behaviors are versions of the same response: delay the emotional impact by delaying contact with the number. The money is still there, but for a moment it feels less real.

A lot of the behavior follows a recognizable sequence:

– First comes hesitation to seek care.

– Then comes surprise at the expense.

– Then comes self-quieting: “I will figure it out.”

– Then comes private recalculation of every other category.

This is why medical expenses can affect more than the health budget. They can change how someone spends on groceries, family outings, gas, or home repairs for the next month. The bill is not isolated. It ripples through daily life, and that ripple can create resentment, anxiety, or a sudden feeling that everything is too tight.

Sometimes the panic is not even about being unable to pay today. It is about what happens if another expense follows. Medical bills can awaken a deeper fear of financial fragility, especially in households where one income, one deductible, or one setback already feels like a balancing act. The man is not only reacting to this bill. He is reacting to the possibility that this bill is a preview.

What Actually Helps

What helps first is naming the pattern without judging it. If the reaction is really about uncertainty, then the solution is not shame. It is visibility. When people can see the likely cost range before they are under pressure, the emotional reaction often softens. A simple cost estimate, insurance check, or treatment breakdown can lower the temperature more than a dozen well-meaning lectures.

This is where soft tools become genuinely useful. A budget calculator can turn vague fear into visible tradeoffs. A bill tracker can show whether the problem is one expense or a repeating pattern. A simple healthcare cost estimator can help someone stop imagining the worst and start working with numbers that feel concrete. These are not magic fixes, but they reduce the unknown.

It also helps to separate the fear of the bill from the fear of the story attached to the bill. Some men are reacting to the idea that they should have seen it coming. Others are reacting to the possibility that they will not be able to protect the people who depend on them. When those stories are named, they stop running the whole reaction from the background.

The most effective response is usually not dramatic. It is boring in the best possible way. It is a small reserve for medical costs, a habit of checking estimates early, and a quick review of how one healthcare bill affects the rest of the month. When the pattern is visible, the mind has less room to invent disaster.

If you want a practical lens, look for the moment when worry turns into avoidance. That is often the point where a person stops opening mail, delays calls, or keeps saying “later” even though the issue is already here. The sooner that moment is recognized, the less power it has.

What To Do Next

If this feels familiar, the next step is not to force confidence. It is to get clearer. Start by looking at one recent medical expense and asking what it actually did to your month, not just your account balance. Did it change what you spent elsewhere? Did it make you delay another decision? Did it create a quiet sense of pressure that never got named?

A basic expense tracker or budgeting tool can help you see that pattern without turning it into a project. If you prefer something simpler, use a calculator to estimate what a typical medical bill would mean inside your current budget. That one step can turn a vague fear into a concrete number, and concrete numbers are easier to face than imagined disasters.

Then notice the part you usually skip. Was the panic about the bill itself, or about what the bill said about your margin, your role, or your security? That distinction matters because it tells you whether the real issue is cost, timing, or the story you carry about money. Once you know that, you can respond to the right problem.

If you want to go one step further, consider making medical expenses a separate category before you need it. Not as a grand plan, just as a small place for reality to land. A little structure now can prevent a lot of private panic later. And if you are not sure where to start, a simple calculator or tracking tool is often enough to show you the shape of the problem before it grows.

Related Reading

- Why Men Over 45 Panic About Unexpected Expenses

- Why Men Quietly Carry Financial Stress Into Relationships

- Why Financial Pressure Quietly Changes Men’s Personality

Keep Exploring the Pattern

Watch more breakdowns of real-life money behavior on our YouTube channel.

Browse the full Money Behavior Library to explore more patterns like this one.

If you want a clearer view of your monthly patterns, try the Salary Breakdown Calculator, the Subscription Cost Calculator, or the Bill Due Date Planner.

Explore more patterns in the Money Behavior Library — a growing collection of real-life financial patterns explained clearly.

Disclaimer:

This content is for educational and informational purposes only and does not constitute financial advice. Always consult a qualified financial professional before making personal financial decisions.