At the grocery store, the total at checkout feels higher than it should, and the number hangs in the air longer than it used to. For many men over 40, that quiet pause is where inflation stops being a headline and starts feeling personal.

Why This Happens

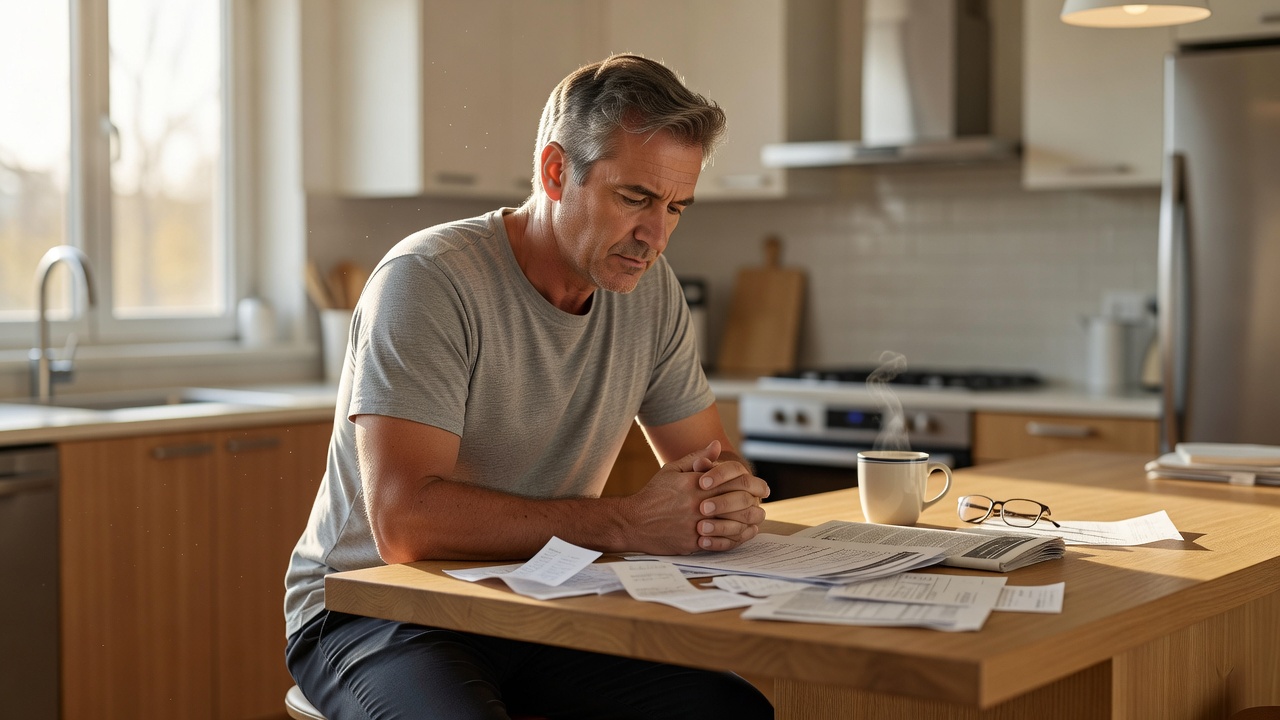

Men over 40 often worry about inflation in a way that never sounds dramatic out loud. It shows up as a quiet recalculation in the background of daily life, where familiar expenses suddenly feel less stable than they used to. The concern is not only about prices rising. It is about the feeling that the ground under long-planned routines is moving.

By this age, many people have built a life around a fairly specific set of assumptions. The mortgage, the school bills, the car payment, the grocery run, the weekend tank of gas, the medical copays, the holiday spending all become part of a known system. Inflation interrupts that system. It creates a gap between what used to work and what works now, and that gap is where worry grows.

For a lot of men, the worry is also tied to identity. They may not think of themselves as anxious people, but they do think of themselves as responsible, prepared, and capable of handling pressure. Inflation threatens that self-image because it introduces a problem that is larger than effort. You can work hard, stay disciplined, and still feel like you are losing ground.

That is why the fear often stays private. It does not always come out as panic. More often it becomes a sharper attention to receipts, a longer look at bank balances, or a strange irritation when ordinary purchases cost more than expected. It is not just about money. It is about control, competence, and the uncomfortable sense that life is becoming harder to manage without warning.

The Hidden Pattern Behind It

The pattern behind this worry is usually not the inflation itself. It is the comparison between present reality and an internal baseline that was built years ago. Many men over 40 carry a mental model of what life should cost, what a normal month should look like, and how far their income should go. When prices shift, that model starts to fail, and failure feels personal even when it is simply mathematical.

This is why inflation can feel bigger at 45 than it did at 25. In your twenties, rising prices are annoying. In your forties, they can feel like a direct threat to the structure of your life. There is more at stake now: family stability, retirement savings, aging parents, home maintenance, insurance, and the pressure to keep everything running without visible strain.

There is also a psychological trap here. People do not react to inflation in a vacuum. They react to inflation through memory. If rent, groceries, gas, and insurance used to fit comfortably inside a month, the new numbers can feel insulting or unreal. The brain keeps asking, why is this suddenly harder, even if the answer is simple and obvious.

This is usually where people realize their money is not random. It is patterned. The same emotional response appears every time a bill comes in higher than expected:

– surprise turns into tension

– tension turns into overthinking

– overthinking turns into avoidance or control

– control shows up as checking, cutting, or second-guessing

Once that loop starts, inflation is no longer just an economic issue. It becomes a recurring emotional event.

Common Mistakes People Make

One common mistake is treating inflation like a temporary inconvenience instead of a structural change in how money behaves. When people assume prices will drift back down soon, they often delay adjustments that would reduce stress. They keep living inside the old budget, then feel confused when the old budget keeps failing.

Another mistake is focusing only on big expenses and ignoring the small, repeated ones. A man might notice the mortgage or the insurance premium, but not the extra thirty dollars a week at the grocery store, the higher lunch tabs, or the slight increase in household supplies. Inflation usually works through repetition, not shock. The small changes add up quietly until the month feels tighter for reasons that are hard to name.

Some people respond by tightening everything at once. They cut spending aggressively, stop enjoying normal routines, and start treating every purchase like a test. That can create a different problem: the budget becomes emotionally unsustainable. A plan that feels like punishment does not last, even if it looks disciplined on paper.

Another mistake is measuring financial health only by income. A higher paycheck does not automatically protect someone from inflation if every expense category rises at the same time. That is one reason people can earn more and still feel behind. The pressure is not always about income level. It is about how quickly income is absorbed by the cost of maintaining a life.

The final mistake is silently assuming this fear means weakness. It does not. Worry is often a signal that someone understands the stakes clearly. The problem is not the presence of worry. The problem is when worry becomes vague and unexamined, because then it starts shaping choices without ever being discussed.

Real-Life Patterns and Behaviors

If you watch closely, inflation anxiety follows a few repeatable patterns in everyday life. A man may begin to notice prices in places he never used to check. He compares groceries from week to week, mentally tracks fuel costs, or starts feeling irritation before opening a bill. The behavior looks small, but it reveals a deeper shift: money is no longer background noise.

Another pattern is the private recalibration. Someone might not say, I am worried about inflation, but he will quietly stop ordering the usual thing, skip a routine purchase, or delay replacing something that used to be replaced without debate. These choices can be sensible, but they are also emotional clues. They show where a person no longer feels safe spending as freely as before.

This is especially common in middle age because the financial picture is layered. The same person may be paying for teenagers, saving for retirement, supporting a partner, and preparing for health-related surprises. Inflation touches all of those at once. What looks like a price increase in one category can feel like a threat to the whole system.

A common behavior is over-monitoring. People check their accounts more often, compare statements, and look for spending leaks that feel easier to control than the bigger economic picture. That can be useful, but it can also become a form of stress management disguised as budgeting. The act of checking brings a brief sense of control, even when the underlying fear stays the same.

Another behavior is emotional compression. Men who are used to carrying responsibility often do not describe money stress in emotional terms. They may call it being careful, staying sharp, or being realistic. But underneath that language is often a quieter story: I do not like how vulnerable this makes me feel. That feeling matters because it shapes whether they respond with clarity or with silent strain.

What Actually Helps

What helps is not pretending inflation is small. It is making the pattern visible. When people see which categories are rising, when the pressure tends to hit, and what emotional response follows, the problem becomes easier to manage. The point is not to eliminate concern. The point is to stop letting concern stay vague.

A practical budget tracker can help here because it turns frustration into data. A simple spending tool, a calculator for monthly cash flow, or even a category-based budget sheet can show whether the issue is groceries, gas, subscriptions, insurance, or a combination. That matters because the brain handles named problems better than foggy ones. Once the pattern is visible, the decisions get calmer.

It also helps to separate inflation from self-judgment. Rising prices do not mean you failed to plan well enough. They mean your old plan was built for different conditions. That distinction sounds small, but it changes the emotional tone of everything that follows. Without it, people often react to economic pressure as if it were proof of personal inadequacy.

Another useful move is to compare actual spending against expectation, not against fantasy. Many money worries grow because the mind remembers a lower number and treats it like a permanent baseline. A realistic comparison can show whether the pressure is temporary, widespread, or concentrated in just a few categories. This is where a budgeting tool or a simple calculator can be more calming than another hour of guessing.

People also benefit from noticing the timing of their stress. Does the worry spike at the grocery store, after bill day, when fuel prices rise, or when the annual insurance renewal arrives? The answer usually reveals a trigger point. Once you know the trigger, you are no longer reacting to a whole invisible force. You are responding to a specific pressure point in the month.

What To Do Next

If this sounds familiar, start by naming the pattern instead of debating it. Ask a simple question: where does inflation actually hit my life, and what behavior does it trigger in me? That question is more useful than a vague sense that everything is getting worse.

Then look at one ordinary month, not your worst month. Use a calculator or a spending tracker to compare what you expected to spend with what you actually spent. You are not trying to become obsessive. You are trying to see whether the stress comes from one category, several categories, or from the feeling of losing predictability itself.

From there, choose one small adjustment that restores clarity. It might be a weekly check-in, a better budget tool, or a side-by-side look at recurring expenses. The goal is not perfection. The goal is a calmer relationship with the numbers so they stop ambushing you in daily life.

And if you want the process to feel less abstract, use a simple inflation or budget calculator before making your next money decision. A tool will not remove the pressure, but it can make the pressure visible enough to work with. That is often the moment people realize they do not need a bigger reaction. They need a clearer map.

Related Reading

Keep Exploring the Pattern

Watch more breakdowns of real-life money behavior on our YouTube channel.

Browse the full Money Behavior Library to explore more patterns like this one.

If you want a clearer view of your monthly patterns, try the Salary Breakdown Calculator, the Subscription Cost Calculator, or the Bill Due Date Planner.

Explore more patterns in the Money Behavior Library — a growing collection of real-life financial patterns explained clearly.

Disclaimer:

This content is for educational and informational purposes only and does not constitute financial advice. Always consult a qualified financial professional before making personal financial decisions.