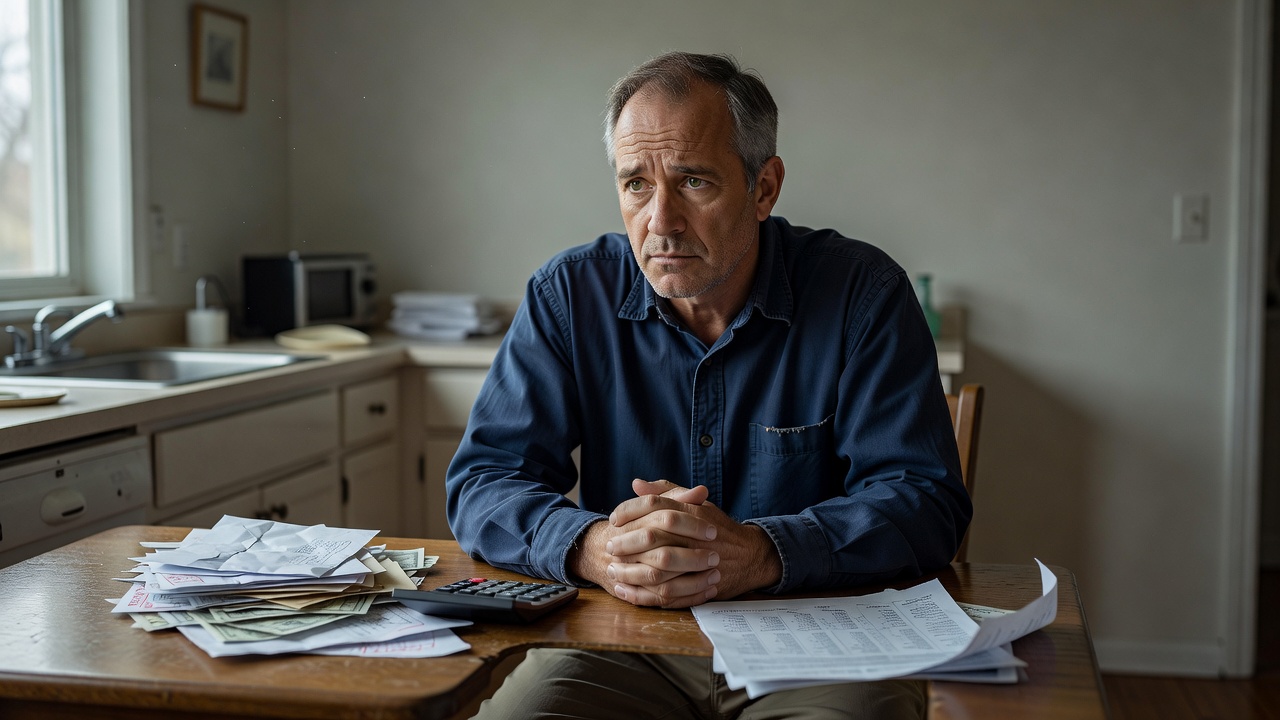

It usually shows up on an ordinary night: the bills are open, the account balance is smaller than expected, and the math feels heavier than it should. For a lot of men over 40, that quiet sense of being financially defeated is not about one bad month — it is about a pattern that has been building in the background for years.

Why This Happens

By the time many men reach their 40s, money stops feeling like a simple problem with a simple answer. The early adult story often promised that working hard would eventually make life feel stable, but real life tends to add mortgages, children, aging parents, health costs, layoffs, and the strange pressure of trying to look unbothered while carrying all of it. That is where the emotional shift begins: money is no longer just money, it becomes a scorecard for effort, status, and control.

The feeling of defeat usually does not arrive in a dramatic moment. It arrives in small, repeatable scenes. A man checks his account after payday and notices there is less left than there used to be. He says yes to a dinner, a repair, or a family expense without really thinking, then feels a private sting later when he sees the balance. Over time, those moments create a quiet internal sentence: I should be doing better than this.

That sentence matters because it is often less about mathematics than identity. Many men were taught to equate being competent with being financially steady, yet modern life has made financial steadiness harder to maintain and easier to fake. You can have a decent income and still feel behind if your lifestyle grew faster than your system, or if your responsibilities multiplied faster than your confidence.

This is usually where people realize their money is not random, it is patterned. The sense of defeat often comes from repeating the same cycle: earn, absorb pressure, spend to relieve pressure, then feel temporary shame when the numbers no longer support the image. The money is not disappearing by accident. It is being used to manage emotional strain in real time.

For men over 40, that strain can be especially quiet because many do not announce it. They may not call themselves anxious, but they feel tense when opening a statement. They may not say they are overwhelmed, but they avoid looking at retirement numbers or credit card totals. The silence becomes part of the problem, because what is not looked at does not get named, and what is not named keeps repeating.

The Hidden Pattern Behind It

The hidden pattern is usually not a lack of discipline. It is a mismatch between the life a man is living and the financial system he is using to support it. A lot of people still think the issue is one big bad habit, but in most cases it is a chain of smaller behaviors that reinforce each other until they feel normal.

A common version looks like this:

– Pressure builds at work or home.

– Spending becomes a quick way to soften that pressure.

– The relief feels immediate, which makes the habit easier to repeat.

– The account balance drops, creating guilt or avoidance.

– Avoidance delays the next correction, which makes the gap bigger.

That is why financial defeat feels so personal. The problem is not only the balance sheet. It is the emotional loop underneath it. A man may tell himself he is simply being practical, but sometimes he is really trying to protect himself from disappointment, conflict, or the feeling of not measuring up.

There is also the hidden belief that adulthood should have produced a clean financial picture by now. Many men over 40 carry an old mental timeline: by this age, I should own more, owe less, save more, and feel calmer. When reality does not match that timeline, the gap creates shame. Shame is powerful because it rarely encourages action. More often, it encourages hiding, minimizing, or waiting for a better month that never quite arrives.

Another part of the pattern is comparison. Men in this age range often compare their private reality to someone else’s public confidence. A colleague with a new truck, a friend talking casually about investing, a sibling who seems to have everything under control, a social feed full of curated stability — all of it can make a normal life feel like failure. The comparison is unfair, but the feeling is real.

What makes the pattern hard to see is that it often wears respectable clothing. The man is working. The bills are mostly paid. The family is covered. Nothing looks catastrophic from the outside. But inside, he is negotiating with a quiet sense of lateness, as if everyone else got a financial manual he somehow missed. That is where defeat settles in: not because the person has nothing, but because he believes he should have been further along.

Common Mistakes People Make

One of the biggest mistakes is treating the feeling as proof of incompetence. When men feel financially defeated, they often turn the experience into a character judgment. They say things like I am bad with money or I never figured this out, when the real issue is usually a long-running behavior pattern that has never been made visible.

Another mistake is trying to fix emotional pressure with one-off spending rules. A man might decide to stop buying takeout, cancel subscriptions, or promise to be stricter after a bad month. Those changes may help a little, but they do not address the reason spending became soothing in the first place. If the underlying trigger is stress, resentment, exhaustion, or a need to feel in control, the pattern usually returns in another form.

A third mistake is waiting for motivation to appear before looking closely at the numbers. This is a subtle but common avoidance habit. People assume they need to feel ready before they open the statements, review the debt, or build a budget. In reality, clarity usually creates readiness, not the other way around. The longer the numbers stay vague, the more intimidating they become.

There is also a mistake that is easy to miss: keeping financial pain private for too long. Many men do not want to worry anyone, look weak, or admit that the situation feels worse internally than it does externally. So they carry it alone. The problem is that isolation gives the pattern more room to grow, because no outside structure interrupts it.

Finally, some men confuse stability with distance from the problem. They may have a steady job and a life that looks functional, so they assume they are fine. But if every extra dollar disappears without intention, if every surprise expense causes panic, or if retirement planning feels like a language they never learned, then the real issue is not income alone. It is financial structure.

Real-Life Patterns and Behaviors

The most revealing money patterns are often ordinary enough to overlook. A man may keep a mental account of what he has already earned and spend as if the next paycheck will smooth everything out. That can work for a while, until one unexpected repair, one family obligation, or one month of higher costs knocks the system sideways.

He may also spend more when he feels less in control. The purchase is not always about the item. Sometimes it is about restoring a sense of agency. A tool, a meal, a gadget, a quick upgrade, or even a solo escape can briefly make life feel more manageable. The purchase says, at least for a moment, I can still decide something.

For some men, the pattern shows up in how they talk about money. They may speak in broad terms and avoid specifics. They know they are doing okay, or not okay, or better than before, but they cannot say exactly how much they save, how much they owe, or where the leaks are. Vague language keeps the emotional heat lower, but it also keeps the problem unresolved.

The behavioral loop often looks like this in daily life:

– He tells himself the issue will settle down after this month.

– He avoids one uncomfortable money task.

– He uses spending, busyness, or distraction to get through the week.

– The account stays uncertain, and the unease returns.

This is where the psychological weight becomes visible. A man may be functioning, but he does not feel oriented. He can show up, work hard, and carry responsibility while quietly sensing that the ground beneath him is not as solid as it should be. That feeling can be exhausting because it is not a crisis anyone else can easily see.

There is also a deeply human pattern around pride. Men over 40 often want to solve problems privately and efficiently. They do not want to ask for help unless the situation is extreme. But money problems rarely become easier through silence. They become easier through pattern recognition. A simple budgeting tool, a spending tracker, or even a basic calculator for debt payoff can reveal what the mind has been too stressed to hold clearly.

The important part is not the tool itself. It is the mirror it provides. Once the numbers are visible, the story changes from I am failing to I can see what keeps happening. That shift matters because it turns shame into observation. And observation is where change starts.

What Actually Helps

What actually helps is not a heroic reset. It is creating enough clarity that the same emotional trigger no longer produces the same invisible outcome. When men over 40 feel financially defeated, they usually do not need a lecture about discipline. They need a system that separates the feeling of pressure from the habit of reacting to it.

That means looking at the pattern in plain language. If spending rises when work feels unstable, name that. If money avoidance begins after family tension, name that too. If the urge to spend shows up after a week of being the one everyone depends on, that is not random behavior. It is a coping response. Once it is identified, it becomes easier to interrupt.

It also helps to stop expecting a perfect budget to solve an emotional problem. A budget is useful, but only if it reflects actual behavior. If the plan is built around who you wish you were instead of who you are on a normal Tuesday, it will quietly fail. A better approach is to build around reality: fixed costs, recurring pressures, likely temptations, and the expenses that always seem small until they are not.

A spending tracker can be surprisingly useful here because it removes memory from the equation. Many people think they need more self-control when they actually need more visibility. The mind tends to remember the big purchases and forget the repeated small ones. Over a month, those small decisions can tell a much more honest story than pride ever will.

This is also where the right calculator can help without making the process emotional. A debt payoff calculator, savings goal calculator, or retirement estimate tool gives shape to uncertainty. The goal is not to obsess over numbers. The goal is to reduce the mental fog that makes everything feel larger and more hopeless than it is.

Most importantly, help tends to work when it is specific. Not I need to be better with money, but I need to know what happens every time I feel behind and spend to compensate. Not I should save more, but I need one visible place where the extra money goes before it disappears. That kind of clarity is calmer than motivation, and usually more durable too.

What To Do Next

If this feeling sounds familiar, the next step is not to shame yourself into a clean slate. It is to observe the pattern while it is still small enough to understand. Start with one week of honest tracking, not to judge yourself, but to see what pressure triggers what behavior.

Then use one simple tool instead of carrying the numbers in your head. A basic budgeting tool, a debt calculator, or a spending tracker can show whether the problem is income, timing, emotional spending, or a combination of all three. That clarity is often more helpful than another vague promise to do better next month.

If you want a calmer way forward, look at the numbers the way you would look at weather: not as a verdict, but as information. The right next move is usually small, visible, and repeatable. Once you see the pattern, the defeat is no longer mysterious, and what felt personal starts to look manageable.

Related Reading

- Why Men Over 40 Quietly Worry About Inflation

- Why Men Quietly Feel Financially Replaceable at Work

- Why Men Over 50 Feel Financially Uncertain About the Future

Keep Exploring the Pattern

Watch more breakdowns of real-life money behavior on our YouTube channel.

Browse the full Money Behavior Library to explore more patterns like this one.

If you want a clearer view of your monthly patterns, try the Salary Breakdown Calculator, the Subscription Cost Calculator, or the Bill Due Date Planner.

Explore more patterns in the Money Behavior Library — a growing collection of real-life financial patterns explained clearly.

Disclaimer:

This content is for educational and informational purposes only and does not constitute financial advice. Always consult a qualified financial professional before making personal financial decisions.