You’re standing in the kitchen after a long workday, looking at a bill that should not feel this heavy. It is strange how money can feel more stressful now, after years of earning, than it did when you had less.

That feeling is real, and it usually means something in the pattern has changed. Not necessarily your discipline, but the life around the money.

Why This Happens

Financial stress often feels harder after decades of working because the stakes have changed, even if the paycheck has not changed in a dramatic way. In your 20s or 30s, money stress can feel temporary, like a rough season you expect to outrun. By middle age, it starts to feel personal, cumulative, and harder to ignore.

At this stage, you are not just paying bills. You are carrying years of obligations, maintenance, family needs, health costs, and the quiet fear that the next surprise will arrive when you are least ready for it. The nervous system notices that pattern long before the spreadsheet does. This is why a modest expense can feel disproportionately heavy.

There is also a psychological shift that happens over time. When you have worked for decades, you expect your effort to have created more stability than it sometimes actually has. If the gap between effort and ease remains wide, the frustration becomes part of the stress itself.

That is why this kind of money pressure can feel so discouraging. It is not only about the numbers. It is about the feeling that you have been responsible for a long time and still do not feel safe.

Many people search for answers like why am I more stressed about money now, or why does financial stress get worse with age. The answer is often less about income alone and more about accumulated mental load, rising fixed costs, and the emotional cost of carrying uncertainty for too long.

The Hidden Pattern Behind It

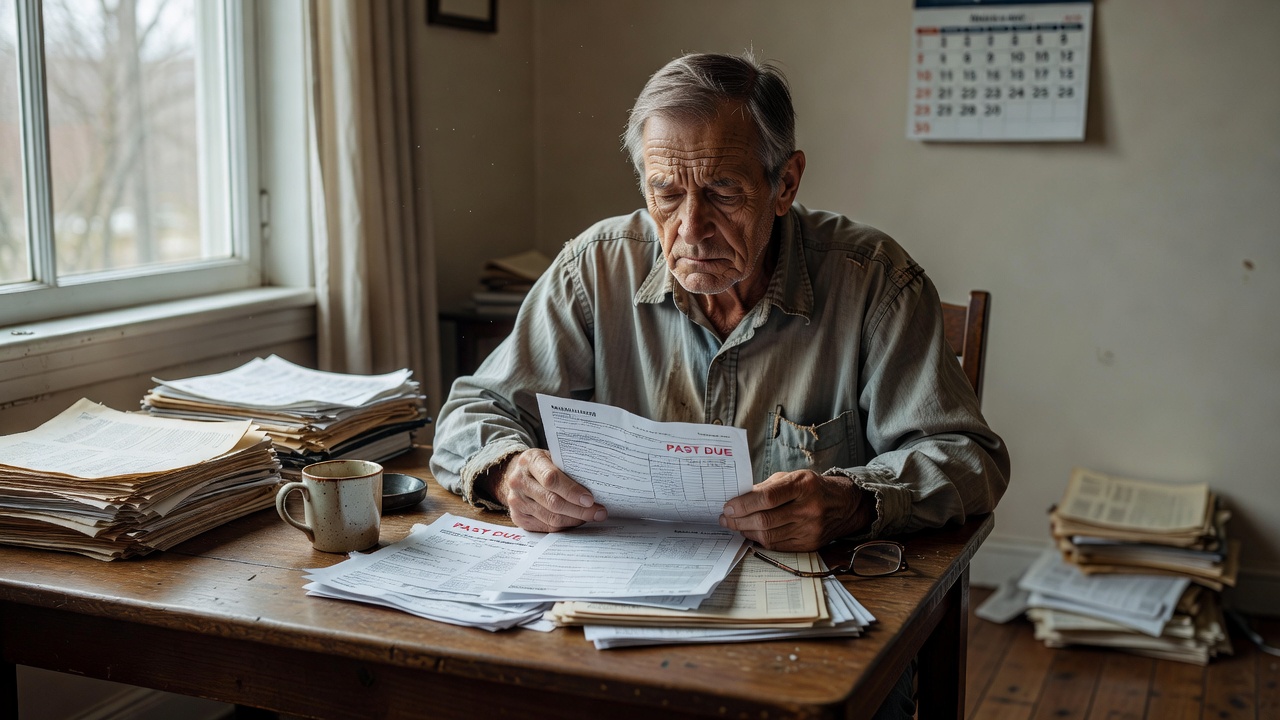

The hidden pattern is that financial stress rarely comes from one large event. It usually comes from repeated friction. Small overdrafts, higher insurance premiums, medical bills, family requests, delayed repairs, and retirement worries all stack together until the mind starts treating money as a constant alert.

Once that alert state becomes normal, everything feels urgent. A car repair is not just a car repair. It becomes proof that the buffer is too thin. A grocery bill is not just a grocery bill. It becomes a reminder that life keeps getting more expensive while your energy for managing it keeps shrinking.

This is where people begin to feel stuck in a loop. They are working, spending, and trying to keep up, but the emotional experience is still one of scarcity. That mismatch matters. People do not only react to their bank balance; they react to what that balance seems to predict.

A common pattern looks like this:

– You delay checking accounts because you do not want another stress spike.

– The delay creates more uncertainty, which makes the next check even harder.

– The bill arrives late, which increases fees or panic.

– The experience confirms the belief that money is always going wrong.

This is usually where people realize their money isn’t random… it’s patterned. The pattern is not laziness. It is avoidance, overload, and a system that has grown too emotionally charged to manage casually.

Common Mistakes People Make

One common mistake is treating the problem as if it were only a math problem. People think if they just made a stricter budget, they would feel better. But when the real issue is chronic tension, fear, or exhaustion, a tighter budget can actually feel like another demand.

Another mistake is assuming the stress means they have failed. That interpretation is emotionally powerful and usually unfair. A person can have worked hard for 30 years, made responsible decisions, and still end up with a fragile financial life because of inflation, caregiving, debt, timing, or underwhelming wage growth.

People also often make the mistake of waiting for motivation before looking at the numbers. In reality, the numbers usually become less frightening after they are seen clearly, not before. Avoidance gives the problem a larger shadow than the problem itself.

A few recurring mistakes tend to show up in this stage of life:

– Confusing financial anxiety with personal failure.

– Trying to fix stress with one dramatic move instead of pattern-based changes.

– Ignoring small leaks because they seem too minor to matter.

– Comparing current stability to an idealized version of earlier life.

When someone keeps saying, I do not know where the money goes, the deeper issue is often not ignorance. It is that the household has been operating on emotional autopilot for years.

Real-Life Patterns and Behaviors

The daily life version of this problem is often very ordinary. You may be earning more than you did years ago, but your expenses are also more complicated, less flexible, and harder to escape. The result is a sense that your money disappears before you can even think about it.

This is especially true for people balancing work with caregiving, aging parents, children still at home, or their own health concerns. The older you get, the less your finances are just about you. Money becomes connected to other people’s needs, and that makes every decision feel heavier.

There is also a behavioral pattern where the stress becomes visible in how you move through the day. You put off logging into your accounts. You avoid opening certain emails. You spend mentally, even when you do not spend physically, because you are rehearsing worst-case scenarios.

Over time, the body learns the rhythm of the stress. Sunday night feels tense. Paydays feel brief. Unexpected mail triggers dread. Even when things are technically manageable, the emotional system keeps acting as if it is bracing for impact.

That is why financial stress after decades of work can feel so different from earlier money stress. It is not just about having less freedom. It is about having less recovery time. A younger person may recover from a bad month faster because they have more flexibility, fewer commitments, and more time to rebuild. A midlife adult often feels every setback immediately.

The behavior then reinforces the feeling. If you are constantly reacting, you never get the calm needed to think clearly. If you never think clearly, you keep making reactive choices. That loop is exhausting, and it is one of the biggest reasons financial stress feels heavier with age.

What Actually Helps

What helps most is not a heroic overhaul. It is reducing the emotional charge around the money so you can see the pattern without flinching. That usually begins with clarity, not control.

A simple tracking tool can help here, especially one that shows categories over time. Not because the tool is magical, but because it gives your mind something concrete to look at. Many people feel calmer once they can distinguish between real overspending, fixed costs, and irregular expenses that only seem random.

Budgeting tools also help when they are used as mirrors, not punishments. The goal is not to shame yourself into discipline. The goal is to make the invisible visible. Once you can see the pattern, you can start asking better questions: Which costs are fixed? Which are emotional? Which ones spike during stress?

This is also where a calculator can be surprisingly useful. A debt payoff calculator, retirement estimate, or savings goal calculator can turn vague dread into a timeline. Not a perfect timeline, just a clearer one. Clarity often lowers anxiety more effectively than optimism does.

The most useful changes tend to be boring, specific, and repeatable:

– Identify the top three recurring stress triggers.

– Separate true emergencies from predictable irregular expenses.

– Review spending when you are calm, not after a scare.

– Use one tool consistently instead of trying five systems at once.

What actually helps is a system that reduces decision fatigue. When money stress has been building for years, the issue is often not that you need more willpower. It is that your current system asks too much of you at the exact moments you have the least energy.

What To Do Next

Start with one honest look at the pattern, not the whole future. Open the account, review the last few months, and notice where the stress starts before the spending does. That is usually the real entry point.

If you want a calm next step, use a simple budgeting tool or calculator to map one category at a time. Look at bills, debt, and irregular expenses separately, because lumping everything together makes the whole picture feel worse than it is. The goal is not to solve your entire life tonight.

The next move is to make the problem smaller and more visible. That alone can change how financial stress feels, because the mind does better with named patterns than with vague dread. Once the pattern is named, it becomes easier to interrupt.

If you want, start with a spending tracker, a debt calculator, or a monthly budget review and treat it like a checkup, not a judgment. That is often the difference between feeling overwhelmed and feeling oriented. And when you are ready, build from that single clear look instead of trying to fix everything at once.

Related Reading

- Why Men Quietly Fear Running Out of Money Eventually

- Why Men Quietly Feel Financially Replaceable at Work

- Why Men Over 50 Feel Financially Uncertain About the Future

Keep Exploring the Pattern

Watch more breakdowns of real-life money behavior on our YouTube channel.

Browse the full Money Behavior Library to explore more patterns like this one.

If you want a clearer view of your monthly patterns, try the Salary Breakdown Calculator, the Subscription Cost Calculator, or the Bill Due Date Planner.

Explore more patterns in the Money Behavior Library — a growing collection of real-life financial patterns explained clearly.

Disclaimer:

This content is for educational and informational purposes only and does not constitute financial advice. Always consult a qualified financial professional before making personal financial decisions.