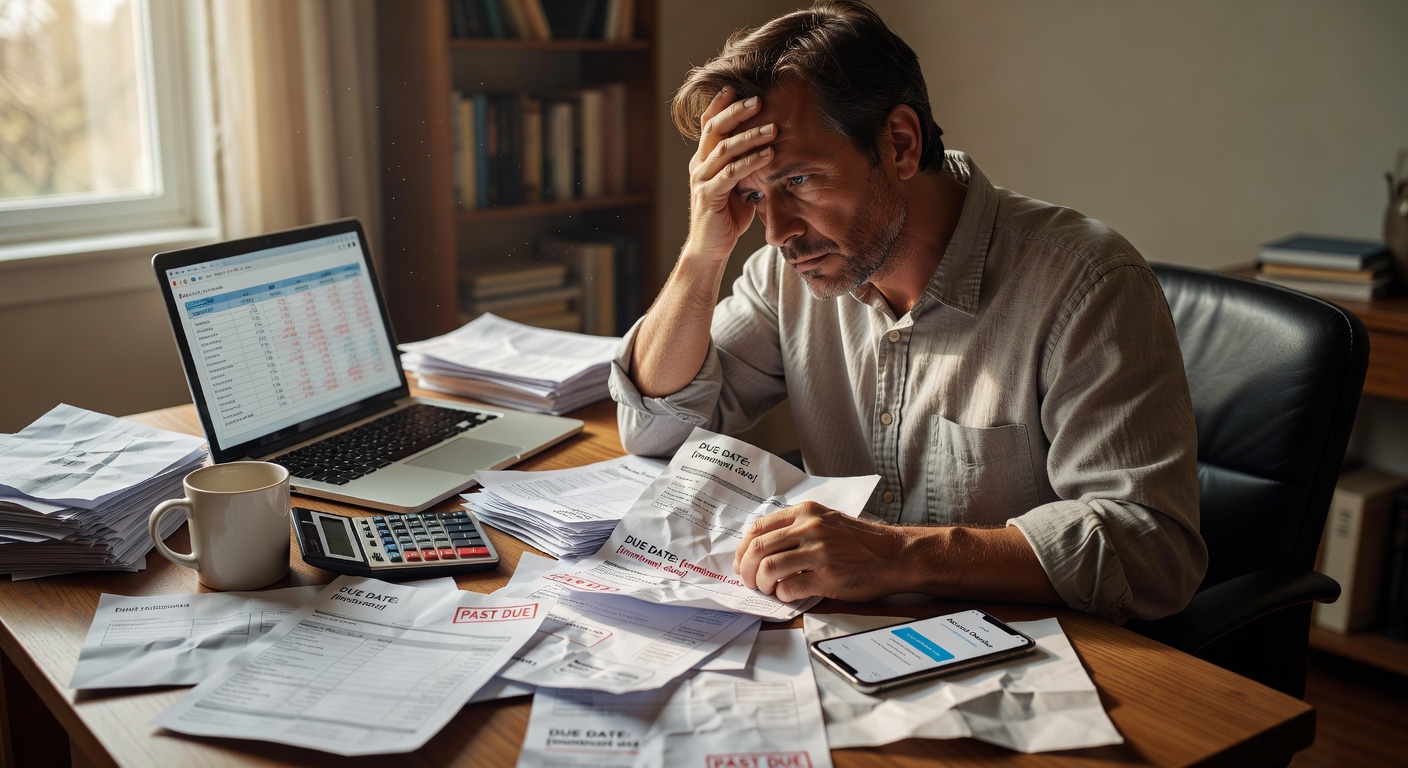

The reminder sits in the inbox, the bank balance is visible, and the bill still waits until later in the evening. Bill payments can start to feel simple enough, right up until decision fatigue takes over near the due date and every choice suddenly feels heavier than it should. That is usually where the sequence starts to slip.

Why This Happens

Decision fatigue does not usually arrive like a clear event. It builds in the background through a day of small choices, work interruptions, family logistics, grocery decisions, and the ordinary mental load that follows middle age. By the time bill payments come into view near the due date, the brain is often less willing to compare accounts, check balances, or decide which transfer should happen first. The task is still simple on paper, but the mind treats it like one more thing to sort out.

That is where bill management gets quietly complicated. A person may intend to pay everything on time, yet the process now requires a series of judgment calls: which bill matters most, which card should be used, whether to wait until payday, whether to move money from savings, and whether a late fee is actually worth avoiding. Research on decision fatigue shows that repeated decision-making can reduce deliberation and increase avoidance or deferral, which fits the feeling many people recognize near month-end. The tension is not that the bill is confusing; it is that the mind is less available than it was earlier in the day.

Financial stress can make the effect stronger, even when the person is generally organized. When money feels tight, the brain starts scanning for possible mistakes instead of clean answers, and that can slow even routine actions like confirming a due date or scheduling a payment. The result is not always panic; sometimes it is a kind of quiet delay, where the bill stays open in a tab while other tasks keep winning attention. It does not feel like a decision at the time.

The closer the due date gets, the more the situation can feel like a series of trade-offs instead of a simple monthly habit. A utility bill, a credit card payment, and a subscription renewal may all be technically manageable, but they do not all feel equally urgent in the moment. Decision fatigue often pushes people toward the option that requires the least mental effort, not the one that best supports the monthly budget. That is why the plan made earlier in the month can still fall apart near the end.

This is also why routine matters so much in bill payments. A recurring system reduces the number of choices that have to be made when mental energy is already thin. Sources on timely payment habits recommend automating as many decisions as possible and setting specific days or times for bill payment, because fewer choices mean less room for fatigue to interfere. The body may be present at the desk, but the mind has already spent some of its capacity elsewhere.

Common Mistakes People Make

The first pattern is waiting until everything feels fully clear before paying anything. That sounds careful, but near a due date it often turns into a pause while the person checks one more account, reopens one more app, or tries to find the perfect order for every payment. The bill does not need perfection to be handled, but decision fatigue makes perfection feel safer than action. This is the part that tends to go unnoticed.

A second pattern is treating every bill as a fresh decision instead of a recurring one. Each payment then carries the weight of a mini negotiation: should this come from checking, savings, or a credit card; should the minimum go out now; should the bigger transfer wait until payday? The more often those choices are made from scratch, the more draining bill management becomes. A monthly budget looks orderly from the outside, while the person inside the process is still deciding the same things over and over.

The third pattern is saving the most mentally demanding bills for the end of the day. That often means opening the banking app after dinner, checking balances while tired, or trying to remember which subscription renews first while scrolling through messages. The timing creates its own friction, because late evening is when many people have already spent their attention on work, family, and small convenience purchases that filled the gaps in the day. The bill itself may be simple, but the timing makes it feel larger than it is.

What follows is often less about the bill and more about the mental residue around it. Once a person has delayed one payment, the remaining bills start to feel heavier too, because every unresolved item adds one more layer of unfinished thinking. That can lead to a quick late-night transfer, a rushed debit card payment, or a temporary choice that keeps the account balance from dropping too low. The behavior makes sense in the moment, even when it leaves the overall system less stable.

These habits are rarely signs of carelessness. They are usually signs that the person has been making too many decisions for too long without a clean point of closure. Decision fatigue debt, as some behavioral writers describe it, is useful language for this feeling because the exhaustion does not disappear just because the task is ordinary. The bill still arrives, but the energy to deal with it arrives unevenly.

It also helps explain why the same person can be careful with money in one part of the month and scattered in another. A strong start to the paycheck cycle can create the impression that the whole month will hold together on its own, but the last stretch often exposes how much effort it takes to stay consistent. The tension is between the plan and the state of mind doing the planning. That gap is where late fees, missed transfers, and unhelpful timing usually begin.

Real-Life Patterns and Behaviors

A common scene is the mid-month balance check that happens between errands. The number looks acceptable, but there are still two utility bills, a credit card payment, and a grocery trip to account for before payday. Decision fatigue starts to shape the next move, and instead of paying the bill right then, the person decides to wait until the evening when there will be more time. That is usually when the evening disappears into other tasks.

Grocery trips are another place where the pattern shows itself. A person may head into the store planning to stay under budget, then notice a few convenience items, a household refill, and one small thing that seems easier to grab now than replace later. The spending itself is not the whole issue; the point is that the brain has already been asked to make a dozen tiny decisions before the bill payment even comes back into view. That is usually where it starts.

Late-night scrolling can add another layer. After a long day, a person may check email, see a subscription renewal, and tell themselves it will be handled after one more video or one more message. The banking app is still open somewhere in the background, but the decision to move money or confirm a payment keeps getting pushed behind lower-effort behavior. The account does not look urgent, so the brain keeps choosing the easier path.

Payday moments create their own version of this pattern. When money lands, it can feel like the month has reset, which makes the first few decisions easier and the later ones less visible. A bill management system that seemed fine on the first day of the pay cycle can become looser near the due date, especially if the person has already covered subscriptions, a debt payment, and a couple of small convenience purchases. The tension is not a shortage of intention; it is a shortage of fresh mental bandwidth.

Unexpected expenses make the pattern even more noticeable. A car repair, school fee, or pharmacy charge can occupy the same mental space as a bill that was supposed to be automatic. The person may know the utility payment is due, but the brain keeps returning to the item that feels more immediate or more uncertain. That does not mean the bill was forgotten in any dramatic sense. It means the mind had to choose which concern to hold first.

Mid-evening is often the worst time for this kind of work because the day has already used up the person’s attention. The bill may require a quick transfer, but even quick transfers ask for concentration, and concentration is exactly what has been spent on work emails, family schedules, and the small decisions that fill ordinary life. A savings account, a credit card, and a bank balance can all be visible at once, yet the act of deciding what to do with them still takes more energy than expected. The sequence matters more than the amount.

What Actually Helps

The most useful adjustment is to remove as many near-due-date choices as possible. When bill payments are handled on a fixed day or at a fixed time, the brain has less to renegotiate each month, and that reduction in friction can matter more than motivation. Automation helps here because it keeps some decisions from appearing at the moment when decision fatigue is strongest. The point is not to become perfectly hands-off; it is to stop asking tired attention to solve the same question repeatedly.

It also helps to separate review from action. Looking over the monthly budget, checking the bank balance, and deciding what gets paid can happen earlier in the month, while the actual payment can happen later on a routine schedule. That split gives the mind a clearer job instead of one oversized task that keeps getting postponed. It feels smaller, and small matters when the day has already been full.

A second adjustment is to place bill payment in the part of the day when the mind is least crowded. For many people, that means earlier rather than later, before work messages, grocery trips, and late-night scrolling have used up attention. A payment handled before the day fills up is less likely to get buried under decisions that seemed unrelated at first. The timing does not need to be ideal; it just needs to be more protected than the default.

A third adjustment is to make the order of payments boring. When every bill has a predetermined place in the sequence, there is less room for mental debate about which one feels most urgent today. That does not remove the reality of due dates, but it keeps the payment process from becoming a fresh negotiation every cycle. A simple rule can preserve energy for the parts of money management that genuinely need thought.

It can also help to keep one buffer between the checking account and the rest of the month. Even a modest cushion can make bill management feel less like a race against the calendar, because the person is not forced to solve every timing issue with the same balance. That buffer is not a cure for poor timing, but it can reduce the number of decisions that arrive with the due date. A savings account used this way becomes less about ambition and more about preventing one small delay from turning into three.

Finally, it helps to respect the point where attention starts to fray. When a person notices that they are rereading the same bill, opening and closing the banking app, or postponing one more transfer, the issue may not be discipline at all. It may simply be that the day has already used up the mental fuel needed for ordinary bill management. By then, the bill is still the bill, but the person handling it is no longer operating with the same clarity they had earlier in the month.

The account can stay ordinary while the sequence around it changes. That quiet shift is often the whole story.

Related Reading

- Why You Keep Delaying Bills—Even When You Know They’re Due (Decision Fatigue)

- Credit Card Bill Surprise: When the Budget Seemed Fine

- Saving After the Cart Added Up and the Bills Stayed

Keep Exploring the Pattern

Watch more breakdowns of real-life money behavior on our YouTube channel.

If bill timing keeps creating pressure, try the Bill Due Date Planner to map out when your payments hit each month.

Disclaimer:

This content is for educational and informational purposes only and does not constitute financial advice. Always consult a qualified financial professional before making personal financial decisions.