The groceries are still on the counter, the delivery charges are already forgotten, and the bank balance is being checked before the next bill lands. Saving money after a shopping spree can start looking less like a plan and more like a series of quiet tradeoffs, one urgent expense at a time.

Why This Happens

Saving money after a spending surge usually becomes difficult because the money is no longer sitting in one neat place waiting to be saved. It has already been assigned, partly by habit and partly by circumstance, to the next utility bill, the grocery run, the school fee, or the car repair that could not wait. That is why the monthly budget can feel stable on paper and unsettled in real life. The tension is simple: the intention to rebuild savings is still there, but the account is already being pulled in several directions.

A spending spree does not only reduce the balance; it changes the emotional shape of the next few weeks. After a burst of convenience purchases, late-night scrolling, or a few too many delivery app orders, people often move into a quieter phase where they start watching every transaction more closely. That shift can make ordinary expenses feel larger than they are because the savings account suddenly looks fragile. It does not feel like a mistake at the time. It feels like the month has become a little less forgiving.

The research on savings behavior helps explain why this feels so sharp. The Federal Reserve reported that only 48 percent of adults said they could cover a $2,000 expense using savings, while 55 percent said they had rainy-day savings for three months of expenses. Those numbers point to a common gap between what people hope their savings can do and what the account can actually handle right away. When urgent expenses arrive after overspending, that gap becomes visible all at once.

This is where saving money often turns into a mental balancing act rather than a financial one. The person is not just deciding whether to save; they are deciding whether to save after the rent, the credit card payment, the pharmacy bill, and the grocery run have all taken their share. The plan was to rebuild, but the week kept adding reasons to postpone. That is usually where it starts.

The main pressure is that urgent spending is never abstract. A car tire does not wait for a better savings month. A subscription renewal, a school supply run, or a higher-than-expected insurance payment arrives with its own deadline. The budget feels as if it should absorb all of it and still leave room for progress, yet real life keeps arriving before the spreadsheet can catch up.

Common Mistakes People Make

The first pattern is treating savings as the leftover category after everything else has already happened. That sounds disciplined, but in practice it often means saving only when the month is unusually calm. Once a grocery trip runs high or a repair shows up, the savings transfer gets pushed back again. The intention is still there, but the timing keeps getting defeated by ordinary life.

The second pattern is trying to recover from overspending by cutting too hard in the next few days. People may skip needed groceries, delay a medical copay, or let a credit card balance drift because they want to protect the savings account at all costs. The tension is that the effort to stay committed can create more pressure later. A too-tight plan often breaks on the first real inconvenience.

The third pattern is pretending every expense can be managed the same way. A birthday dinner, an appliance repair, and a higher gas bill all behave differently in a monthly budget, but they are often treated as if they can simply be absorbed by spending less somewhere else. That leads to a false sense of control, especially when debit card charges and bank alerts keep arriving faster than the budget tracker can be updated. The month looks manageable until the actual timing of the bills shows up.

Each of these patterns tends to come from the same place: the desire to feel back on track quickly. After a shopping spree, the urge is to repair the account immediately and prove that the damage was temporary. But money does not usually respond to urgency in the same way people do. It responds to cash flow, due dates, and whatever the bank balance happens to be at the moment.

There is also a quieter problem hiding underneath all three patterns. When savings are treated as the only sign of progress, every urgent expense feels like a setback rather than a normal event in a working financial life. That can make people overreact to one week and underprepare for the next. The behavior is understandable, but it can keep the cycle going.

What makes these mistakes feel familiar is that they rarely look reckless from the inside. They look temporary, practical, and reasonable in the moment. The grocery receipt is high, but the household still needs food. The credit card payment is due, but the savings transfer can wait until payday. That is how the budget slowly starts to absorb exceptions until the exceptions become the pattern.

Real-Life Patterns and Behaviors

The most recognizable version of this cycle starts at the grocery store. A person goes in to buy essentials, then adds a few convenience items because the week has already been exhausting. By the time the receipt prints, the total has crossed the number that felt safe in the morning. Saving money after that kind of trip is not about willpower alone; it is about the fact that the bank balance now has less room for both food and savings.

A similar pattern often shows up around payday. The paycheck lands, a few bills are paid, and the account finally looks less tense. That is usually when the mind starts to relax and small spending decisions feel harmless again. Then the next urgent expense appears, and the savings transfer never quite gets its turn. The account looked fine. That was usually when it slipped.

Delivery app spending creates its own version of the same problem. The order itself feels small because it solves a tired evening, a late workday, or a missing grocery item without much effort. The issue is not the single order; it is the way repeated convenience charges quietly reduce the amount available for savings goals and debt payments. By the time the pattern becomes visible, the month is already carrying the result.

Subscription renewals can do the same thing without much attention at all. A streaming service, a cloud storage fee, or a household app charge may be easy to ignore until several similar charges land in the same week. That is when the monthly budget starts to feel less like a plan and more like a list of things that already decided themselves. Recognition comes late because none of the charges feels large on its own.

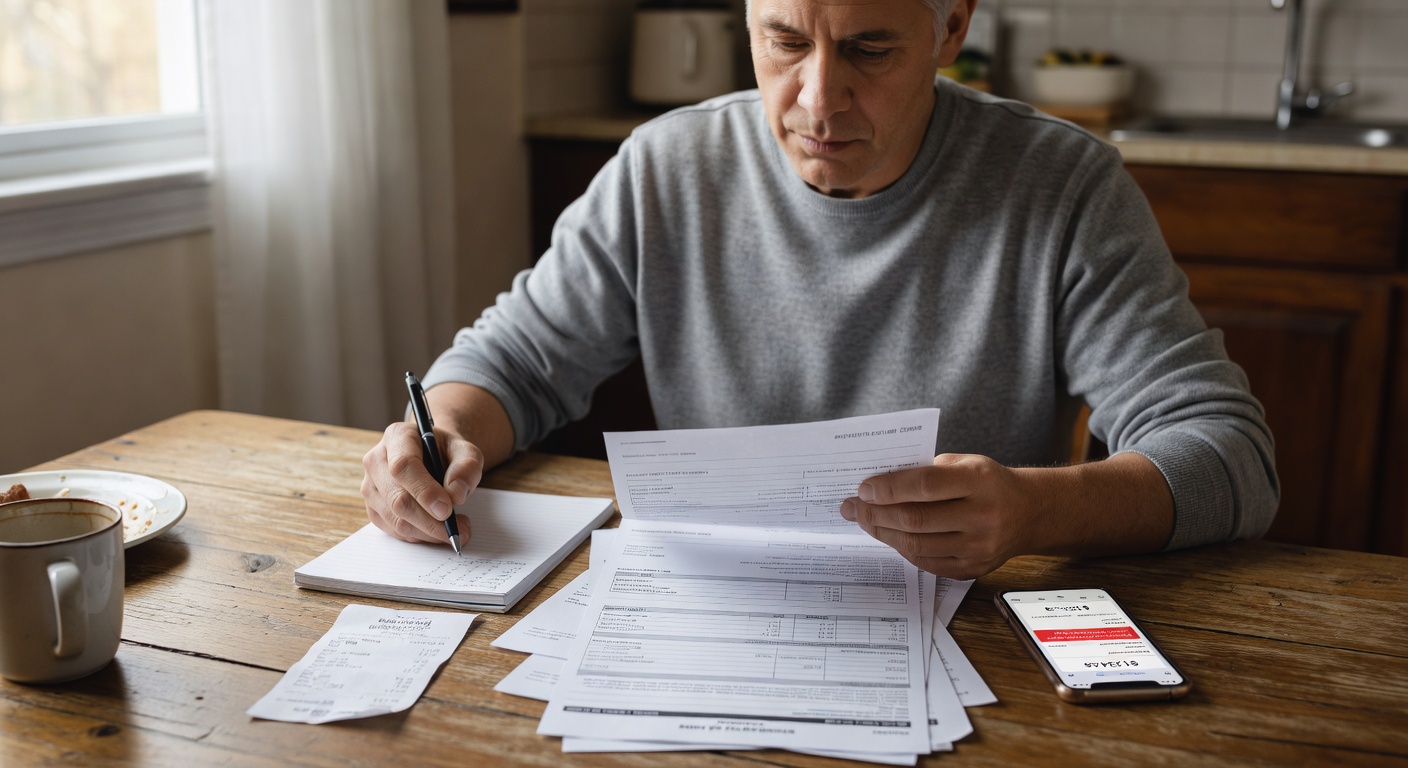

The most revealing pattern may be the mid-month balance check. Someone opens the banking app, sees that the number is lower than expected, and immediately starts mentally rearranging the rest of the month. The reaction is rarely dramatic; it is usually a quiet recalculation of what can be delayed, reduced, or postponed. That moment carries the real tension, because the need to save money is still present while the immediate cash flow is already spoken for.

What Actually Helps

What tends to help first is separating urgent expenses from guilt. A car repair, a pharmacy bill, or a utility payment is not solved by wishing the spending spree had gone differently. Once the expense is real, the better question is what the account can handle without breaking the rest of the month. That shift matters because it stops savings from being treated as proof of discipline and starts treating it as one part of a larger monthly budget.

It also helps to make the savings goal smaller for a while instead of abandoning it. The point after overspending is usually not to rebuild everything at once, but to keep the habit visible while the balance stabilizes. A modest automatic transfer can preserve the pattern of saving money without pretending the account is in the same shape as before. That makes room for groceries, insurance, and debt payments without turning every expense into a crisis.

A separate spending category for unavoidable costs can reduce the feeling that every surprise is an emergency. When irregular expenses are expected to appear somewhere in the plan, they stop knocking the savings account off course so violently. This matters for things like school fees, annual renewals, and small repairs that do not fit neatly into a weekly budget. The behavior changes because the money already has a place to go before the bill arrives.

It also helps to slow down the rebound phase after a shopping spree. People often feel pressure to become extremely frugal for a few days and then return to normal spending once the balance improves a little. That cycle can make the bank account look better briefly while keeping the underlying pattern untouched. A steadier adjustment, especially around convenience purchases and credit card use, tends to create more consistency than a dramatic reset.

The next useful shift is to watch timing instead of only totals. A budget can look acceptable in the month as a whole and still fail because several charges cluster before payday. That is why mid-month checks can be more useful than waiting for the statement to close. The issue is often not that there is no money at all; it is that the money is arriving and leaving in the wrong order for the plan.

For many households, the real answer is to protect a small savings account while accepting that some months will be uneven. That does not mean lowering standards or giving up on financial planning. It means recognizing that a working budget has to survive bill payments, groceries, and the occasional repair without pretending every week can be perfectly balanced. The month keeps moving whether or not the spending does.

Related Reading

- Unexpected Bills After a Shopping Spree Leave Savings Thin

- Saving for Rent and Still Clicking That Sale Tag

- Family Getaway Costs More When the Itinerary Shifts

Keep Exploring the Pattern

Watch more breakdowns of real-life money behavior on our YouTube channel.

If bill timing keeps creating pressure, try the Bill Due Date Planner to map out when your payments hit each month.

Disclaimer:

This content is for educational and informational purposes only and does not constitute financial advice. Always consult a qualified financial professional before making personal financial decisions.