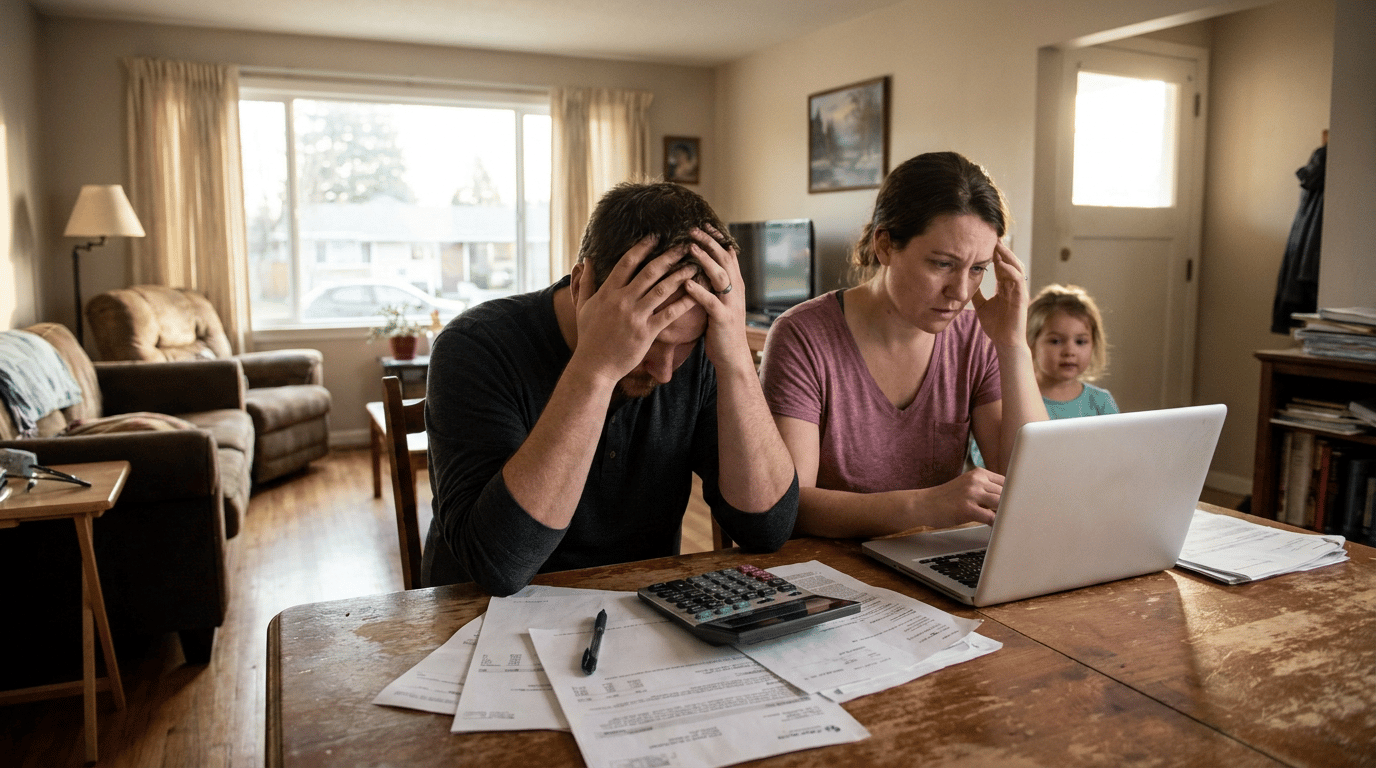

The dentist calls back just as the grocery app subtotal is sitting on the screen, and the rest of the evening starts to rearrange itself around one unexpected family expense. The monthly budget was built for rent, insurance, credit cards, and all the ordinary repeats — not the thing that arrives midweek and asks for attention right away.

Why This Happens

Unexpected family emergency expenses do more than remove cash from a checking account. They interrupt the sequence that most budgets rely on, where bills arrive in roughly the same order and spending can be planned around a predictable pay cycle. When the sequence changes, the whole money routine starts to wobble, even if the numbers on paper looked fine earlier in the month. That is usually where it starts.

The first reason this happens is that most budgets are built for regularity, not interruption. A person can account for utilities, groceries, and debt payments with care, yet still have very little space for a hospital copay, a damaged phone, or a last-minute trip related to a family emergency. The issue is not simply that the expense is large. The issue is that it arrives without warning and asks to be paid before the rest of life has adjusted.

Pew’s research on financial shocks makes this pattern clearer, noting that unexpected expenses and income losses can create immediate strain and make it harder to build or rebuild a cushion. It also found that more than a quarter of people said these challenges made it hard for their household to save money most months. That matters because the emergency does not end when the bill is paid; it can change the next several paydays too. A savings account that felt adequate on a calm afternoon can feel very small once the family calendar turns urgent.

There is also a quiet mental effect that people often miss. Families tend to treat an emergency as a temporary event, but the budget experiences it as a chain reaction: one withdrawal, then a transfer, then a delayed bill, then a card balance that sits higher than expected. The mind wants to focus only on the immediate need, while the bank balance records the entire sequence. The gap between those two views is where the stress tends to hide.

Unexpected family emergency expenses can also expose how thin the margin was before the event happened. A household may appear stable because the rent gets paid and the subscriptions keep renewing, yet the actual flexibility may be fragile. Some people only notice this when the emergency requires a credit card or a short-term loan, and the next statement arrives with less room than expected. The budget did not collapse all at once; it lost shape in small pieces.

Common Mistakes People Make

The first pattern is trying to make the emergency disappear by treating it as a one-time exception. A parent pays the bill, moves money from savings, and tells themselves the month can absorb it because the event is over. That sounds reasonable in the moment, and it often feels like the most responsible response. The trouble is that the rest of the budget still has to live through the aftermath.

When a family emergency expense is handled as a sealed-off event, later spending gets less visibility than it should. The grocery trip runs a little higher, the gas tank gets filled without much thought, and a few auto-renewing charges keep moving in the background. None of those choices feels connected to the emergency, which is exactly why they matter. The original bill is gone, but the recovery cost is still unfolding.

A second common habit is using the easiest account instead of the most sustainable one. The checking balance looks available, so the money comes from there; if that is short, the credit card covers the gap. That choice does not feel careless at the time because the goal is simply to solve the immediate need. Yet every quick fix can change the next due date, the next statement, and the next mid-month balance check.

This becomes even more noticeable when people tell themselves they will sort it out after payday. The plan is not irrational; it is often the only available option. But the budget rarely resets cleanly after a surprise. If the emergency was large enough to displace savings, it usually leaves behind a quieter layer of disruption that shows up in the following weeks.

The third pattern is waiting too long to acknowledge the secondary costs. A family emergency rarely involves only one payment. There may be transportation, prescriptions, child care adjustments, missed work time, or extra food spending around the event. Those extras can feel minor in isolation, but together they create the kind of cash flow gap that is hard to spot until the account is already lower than expected.

That is the part that tends to go unnoticed. People often track the obvious bill and ignore the smaller friction around it because the smaller items do not seem serious enough to record. By the time they are visible, the month has already absorbed them. A budget tracker can only help if the whole event is being seen, not just the headline cost.

Real-Life Patterns and Behaviors

One familiar scene is the grocery run that starts normally and ends with a phone call from a relative, a pharmacy pickup, or a request to cover something urgent before the weekend. The cart still gets filled, but now every item has to compete with an unplanned family emergency expense that was not part of the original plan. The tension is not dramatic; it is practical and immediate. The receipt is the same length, but the feeling at checkout is different.

People often respond by trimming the visible spending and leaving the hidden spending untouched. They may cut a restaurant order, skip a few extras at the store, or pause a subscription, while the emergency-related charges continue through a credit card or debit withdrawal. This creates the illusion that control has returned, even though the budget is still absorbing the event. The account balance knows the difference even when the person trying to manage it does not.

Another common setting is the middle-of-the-month bank balance check. The number looks lower than expected, and the first thought is usually to blame regular spending rather than the emergency that shifted everything a week earlier. That reaction makes sense because ordinary purchases are easier to remember than one larger interruption. Still, the sequence matters more than the single transaction, especially when insurance, copays, or travel costs were involved.

Subscription renewals also reveal the pattern. A family may keep paying streaming services, delivery apps, or a budgeting app because those charges are small and familiar, even while larger expenses are forcing the monthly budget to stretch. The surprise is not that these renewals exist; it is that they keep happening while the household is in recovery mode. Small automatic charges are easy to ignore when life is calm, but they become more noticeable when every dollar has a job.

Payday moments can be especially revealing after an emergency. The deposit arrives, the account briefly looks repaired, and then the outstanding bills, debt payments, and replenishment transfers begin to move again. The money was never really free to use, but the emotional effect of seeing a larger balance can make it feel that way for a short time. That is how the budget gets revised without anyone deliberately deciding to revise it.

The pattern also shows up in households that think of themselves as financially organized. They may have a monthly budget, a savings account, and a good sense of where money usually goes, yet an unexpected family emergency expense can still set off a chain of small compromises. The compromises do not look reckless. They look like ordinary life continuing under changed conditions, which is exactly why they are so easy to miss.

What Actually Helps

What helps first is treating the emergency as more than the bill in front of it. The expense itself matters, but so do the related costs that follow it through the month. A household does not need perfect forecasting to benefit from seeing the full sequence more clearly. When the event is mentally expanded beyond the first payment, the budget stops being surprised twice.

A separate place for emergency money tends to work better than hoping the checking account will absorb everything. That does not have to mean a large fund right away; even a modest savings account with a clear purpose changes the way decisions get made. The point is less about building a perfect buffer and more about reducing the need to improvise every time a family crisis appears. The money behaves differently when its job is already defined.

It also helps to pause before letting one account solve every part of the problem. A credit card can bridge timing, but it can also leave the household carrying the event longer than expected. A short conversation with the bank balance, the monthly budget, and the next few due dates often reveals whether the expense needs to be split across pay cycles instead of absorbed at once. That small shift can make the aftermath feel less chaotic.

People also do better when they update the budget instead of pretending the month is still normal. A budget tracker is useful not because it prevents surprises, but because it shows which categories were quietly affected. If groceries, gas, child care, or debt payments need to be adjusted for a few weeks, it is easier to do that early than to wait for the account to reveal the change on its own. The goal is not a perfect spreadsheet; it is a clearer read on the shape of the month.

Insurance and routine account reviews matter here too, even when they are not exciting. A family emergency expense is easier to absorb when health coverage, auto coverage, or other basic protections are not left vague in the background. The same is true for keeping an eye on recurring charges and stale subscriptions that continue draining money during a sensitive period. Quiet financial maintenance does not feel dramatic, but it often decides how wide the gap becomes after the surprise.

The final adjustment is psychological rather than technical. People often judge themselves for not being ready, when the more accurate observation is that most budgets are built for repetition, not interruption. That is why the unexpected family emergency expense can feel so disorienting even in households that usually manage money well. The month keeps moving whether or not the spending does.

Related Reading

- Emergency Fund Too Small After a Costly Week

- Holiday Car Repairs and the Budget That Starts Slipping

- New Baby Budget Shock: When Baby Costs Change Everything

Keep Exploring the Pattern

Watch more breakdowns of real-life money behavior on our YouTube channel.

If you want a clearer view of where your income goes each month, try the Salary Breakdown Calculator.

Disclaimer:

This content is for educational and informational purposes only and does not constitute financial advice. Always consult a qualified financial professional before making personal financial decisions.