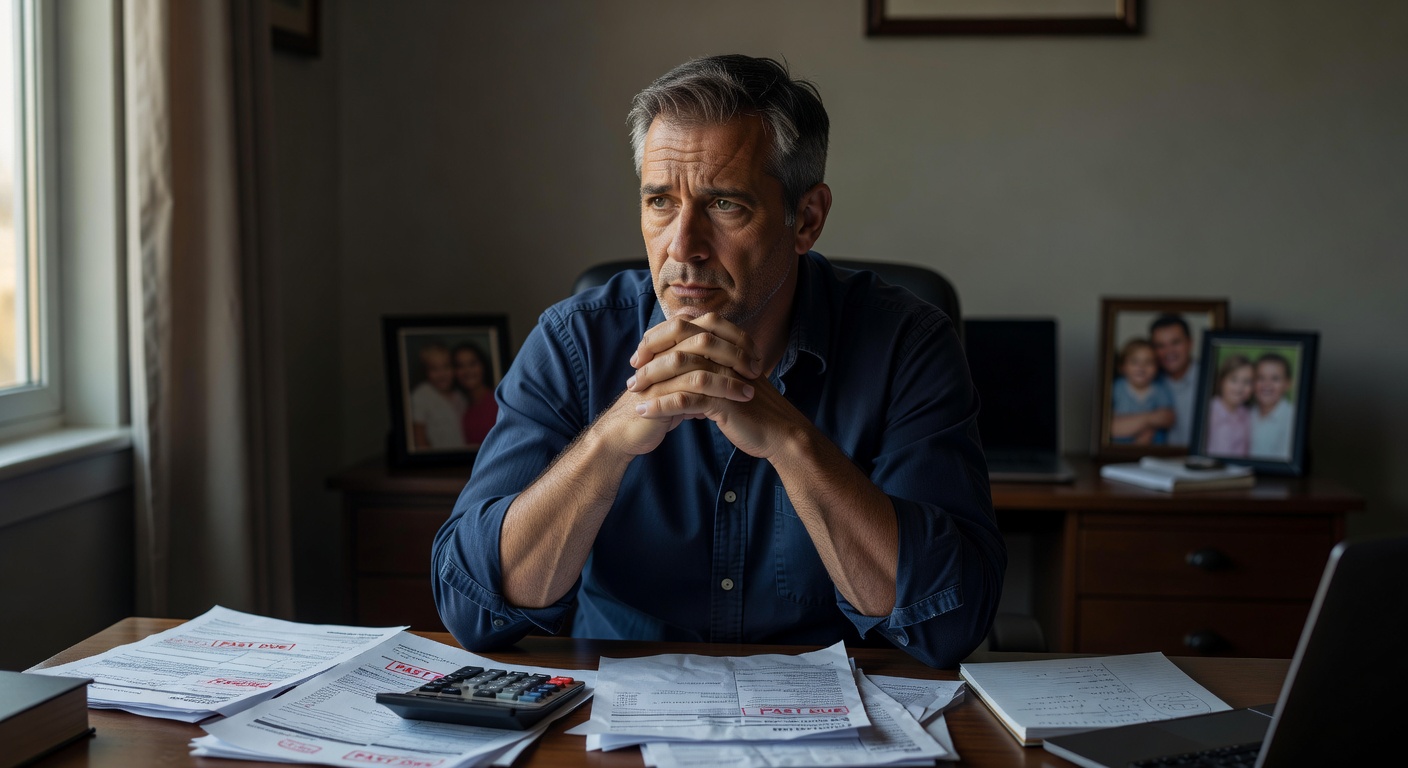

He comes home, sets his keys down, and answers “fine” when someone asks how work was. The bills are in his head before dinner is even served, and the stress stays there because that is what he thinks a father is supposed to do. If you have ever wondered why fathers quietly carry financial stress alone, the answer is usually less about money and more about the roles they feel forced to play.

Why This Happens

A lot of fathers do not announce financial stress because they have learned that silence looks steadier than honesty. In many homes, the father becomes the default absorber of money pressure, even when both adults are affected by the same bills, the same inflation, and the same uncertainty. He may not say much, but he is tracking everything: the mortgage, the car repair, the school fee, the grocery total, the holiday spending, and the timing of each paycheck.

What makes this pattern so persistent is that it often feels like responsibility rather than secrecy. A father may believe that if he stays calm, everyone else can stay calm too. That belief can become a habit, and the habit can harden into identity. Over time, he does not just carry financial stress alone; he starts to think carrying it alone is part of being dependable.

There is also a social script at work here. Many men grew up hearing that providing is proof of love, while emotional visibility is something to be managed or minimized. So when money gets tight, the instinct is not to talk. The instinct is to tighten, suppress, and keep moving. On the surface, that looks like control. Inside, it often feels like quiet pressure with no exit.

This is where the emotional search behind the question really lives. People are not only asking, “Why is my husband stressed about money?” or “Why do fathers worry about finances in silence?” They are asking why the stress seems so private, even when the household problem is shared. The answer usually starts with role pressure, then moves into shame, and then settles into routine.

The Hidden Pattern Behind It

The hidden pattern is that financial stress often becomes invisible before it becomes dramatic. A father may not say he is overwhelmed, but his behavior changes in small ways long before anyone names it. He may delay repairs, avoid looking at the account too often, or become unusually defensive when spending comes up. Those small reactions are not random; they are signs of an internal calculation happening all the time.

The pattern usually follows a simple loop:

– He notices the pressure early.

– He keeps it to himself to avoid worry or conflict.

– He manages it quietly through overwork, delay, or mental juggling.

– The household reads his silence as calm.

– He becomes the only person carrying the full emotional load.

That loop can repeat for years because it creates the appearance of stability. A father who never mentions money trouble may be seen as strong, but the silence can hide real strain. Instead of asking for support, he may try to solve everything by pushing harder, cutting personal spending, or working longer hours. The household looks functional, but the pressure keeps accumulating underneath.

This is usually where people realize their money is not random, it is patterned. The pattern is not just about how much is earned. It is about how stress is processed, where it is stored, and who is allowed to know about it. In many families, the father becomes the place where uncertainty goes to disappear.

There is also a psychological trap in being the problem-solver. If a man is used to being the one who fixes things, admitting financial stress can feel like admitting failure. That feeling can be stronger than the stress itself. So the mind chooses temporary privacy over uncomfortable truth, even when truth would actually reduce the burden.

Common Mistakes People Make

One common mistake is assuming silence means the father is not struggling. In reality, many fathers become quieter precisely when the pressure is highest. They may look stable because they are trying to protect others from worry, but that protection can create distance. The family senses something is wrong, yet no one has a clear name for it.

Another mistake is turning financial stress into a character judgment. People may say he is controlling, withdrawn, or emotionally unavailable without recognizing the pattern underneath. Sometimes those behaviors are symptoms of money anxiety, not separate personality flaws. That does not excuse harmful behavior, but it does explain why the same stress keeps showing up in the same form.

A third mistake is treating the issue as if better budgeting alone will solve it. Budgeting helps, but a father who is carrying stress in silence may not need only a spreadsheet. He may need a safer way to talk about uncertainty without feeling stripped of his role. A budgeting tool or monthly money tracker can clarify the numbers, but it cannot replace the emotional permission to be honest.

People also make the mistake of waiting for a crisis before paying attention. By the time the issue becomes obvious, the father may already have spent months absorbing pressure privately. He may have already skipped personal needs, postponed expenses, or absorbed the emotional tension of several conversations he never had. The real cost is not just financial. It is the long period of being alone with it.

Real-Life Patterns and Behaviors

You can often spot this pattern in ordinary life long before anyone says the words out loud. He checks bills late at night when the house is quiet. He opens the bank app, closes it, and opens it again, hoping the numbers feel different the second time. He says no to things without explaining why, then makes the refusal sound practical instead of scared.

Another common behavior is over-functioning. He takes on extra hours, extra tasks, or extra responsibility because action feels easier than conversation. This can look admirable from the outside, and sometimes it is admirable, but it can also be a form of pressure avoidance. Work becomes the place where anxiety gets converted into motion.

A different pattern shows up in spending decisions. He may be careful about family expenses but strangely reluctant to spend on himself. New shoes wait, medical appointments wait, and small personal purchases feel indulgent. This is not always frugality; sometimes it is self-erasure dressed up as discipline. When a man believes his needs are optional, money stress becomes even harder to name.

The emotional pattern is often just as clear as the financial one. He may become shorter with people, more tired than expected, or oddly detached during money conversations. He may also insist that everything is fine when the behavior says otherwise. That mismatch is often the clue. The words say calm, but the pattern says containment.

What makes this so hard is that the family may adapt to the silence. If no one asks, no one has to answer. If he keeps managing, others can keep assuming. Over time, the household can become organized around his hidden stress without ever consciously naming it. That is how money pressure becomes a family atmosphere instead of a single conversation.

What Actually Helps

What helps first is not a perfect budget, but a visible one. When money stress lives only in one person’s head, it grows larger and more emotional than it needs to be. Writing down the actual numbers in a simple tracking tool or budgeting tool can reduce the mental fog immediately. Not because the numbers are easy, but because they stop floating around as fear.

The next helpful shift is making stress discussable before it becomes urgent. That does not mean turning every dinner into a financial review. It means creating a calm, regular moment where money is just another household topic, not a crisis topic. When fathers are allowed to speak early, they are less likely to carry everything alone until it turns into resentment or burnout.

It also helps to separate provision from perfection. Many fathers quietly believe they have to provide without pause, without uncertainty, and without visible strain. But real financial stability is not the absence of stress. It is the ability to notice stress early and respond before it hardens. That is a different skill, and it can be learned.

For some families, the most useful step is not cutting more expenses but naming the pattern itself. Once the pattern is visible, the conversation changes. Instead of “Why are you always tense about money?” it becomes “We both know this is heavy, so how do we handle it differently?” That shift alone can reduce the private burden. It turns a hidden job into a shared one.

This is also where calculators can be useful in a very human way. A debt payoff calculator, savings goal tracker, or monthly cash flow tool does more than organize data. It gives the brain something concrete to hold onto when emotion is trying to fill every space. The goal is not control for its own sake. The goal is relief through clarity.

What To Do Next

If this pattern feels familiar, start by noticing where the stress lives in your routine. Is it in the silence after work, the late-night account checks, the reluctance to spend on yourself, or the way you keep saying “I am handling it” when you are actually tired? Naming the pattern is not weakness. It is usually the first moment real change becomes possible.

Then make the money visible in one simple place. A basic budgeting tool, a bill tracker, or a calculator for debt and savings can turn vague pressure into something you can actually see. Once the numbers are visible, the emotional load usually becomes easier to discuss because it is no longer just a feeling. It is a pattern with shape.

If you are the one carrying this quietly, consider one honest conversation this week. Not a dramatic one. Just enough to stop pretending the stress belongs to you alone. And if you are the person living beside that silence, lead with curiosity instead of correction. That small shift can make money feel less like a private burden and more like a shared plan.

Related Reading

- Why Working Fathers Never Feel Financially Relaxed

- Why Men Over 40 Stop Feeling Financially Secure

- Why Money Arguments Feel More Personal Than Financial

Keep Exploring the Pattern

Watch more breakdowns of real-life money behavior on our YouTube channel.

Browse the full Money Behavior Library to explore more patterns like this one.

If you want a clearer view of your monthly patterns, try the Salary Breakdown Calculator, the Subscription Cost Calculator, or the Bill Due Date Planner.

Explore more patterns in the Money Behavior Library — a growing collection of real-life financial patterns explained clearly.

Disclaimer:

This content is for educational and informational purposes only and does not constitute financial advice. Always consult a qualified financial professional before making personal financial decisions.