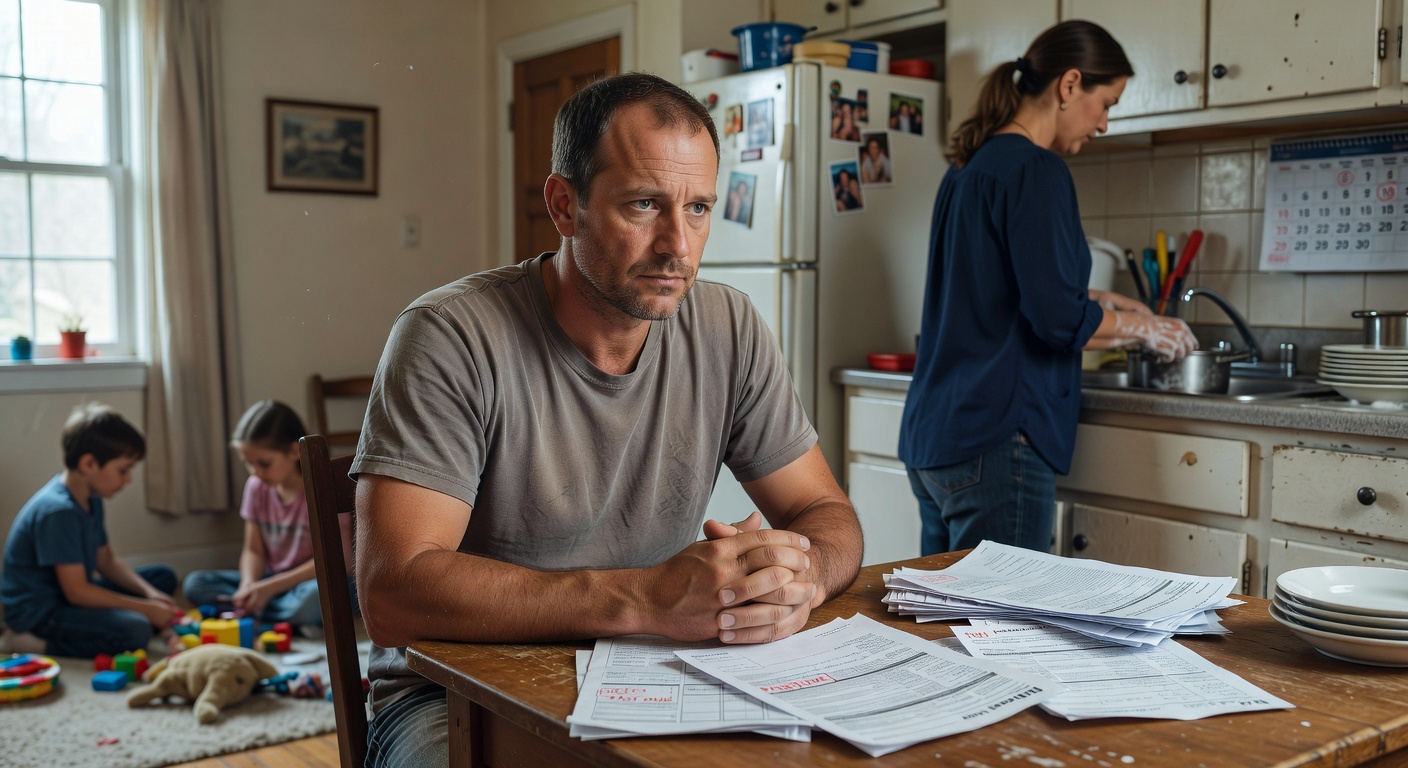

It happens in the grocery aisle, or when the utility bill arrives, or when your child needs something that used to feel ordinary. You look at the numbers and realize that providing for a family now feels heavier, more complicated, and more emotionally loaded than it used to. That feeling is not just about money; it is about pressure, timing, and the quiet way daily life has become more expensive in every direction.

Why This Happens

The feeling that providing for a family is harder than ever usually starts long before a person says it out loud. It shows up as a small internal flinch when prices have jumped again, when a child outgrows clothes faster than expected, or when one extra expense pushes the whole month off balance. What makes this so difficult is that it does not feel like one problem. It feels like many small problems arriving at once, each one asking for attention.

For a lot of middle-aged adults, the emotional burden is not just the size of the bill. It is the memory of a different financial reality. Many people remember a time when a single income could cover more, when savings felt more reachable, and when family spending seemed easier to predict. Now the same person may be earning more on paper but feeling less secure in practice, which creates a confusing mismatch between effort and outcome.

That mismatch is what makes this issue feel so personal. When someone is working hard, managing a household, and still feeling behind, they do not just think, “Everything is more expensive.” They think, “Why am I still struggling if I am doing what I am supposed to do?” That thought carries shame, frustration, and fatigue all at once.

The real answer is not that people became worse at handling money. The answer is that the structure around family life changed. Housing, childcare, food, insurance, transportation, and even school-related costs have all risen in ways that compound each other. A family budget is not just one category; it is a system, and when several parts of that system rise together, the pressure becomes hard to ignore.

This is where many people start to feel financially stuck. They are not being careless. They are reacting to a landscape that is less forgiving than it once was, and their daily decisions have become more reactive because the margin for error is thinner than before.

The Hidden Pattern Behind It

The hidden pattern is that providing becomes harder not only because expenses rise, but because the emotional role of provider expands. Once a person sees themselves as the one who must keep everything steady, every purchase starts to carry moral weight. A grocery run is no longer just groceries. It becomes a test of discipline, care, and whether the household is safe for another week.

This is usually where people realize their money is not random; it is patterned. The same stress that makes them overcheck their account can also make them overspend on a “fix” that brings brief relief. The same pressure that makes them delay one bill can make them feel like they must compensate by buying something for the family later. Money behavior often swings between control and comfort, especially when someone feels responsible for everyone else.

A common pattern looks like this:

– Income arrives, and relief lasts for a few days.

– Expenses appear faster than expected, and the mood shifts.

– The provider role feels heavier, so small treats or urgent purchases feel justified.

– The budget gets tighter, and the cycle starts again.

The important thing is not the specific purchase. It is the emotional loop underneath it. When people feel stretched, they often try to restore dignity through spending, even if the purchase does not truly solve the pressure. That is why family finances can feel exhausting even when the numbers are technically “under control.”

Another hidden pattern is mental load. One person in the household often becomes the default planner, reminder system, and emergency responder all at once. They are tracking school dates, birthdays, repair costs, groceries, prescriptions, and the invisible timing of bills. That mental load drains attention, and when attention is drained, budgeting becomes harder to sustain.

In other words, the problem is not just lack of money. It is constant decision fatigue. And decision fatigue makes even good systems feel fragile.

Common Mistakes People Make

One of the most common mistakes is treating every money problem like a discipline problem. When people feel behind, they often respond by tightening every category at once, then feeling guilty when the plan does not hold. This creates a cycle where the budget becomes a punishment instead of a support tool, and that usually leads to rebellion or burnout.

Another mistake is assuming the answer is simply to “spend less” without looking at the emotional triggers behind spending. A family budget can fail even when the numbers are realistic if it does not account for stress, unpredictability, and the need for occasional breathing room. People do not only spend based on logic; they spend based on exhaustion, urgency, guilt, and the wish to protect the people they love.

A third mistake is underestimating how often people use comparison as a measure of failure. They compare their current life to a previous version of themselves, to neighbors, to friends, or to a remembered standard that may no longer exist. That comparison can make ordinary expenses feel like evidence of personal weakness, when in reality they are often evidence of a changed economy and a changed stage of life.

The fourth mistake is waiting too long to notice the pattern. Many households do not realize there is a recurring pressure point until the bank balance, the credit card, or the monthly leftover money tells the story for them. By then, the stress has already become emotional, not just mathematical.

When people miss the pattern, they tend to blame the symptom. They say, “We need to be stricter,” or “I just need more self-control.” But the pattern is usually deeper: over-responsibility, shrinking margin, surprise costs, and the quiet expectation that one person should absorb the whole load.

Real-Life Patterns and Behaviors

If this feels familiar, it is because many households follow the same sequence without naming it. The money comes in, the calendar fills up, and the family starts spending in response to needs that do not wait politely. The result is a life where the budget is constantly negotiating with reality.

Here are some of the most common real-life behaviors behind the feeling that providing has become harder:

– Delaying personal needs so the family can be covered first.

– Treating every unexpected cost as a setback instead of a normal event.

– Feeling relief after paying one bill, then anxiety when the next one appears.

– Using shopping or convenience spending to recover from stress.

These behaviors are not signs of failure. They are signs of a nervous system trying to cope with responsibility. A person who feels like the household anchor often becomes more reactive with money, not less, because the stakes feel too high to stay emotionally neutral.

There is also the behavior of quiet sacrifice. Many providers cut back on their own needs for so long that they stop noticing how depleted they are. They may not buy the replacement shoes, skip the appointment, put off the haircut, or ignore their own small comforts, all in the name of keeping the family stable. Over time, that sacrifice can become its own kind of pressure.

And then there is the behavior of overcorrecting. When the stress becomes visible, some people suddenly try to become extremely strict. They cancel everything, restrict every category, and try to fix months of tension in one weekend. The problem is that a family system built on constant deprivation usually does not last. It needs rhythm, not punishment.

This is why the same issue keeps returning. The problem is not that people do not care enough. The problem is that their patterns are built around reacting to fear rather than planning around reality.

What Actually Helps

What helps most is not a dramatic financial overhaul. It is noticing the repeating pattern before it turns into panic. When people understand the rhythm of their own money behavior, they can make calmer decisions, even if the numbers are still tight.

The first helpful shift is to separate the problem into layers. There is the math layer, the emotional layer, and the logistics layer. A household may need a budgeting tool for the math, a tracking tool for the patterns, and a simple conversation about what the family can realistically carry without constant strain. Those are different problems, and they need different responses.

A spending tracker or budget calculator can be useful here because it shows the shape of the month instead of just the final balance. Many people only look at what is left, but what matters more is when money disappears and why. If the problem is uneven timing, a calculator can reveal that. If the problem is a recurring category, tracking can expose it. If the problem is emotional spending after a hard day, the numbers will usually show that too.

The second helpful shift is to build in a small amount of flexibility on purpose. Families often fail budgets because they try to create a perfect system for an imperfect life. A plan with no room for real-world surprises usually collapses the first time the car needs something, the child needs something, or the week simply runs long.

The third helpful shift is to redefine success. If the old definition was “never feel stressed,” that will fail. A more realistic definition is “I can see the pattern, respond earlier, and keep the family steady without constantly feeling like I am behind.” That is a different goal, and it is much more sustainable.

This is the part many people miss: relief often comes from clarity before it comes from extra income. More money can help, of course, but without a clear pattern, more money can simply move the stress to a higher level. That is why families who feel broke at one income often still feel pressured after a raise. The structure has not changed yet.

What To Do Next

If this story feels uncomfortably familiar, start by looking at one month with fresh eyes. Do not ask only where the money went. Ask what kind of week produced the spending, what emotions came before the purchases, and which expenses are predictable but still feel surprising. That kind of review is often where the real pattern appears.

A simple budget calculator or spending tracker can help you do that without guessing. The point is not to become obsessive. The point is to make the invisible visible so the pressure stops feeling like a mystery. Once you can see the rhythm, you can stop treating every month like a personal failure.

If you want a practical next step, choose one tool and use it for one cycle: a household budget worksheet, a monthly expense tracker, or a calculator that shows where your money actually has room to breathe. That small act can change the conversation from “Why is this happening to us?” to “Now we can see the pattern.”

And that is usually where things begin to soften. Not because the world suddenly gets cheaper, but because the family stops carrying the stress in the dark. If you are ready, start with one clear picture of your numbers and let that be enough for now.

Related Reading

- Saving Money After a Shopping Splurge Feels Unsettled

- Family Getaway Costs More When the Itinerary Shifts

- Why Bill Management Falls Apart at the Last Minute

Keep Exploring the Pattern

Watch more breakdowns of real-life money behavior on our YouTube channel.

Browse the full Money Behavior Library to explore more patterns like this one.

If you want a clearer view of your monthly patterns, try the Salary Breakdown Calculator, the Subscription Cost Calculator, or the Bill Due Date Planner.

Explore more patterns in the Money Behavior Library — a growing collection of real-life financial patterns explained clearly.

Disclaimer:

This content is for educational and informational purposes only and does not constitute financial advice. Always consult a qualified financial professional before making personal financial decisions.