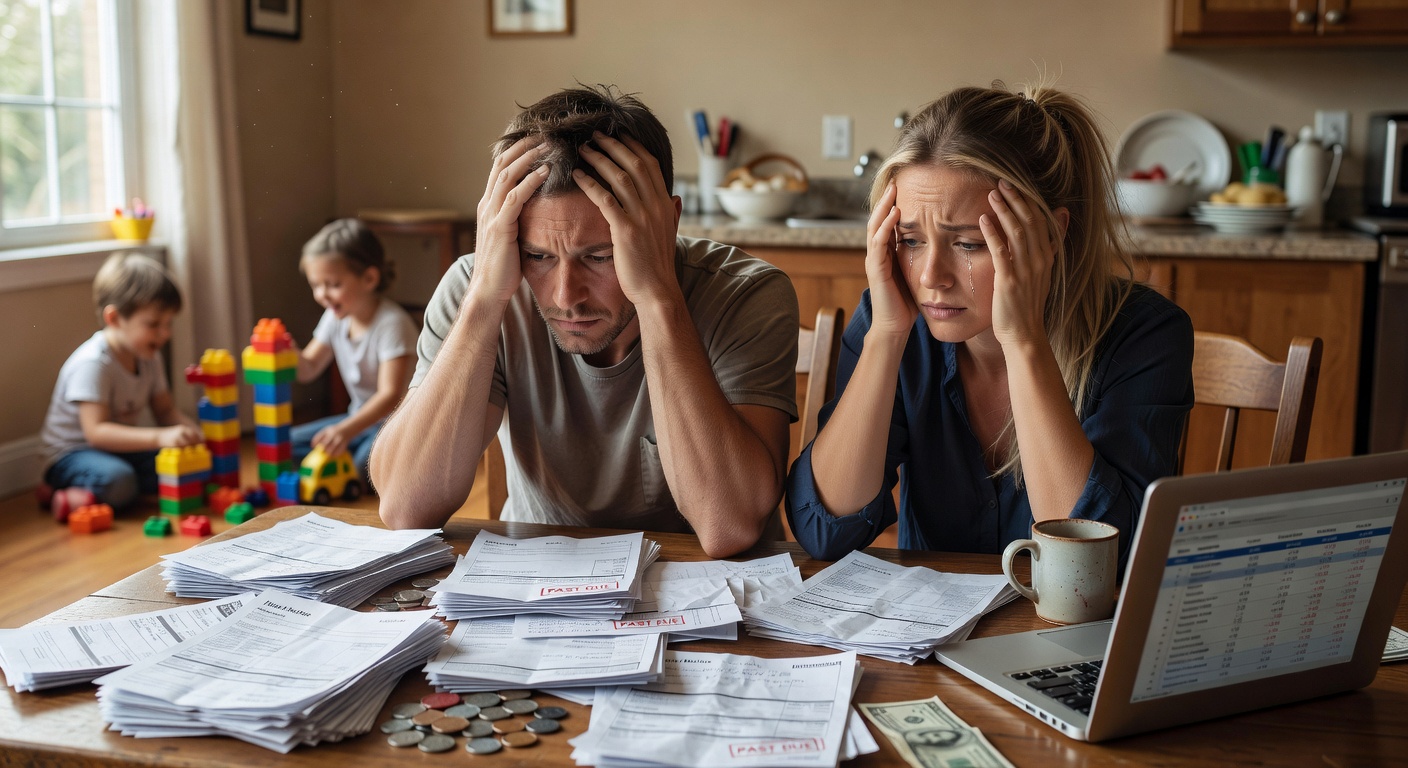

The first time a child needs something unexpected, the money stress changes shape. It is not just about the bill anymore; it is about the feeling that every choice now carries more weight than it used to.

Why This Happens

Financial stress often feels heavier after children because the stakes are no longer abstract. Before kids, a tight month can feel inconvenient; after kids, the same month can feel like a warning sign, as if one missed payment could ripple through the whole household. That shift is not weakness or bad planning. It is the mind responding to responsibility, visibility, and the constant awareness that someone else depends on your decisions.

A lot of parents describe the same quiet pressure: the grocery bill is higher, the calendar is fuller, and every small expense now competes with something that feels more important. The interesting part is that the stress is not only about actual spending. It is also about the mental load of tracking future needs, anticipating emergencies, and trying to stay one step ahead of surprises. That is why the same income can feel suddenly tighter once children enter the picture.

Children also make money more emotionally visible. You do not just notice your own wants anymore; you notice school fees, clothes, snacks, activities, childcare, and the slow accumulation of little costs that never used to matter. When money is tied to protecting a child’s comfort or stability, the brain treats it as a threat, not a budget line. This is usually where people realize their money is not random… it is patterned.

There is also a social layer to it. Parents often compare themselves to other families in ways they never did before. You might start asking whether your child has enough, whether you are falling behind, or whether everyone else seems to be handling it more easily. That comparison makes financial pressure feel personal, even when the real issue is simply a higher-cost life stage.

The Hidden Pattern Behind It

The hidden pattern is that parenting changes the meaning of money from self-management to protection. Before children, money mostly supported preference, convenience, or future goals. After children, money starts to represent safety, belonging, and adequacy. That is a powerful psychological shift because now each financial decision can feel like a judgment on the kind of parent you are.

This is why people who were once calm about money can become anxious very quickly after having children. They are not reacting only to math; they are reacting to uncertainty. A family budget can be technically balanced and still feel fragile because children create more moving parts: sudden growth spurts, school schedules, medical costs, transportation changes, and the never-ending need to plan ahead. The mind does not experience that as a spreadsheet. It experiences it as constant vigilance.

The pattern usually looks like this:

– More needs appear in smaller increments, so the pressure feels nonstop.

– Parents delay their own spending, then resent how little is left.

– Unplanned costs feel morally heavier because they affect the whole family.

– Even “normal” expenses feel like signs that something is slipping.

Another part of the pattern is that parents often start budgeting around fear instead of reality. They overestimate what they need to feel safe, or they undercount the true cost of daily family life because the numbers are easier to avoid than to face. Both responses create stress. One makes you feel trapped by scarcity; the other makes you feel blindsided by surprise. In either case, the emotional outcome is the same: money starts to feel harder than it actually is.

Common Mistakes People Make

One common mistake is treating the stress like a personal failure instead of a predictable response. Parents often say, “I used to be better with money,” when what really happened is that their life became more complex. That self-blame can make the stress worse because it adds shame to the financial pressure. Shame tends to reduce clarity, and clarity is exactly what people need when a household budget is under strain.

Another mistake is trying to make the old lifestyle fit the new season of life without adjusting the system. A single person can survive with loose categories and a few reminders in their head. A family usually cannot. Children create enough variable spending that a vague approach starts to leak money and energy. This is where a budgeting tool or expense tracker becomes useful, not because it is magical, but because it turns guesswork into visible patterns.

Some parents also make the mistake of focusing only on the biggest bills. The mortgage, rent, or childcare may get all the attention, while the smaller family costs quietly pile up in the background. Snacks, school supplies, birthday gifts, sports fees, and convenience purchases can become invisible stressors because they are scattered across the month. When people finally look at them together, they often say the same thing: “I had no idea it added up like this.”

Another common trap is waiting to feel calmer before making a plan. But calm usually comes after structure, not before it. When money feels emotionally loaded, the instinct is to avoid looking too closely. Yet avoidance keeps the pattern intact. The longer the spending stays vague, the more powerful the stress becomes, because uncertainty always feels more expensive than it is.

Real-Life Patterns and Behaviors

In real life, financial stress after children often shows up as behavior before it shows up as words. You may notice yourself checking the account more often, avoiding certain stores, delaying purchases for yourself, or feeling tense when a school email mentions fees. These reactions seem small, but they tell a bigger story: your brain is scanning for risk because the household now feels more exposed.

Many parents also become more emotionally reactive to ordinary spending decisions. A forty-dollar purchase that would have been easy before kids can suddenly feel uncomfortable, while a much larger family expense may be accepted because it feels necessary. That uneven reaction is not irrational. It is the result of money becoming emotionally segmented: some spending feels protective, while other spending feels indulgent or dangerous.

A lot of families fall into one of a few repeated patterns:

– One parent becomes the “money monitor” and carries most of the mental load.

– Spending increases quietly through convenience purchases that save time.

– Parents postpone their own needs until resentment builds.

– Income feels like it disappears faster once family logistics take over.

There is also the pattern of emotional substitution. When parents feel stretched thin, they may try to fix the discomfort with small treats, purchases for the children, or a temporary break from the pressure. That is understandable. A tired parent wants relief, not a lecture. But if the relief spending becomes automatic, it can create a loop: stress leads to spending, spending leads to less room, and less room leads to more stress.

This is where the pattern matters more than the purchase itself. The same family can have two very different experiences with the same income depending on how they move through the month. One household tracks, anticipates, and adjusts. Another absorbs stress until the pressure forces a reaction. The money may look similar on paper, but the lived experience is not even close.

What Actually Helps

What helps most is not forcing yourself to “worry less.” It is making the money more legible. When families can see where the pressure comes from, the stress often loses some of its mystery. A simple budget that separates fixed bills, variable family costs, and true buffer money can do more for peace of mind than a complicated plan that no one wants to maintain.

It also helps to stop treating every expense as equally emotional. Some costs are life maintenance, some are seasonal, and some are impulse-driven responses to exhaustion. Once you start naming those categories, you can make better decisions without turning every purchase into a moral event. That shift matters because many parents are not actually overspending wildly; they are underestimating the emotional weight of routine family life.

A calculator or budgeting tool can be useful here because it removes some of the memory burden. Even a simple spending tracker can show whether the problem is income, timing, leaks, or a mismatch between expectations and reality. This is especially helpful for middle-aged adults who are balancing childcare, work, and the constant background noise of household management. The goal is not perfection. It is visibility.

It also helps to build one small layer of margin into the family system. Not a fantasy cushion, just enough room so that every surprise does not feel like a crisis. That could mean setting aside a monthly family buffer, creating a separate category for kid-related extras, or using a budgeting app to track recurring school and activity costs. When the money has a place to go, the mind stops treating every surprise as an emergency.

Most importantly, parents often need permission to accept that this season is more demanding. That does not mean giving up. It means understanding that your stress response is not proof that you are failing. It is proof that the load is real. Once you see that clearly, you can work with the pattern instead of fighting yourself.

What To Do Next

If this article felt uncomfortably familiar, the next step is not to overhaul everything at once. Start by looking at one month of family spending with fresh eyes. Notice where the surprises actually come from, where the pressure builds, and which expenses are emotional rather than structural. That kind of review often reveals more than people expect.

If you want something practical, use a budgeting tool or calculator to map the categories that matter most: groceries, childcare, school costs, transportation, and the quiet extras that keep appearing. You do not need a perfect system to learn something useful. You only need enough visibility to see the pattern clearly. Once you can see it, the stress becomes more workable.

Then choose one small adjustment that reduces friction, not one that adds more rules. Maybe it is a separate category for kid-related costs. Maybe it is a weekly review instead of constant checking. Maybe it is setting a realistic buffer so the next surprise does not feel like proof that everything is slipping. The calmer your system, the less your money has to carry emotionally.

If you are at the point where every month feels like a fresh negotiation with yourself, that is usually the moment to pause and map the pattern rather than push harder. A simple budgeting calculator or expense tracker can help turn vague stress into something visible enough to manage. And sometimes that is the beginning of feeling steady again.

Related Reading

- Why Financial Stress Feels Heavier for Fathers

- Why Supporting Adult Children Feels Financially Endless

- Why Debt Feels Impossible When Bills Come First

Keep Exploring the Pattern

Watch more breakdowns of real-life money behavior on our YouTube channel.

Browse the full Money Behavior Library to explore more patterns like this one.

If you want a clearer view of your monthly patterns, try the Salary Breakdown Calculator, the Subscription Cost Calculator, or the Bill Due Date Planner.

Explore more patterns in the Money Behavior Library — a growing collection of real-life financial patterns explained clearly.

Disclaimer:

This content is for educational and informational purposes only and does not constitute financial advice. Always consult a qualified financial professional before making personal financial decisions.